Home Depot 2004 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2004 Home Depot annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

|

|

Notes to Consolidated Financial Statements (continued)

The Home Depot, Inc. and Subsidiaries

31The Home Depot, Inc.

Cost in Excess of the Fair Value of Net Assets Acquired

Goodwill represents the excess of purchase price over fair value of

net assets acquired. In accordance with SFAS No. 142, “Goodwill

and Other Intangible Assets,” the Company stopped amortizing

goodwill effective February 4, 2002. The Company assesses the

recoverability of goodwill at least annually by determining

whether the fair value of each reporting entity supports its carrying

value. The fair values of the Company’s identified reporting units

were estimated using the expected present value of discounted cash

flows. The Company recorded no impairment charges for fiscal

2004 or fiscal 2003 and $1.3 million for fiscal 2002.

Impairment of Long-Lived Assets

The Company evaluates the carrying value of long-lived assets

when management makes the decision to relocate or close a store,

or when circumstances indicate the carrying amount of an asset

may not be recoverable. Losses related to the impairment of long-

lived assets are recognized to the extent the sum of undiscounted

estimated future cash flows expected to result from the use of the

asset are less than the asset’s carrying value. If the carrying value

is greater than the future cash flows, a provision is made to write

down the related assets to the estimated net recoverable value.

Impairment losses were recorded as a component of Selling and

Store Operating Expenses in the accompanying Consolidated

Statements of Earnings. When a location closes, the Company also

recognizes in Selling and Store Operating Expenses the net present

value of future lease obligations, less estimated sublease income.

Stock-Based Compensation

Effective February 3, 2003, the Company adopted the fair value

method of recording stock-based compensation expense in accor-

dance with SFAS No. 123, “Accounting for Stock-Based

Compensation” (“SFAS 123”). The Company selected the prospective

method of adoption as described in SFAS No. 148, “Accounting

for Stock-Based Compensation – Transition and Disclosure” and

accordingly, stock-based compensation expense was recognized

related to stock options granted, modified or settled and expense

related to the Employee Stock Purchase Plan (“ESPP”) after the begin-

ning of fiscal 2003. The fair value of stock options and ESPP as deter-

mined on the date of grant using the Black-Scholes option-pricing

model is being expensed over the vesting period of the related stock

options and ESPP. As such, the Company recognized $86 million and

$40 million of stock-based compensation expense related to stock

options and ESPP in fiscal 2004 and 2003, respectively.

Prior to February 3, 2003, the Company elected to account for

its stock-based compensation plans under Accounting Principles

Board Opinion No. 25, “Accounting for Stock Issued to Employees”

(“APB 25”), which requires the recording of stock-based compensa-

tion expense for some, but not all, stock-based compensation.

Pursuant to APB 25, no stock-based compensation expense related

to stock option awards and ESPP was recorded in fiscal 2002.

The per share weighted average fair value of stock options granted

during fiscal 2004, 2003 and 2002 was $13.57, $9.79 and

$17.34, respectively. The fair value of these options was deter-

mined at the date of grant using the Black-Scholes option-pricing

model with the following assumptions:

Fiscal Year Ended

January 30, February 1, February 2,

2005 2004 2003

Risk-free interest rate 2.6% 3.0% 4.0%

Assumed volatility 41.3% 44.6% 44.3%

Assumed dividend yield 0.8% 1.0% 0.5%

Assumed lives of options 5 years 5 years 5 years

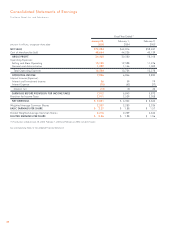

The following table illustrates the effect on Net Earnings and

Earnings per Share as if the Company had applied the fair value

recognition provisions of SFAS 123 to all stock-based compensation

in each period (amounts in millions, except per share data):

Fiscal Year Ended

January 30, February 1, February 2,

2005 2004 2003

Net Earnings, as reported $5,001 $4,304 $3,664

Add: Stock-based

compensation expense

included in reported

Net Earnings, net of

related tax effects 79 42 10

Deduct: Total stock-based

compensation expense

determined under fair

value based method

for all awards, net of

related tax effects (237) (279) (260)

Pro forma net earnings $4,843 $4,067 $3,414

Earnings per Share:

Basic – as reported $2.27 $1.88 $1.57

Basic – pro forma $2.19 $1.78 $ 1.46

Diluted – as reported $ 2.26 $ 1.88 $ 1.56

Diluted – pro forma $ 2.19 $ 1.78 $ 1.46