Haier 2008 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2008 Haier annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Annual Report 2008

二零零八年年報

海爾電器集團有限公司

Haier Electronics Group Co., Ltd

77

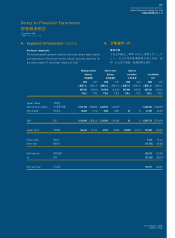

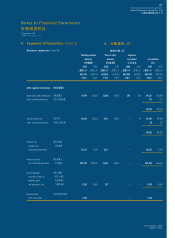

Notes to Financial Statements

財務報表附註

31 December 2008

二零零八年十二月三十一日

2.4 Summary of Significant Accounting Policies

(Cont’d)

Income tax (Cont’d)

Deferred tax assets are recognised for all deductible temporary

differences, carryforward of unused tax credits and unused tax

losses, to the extent that it is probable that taxable profit will be

available against which the deductible temporary differences, and

the carryforward of unused tax credits and unused tax losses can

be utilised, except:

• where the deferred tax asset relating to the deductible

temporary differences arises from the initial recognition of

an asset or liability in a transaction that is not a business

combination and, at the time of the transaction, affects neither

the accounting profit nor taxable profit or loss; and

• in respect of deductible temporary differences associated

with investments in subsidiaries, deferred tax assets are only

recognised to the extent that it is probable that the temporary

differences will reverse in the foreseeable future and taxable

profit will be available against which the temporary differences

can be utilised.

The carrying amount of deferred tax assets is reviewed at each

balance sheet date and reduced to the extent that it is no longer

probable that sufficient taxable profit will be available to allow all or

part of the deferred tax asset to be utilised. Conversely, previously

unrecognised deferred tax assets are reassessed at each balance

sheet date and are recognised to the extent that it is probable that

sufficient taxable profit will be available to allow all or part of the

deferred tax asset to be utilised.

Deferred tax assets and liabilities are measured at the tax rates that

are expected to apply to the period when the asset is realised or the

liability is settled, based on tax rates (and tax laws) that have been

enacted or substantively enacted at the balance sheet date.

Deferred tax assets and deferred tax liabilities are offset if a legally

enforceable right exists to set off current tax assets against current

tax liabilities and the deferred taxes relate to the same taxable entity

and the same taxation authority.

2.4 主要會計政策概要

(續)

所得稅

(續)

在有可扣稅暫時差額、承前之未動用稅項抵免

及未動用稅項虧損可供用於抵銷應課稅溢利之

情況下,遞延稅項資產乃就所有可扣稅之暫時

差額及承前之未動用稅項抵免及未動用稅項虧

損確認,惟:

• 倘遞延稅項資產關於首次確認交易(業務

合併除外)資產或負債產生之可扣稅暫時

差額,且交易時並不影響會計溢利及應課

稅溢利或虧損則另作別論;及

• 就與附屬公司之投資有關之可扣稅暫時差

額而言,只會在於可見未來可沖回暫時差

額及有應課稅溢利可供用於抵銷暫時差額

之情況下,才會確認遞延稅項資產。

於每個結算日均會審閱遞延稅項資產之賬面

值,及倘不再可能有足夠之應課稅溢利以動用

全部或部分遞延稅項資產,則會減低遞延稅項

資產。相反,於每個結算日均會重新評估之前

未確認之遞延稅項資產,而如可能有足夠應課

稅溢利以動用全部或部分遞延稅項資產,則予

以確認遞延稅項資產。

遞延稅項資產及負債按變現資產或償還負債期

間預計適用稅率計算,而預計之適用稅率乃按

結算日已頒行或大致上已頒行之稅率(及稅法)

釐定。

倘根據法例可將同一應課稅實體及同一稅務當

局的即期稅項資產與即期稅項負債以及遞延稅

項對銷,則可將遞延稅項資產與遞延稅項負債

對銷。

56432.27b!Opuft/joee!!!8856432.27b!Opuft/joee!!!88 33050311:!!!5;27;1:33050311:!!!5;27;1: