Haier 2008 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2008 Haier annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Annual Report 2008

二零零八年年報

海爾電器集團有限公司

Haier Electronics Group Co., Ltd

64

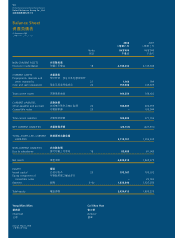

Notes to Financial Statements

財務報表附註

31 December 2008

二零零八年十二月三十一日

2.4 Summary of Significant Accounting Policies

Subsidiaries

A subsidiary is an entity whose financial and operating policies the

Company controls, directly or indirectly, so as to obtain benefits

from its activities.

The results of subsidiaries are included in the Company’s income

statement to the extent of dividends received and receivable. The

Company’s interests in subsidiaries are stated at cost less any

impairment losses.

Impairment of non-financial assets other than goodwill

Where an indication of impairment exists, or when annual

impairment testing for an asset is required (other than inventories,

deferred tax assets and financial assets), the asset’s recoverable

amount is estimated. An asset’s recoverable amount is the higher

of the asset’s or cash-generating unit’s value in use and its fair value

less costs to sell, and is determined for an individual asset, unless the

asset does not generate cash inflows that are largely independent

of those from other assets or groups of assets, in which case the

recoverable amount is determined for the cash-generating unit to

which the asset belongs.

An impairment loss is recognised only if the carrying amount of

an asset exceeds its recoverable amount. In assessing value in use,

the estimated future cash flows are discounted to their present

value using a pre-tax discount rate that reflects current market

assessments of the time value of money and the risks specific to

the asset. An impairment loss is charged to the income statement

in the period in which it arises.

An assessment is made at each reporting date as to whether

there is any indication that previously recognised impairment losses

may no longer exist or may have decreased. If such an indication

exists, the recoverable amount is estimated. A previously recognised

impairment loss of an asset other than goodwill is reversed only if

there has been a change in the estimates used to determine the

recoverable amount of that asset, but not to an amount higher than

the carrying amount that would have been determined (net of any

depreciation/amortisation) had no impairment loss been recognised

for the asset in prior years. A reversal of such an impairment loss is

credited to the income statement in the period in which it arises.

2.4 主要會計政策概要

附屬公司

附屬公司指本公司直接或間接控制其財政及經

營政策以自該實體之業務獲益之實體。

附屬公司之業績按已收及應收之股息,計入本

公司之收益表。本公司於附屬公司之權益乃按

成本減任何減值虧損列賬。

商譽以外之非財務資產減值

倘出現任何減值跡象或按規定每年檢討資產(不

包括存貨、遞延稅項資產及財務資產)顯示減

值,則會估計資產之可收回數額。資產之可收

回數額乃按資產或現金產生單位之使用價值及

公平值減銷售成本兩者中之較高者計算,而個

別資產須分開計算,惟若資產並不產生明顯獨

立於其他資產或資產組別之現金流入,則可收

回數額按資產所屬現金產生單位之可收回數額

計算。

當資產之賬面值超出其可收回數額時,方會確

認減值虧損。評估使用價值時,估計未來現金

流量按可反映貨幣時間價值及資產特定風險之

現時市場評估之稅前貼現率貼現為現值。減值

虧損乃於產生期間在收益表中扣除。

於各申報日期,將評估有否跡象顯示過往已確

認之減值虧損不再存在或可能減少。若出現上

述跡象,則估計可收回數額。當用以釐定資產

可收回數額之估計方法有變時,方會撥回先前

已確認之資產減值虧損(商譽除外),惟撥回之

數額不得超逾假設過往年度並無就該項資產確

認減值虧損之原賬面值(已扣除任何折舊╱攤

銷)。撥回之減值虧損乃於產生期間計入收益

表。

56432.27b!Opuft/joee!!!7556432.27b!Opuft/joee!!!75 33050311:!!!5;27;1333050311:!!!5;27;13