Haier 2009 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2009 Haier annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

31 December 2009

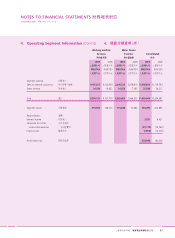

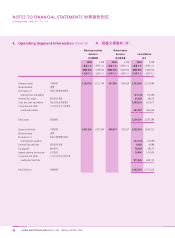

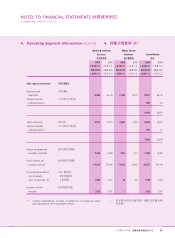

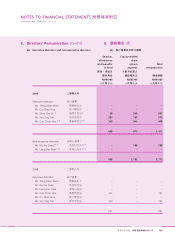

NOTES TO FINANCIAL STATEMENTS 財務報表附註

海爾電器集團有限公司 95

3. Significant Accounting Judgements and

Estimates (Cont’d)

Estimation uncertainty (Cont’d)

Write-down of inventories to net realisable value

Write-down of inventories to net realisable value is made based

on the ageing and estimated net realisable value of inventories.

The assessment of the write-down amount involves management’s

judgements and estimates. Where the actual outcome or expectation

in future is different from the original estimate, such differences

will impact the carrying value of the inventories and the write-

down charge/reversal in the period in which such estimate has

been changed.

Product warranty and installation provisions

Product warranty and installation provisions are made based on

sales volume and past experience of the level of installation services

rendered, repairs or returns. The assessment of the provision amount

involves management’s judgements and estimates. Where the actual

outcome or expectation in future is different from the original

estimate, such differences will impact the carrying amount of the

product warranty and installation provisions and the provision

amount charged/reversed in the period in which such estimate

has been changed.

Useful lives of items of property, plant and equipment

Management determines the estimated useful lives and related

depreciation for the Group’s property, plant and equipment. This

estimate is based on the historical experience of the actual useful

lives of items of property, plant and equipment of similar nature

and functions. It could change significantly as a result of technical

innovations and competitor actions in response to industry cycles.

The depreciation charge will increase where the useful lives are

less than the previously estimated useful lives, or management will

write off or write down obsolete or non-strategic assets that have

been abandoned or sold.

Impairment of receivables

The Group maintains an allowance for estimated loss arising from

the inability of its debtors to make the required payments. The Group

makes its estimates based on the ageing of its receivable balances,

debtors’ creditworthiness, and historical write-off experience. If the

financial condition of its debtors was to deteriorate so that the

actual impairment loss might be higher than expected, the Group

would be required to revise the basis of making the allowance.

3.

撇減存貨至可變現淨值

產品保養及安裝撥備

物業、廠房及設備項目之可使用年期

應收賬款減值