Haier 2009 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2009 Haier annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

31 December 2009

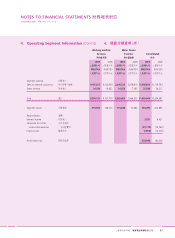

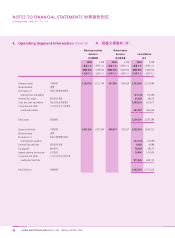

NOTES TO FINANCIAL STATEMENTS 財務報表附註

海爾電器集團有限公司 91

2.4 Summary of Significant Accounting

Policies (Cont’d)

Borrowing costs

Borrowings costs directly attributable to the acquisition, construction

or production of qualifying assets, i.e., assets that necessarily take

a substantial period of time to get ready for their intended use

or sale, are capitalised as part of the cost of those assets. The

capitalisation of such borrowing costs ceases when the assets

substantially ready for their intended use or sale. Investment

income earned on the temporary investment of specific borrowings

pending their expenditure on qualifying assets is deducted from the

borrowing costs capitalised. All other borrowing costs are expensed

in the period in which they are incurred. Borrowing costs consist

of interest and other costs that an entity incurs in connection with

the borrowing of funds.

Dividends

Final dividends proposed by the directors are classified as a separate

allocation of retained profits within the equity section of the

statement of financial position, until they have been approved

by the shareholders in a general meeting. When these dividends

have been approved by the shareholders and declared, they are

recognised as a liability.

Interim dividends are simultaneously proposed and declared,

because the Company’s bye-laws grant the directors the authority

to declare interim dividends. Consequently, interim dividends are

recognised immediately as a liability when they are proposed and

declared.

2.4