Home Depot 2004 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2004 Home Depot annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48

|

|

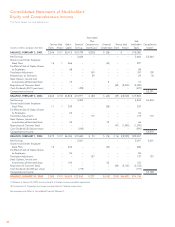

Notes to Consolidated Financial Statements (continued)

The Home Depot, Inc. and Subsidiaries

36

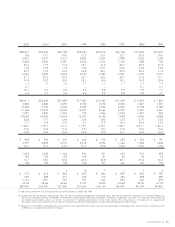

5|LEASES

The Company leases certain retail locations, office space,

warehouse and distribution space, equipment and vehicles. While

most of the leases are operating leases, certain locations and

equipment are leased under capital leases. As leases expire, it can

be expected that, in the normal course of business, certain leases

will be renewed or replaced.

Certain lease agreements include escalating rents over the lease

terms. The cumulative expense recognized on a straight-line basis

in excess of the cumulative payments is included in Other Accrued

Expenses on the accompanying Consolidated Balance Sheets.

The Company has a lease agreement under which the Company

leased assets totaling $282 million. The lease was created as a

subsequent lease to an initial lease of $600 million. These two

leases were originally created under structured financing arrange-

ments and involve three special purpose entities. The Company

financed a portion of its new stores opened in fiscal years 1997

through 2003, as well as a distribution center and office buildings,

under these lease agreements. Under both agreements, the lessor

purchased the properties, paid for the construction costs and

subsequently leased the facilities to the Company. The Company

records the rental payments under the terms of the operating lease

agreements as Selling and Store Operating Expenses in the

accompanying Consolidated Statements of Earnings.

In December 2003, the Company exercised its option to purchase

the assets under the initial lease agreement of $600 million at the

original cost of the assets of $598 million, which approximated fair

market value. These assets are included in the accompanying

Consolidated Balance Sheets in Property and Equipment and are

being depreciated on a straight-line basis over their estimated

remaining useful lives. In connection with the purchase of the

assets, one of the aforementioned special purpose entities was

dissolved, leaving two special purpose entities.

The lease term for the remaining $282 million agreement expires in

2008 with no renewal option. The lease provides for a substantial

residual value guarantee limited to 79% of the initial book value

of the assets and includes a purchase option at the original cost of

each property. As the leased assets were placed into service, the

Company estimated its liability under the residual value guarantee.

The maximum amount of the residual value guarantee relative to

the assets under the off-balance sheet lease agreement described

above is estimated to be $223 million. Events or circumstances that

would require the Company to perform under the residual value

guarantee include (1) initial default on the lease with the assets sold

for less than book value, or (2) the Company’s decision not to

purchase the assets at the end of the lease and the sale of the assets

results in proceeds less than the initial book value of the assets.

In the first quarter of fiscal 2004, the Company adopted the

revised version of FASB Interpretation No. 46, “Consolidation of

Variable Interest Entities” (“FIN 46”). FIN 46 requires consolidation

of a variable interest entity if a company’s variable interest

absorbs a majority of the entity’s expected losses or receives a

majority of the entity’s expected residual returns, or both.

In accordance with FIN 46, the Company was required to consol-

idate one of the two remaining aforementioned special purpose

entities that, before the effective date of FIN 46, met the require-

ments for non-consolidation. The second special purpose entity

that owns the assets leased by the Company totaling $282 million

is not owned by or affiliated with the Company, its management

or its officers. Pursuant to FIN 46, the Company was not deemed

to have a variable interest, and therefore was not required to

consolidate this entity.

FIN 46 requires the Company to measure the assets and liabilities

at their carrying amounts, which amounts would have been

recorded if FIN 46 had been effective at the inception of the trans-

action. Accordingly, during the first quarter of 2004, the Company

recorded Long-Term Debt of $282 million and Long-Term Notes

Receivable of $282 million on the Consolidated Balance Sheets.

The Company continues to record the rental payments under the

operating lease agreements as Selling and Store Operating

Expenses in the Consolidated Statements of Earnings. The adoption

of FIN 46 had no economic impact on the Company.

Total rent expense, net of minor sublease income for fiscal 2004,

2003 and 2002 was $684 million, $570 million and $533 million,

respectively. Certain store leases also provide for contingent rent

payments based on percentages of sales in excess of specified

minimums. Contingent rent expense for fiscal 2004, 2003 and

2002 was approximately $11 million, $7 million and $8 million,

respectively. Real estate taxes, insurance, maintenance and operat-

ing expenses applicable to the leased property are obligations of the

Company under the lease agreements.