HSBC 2015 Annual Report Download - page 424

Download and view the complete annual report

Please find page 424 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

414 -

415

415 -

416

416 -

417

417 -

418

418 -

419

419 -

420

420 -

421

421 -

422

422 -

423

423 -

424

424 -

425

425 -

426

426 -

427

427 -

428

428 -

429

429 -

430

430 -

431

431 -

432

432 -

433

433 -

434

434 -

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

Notes on the Financial Statements (continued)

29 – Provisions / 30 – Subordinated liabilities

HSBC HOLDINGS PLC

422

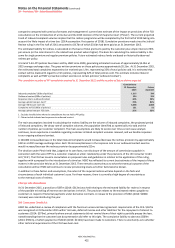

companies compared with previous forecasts and management’s current best estimate of the impact on provisions of the FCA

consultation on the introduction of a time bar and the 2014 decision of the UK Supreme Court (‘Plevin’). The current projected

trend of inbound complaint volumes implies that the redress programme will be completed by the first half of 2018 taking into

account the likely impact of a time bar. (2014 assumption: first quarter of 2018). Cumulative provisions made since the Judicial

Review ruling in the first half of 2011 amounted to $4.7bn of which $3.6bn had been paid as at 31 December 2015.

The estimated liability for redress is calculated on the basis of total premiums paid by the customer plus simple interest of 8%

per annum (or the rate inherent in the related loan product where higher). The basis for calculating the redress liability is the

same for single premium and regular premium policies. Future estimated redress levels are based on historically observed

redress per policy.

A total of 5.4m PPI policies have been sold by HSBC since 2000, generating estimated revenues of approximately $4.0bn at

2015 average exchange rates. The gross written premiums on these policies was approximately $5.2bn. At 31 December 2015,

the estimated total complaints expected to be received was 1.9m, representing 35% of total policies sold. It is estimated that

contact will be made with regard to 2.3m policies, representing 42% of total policies sold. This estimate includes inbound

complaints as well as HSBC’s proactive contact exercise on certain policies (‘outbound contact’).

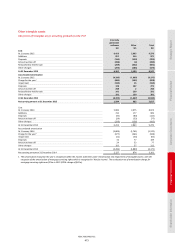

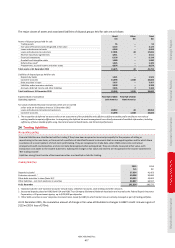

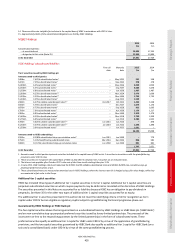

The cumulative number of PPI complaints received to 31 December 2015 and the number of future claims expected

Cumulative to

31 December

2015

Future

expected

Inbound complaints1 (000s of policies) 1,215 336

Outbound contact (000s of policies) 624 101

Response rate to outbound contact 44% 52%

Average uphold rate per claim2 74% 81%

Average redress per claim ($) 3,058 2,844

Complaints to FOS (000s of policies) 121 51

Average uphold rate per FOS claim 36% 53%

1 Excludes invalid claims where the complainant has not held a PPI policy.

2 Claims include inbound and responses to outbound contact.

The main assumptions involved in calculating the redress liability are the volume of inbound complaints, the projected period

of inbound complaints, the decay rate of complaint volumes, the population identified as systemically mis-sold and the

number of policies per customer complaint. The main assumptions are likely to evolve over time as root cause analysis

continues, more experience is available regarding customer-initiated complaint volumes received, and we handle responses

to our ongoing outbound contact.

A 100,000 increase/decrease in the total inbound complaints would increase/decrease the redress provision by approximately

$221m at 2015 average exchange rates. Each 1% increase/decrease in the response rate to our outbound contact exercise

would increase/decrease the redress provision by approximately $15m.

The decision under Plevin held that, judged on its own facts, non-disclosure of the amount of commissions payable in

connection with the sale of PPI to a customer created an unfair relationship under the provisions of the UK Consumer Credit

Act (‘CCA’). The FCA has issued a consultation on proposed rules and guidelines in relation to the application of this ruling,

together with a proposal for the introduction of a time bar. HSBC has reflected its current best estimate of the impact of these

matters in the provision held as at 31 December 2015. There remains uncertainty as to what the eventual outcome of the

consultation will be: HSBC will continue to review provisioning levels as further facts become known.

In addition to these factors and assumptions, the extent of the required redress will also depend on the facts and

circumstances of each individual customer’s case. For these reasons, there is currently a high degree of uncertainty as

to the eventual costs of redress.

Interest rate derivatives

At 31 December 2015, a provision of $87m (2014: $312m) was held relating to the estimated liability for redress in respect

of the possible mis-selling of interest rate derivatives in the UK. The provision relates to the estimated redress payable to

customers in respect of historical payments under derivative contracts. A release to the provision of $38m (2014: $288m

increase) was recorded during the year.

UK Consumer Credit Act

HSBC has undertaken a review of compliance with the fixed-sum unsecured loan agreement requirements of the CCA. $167m

was recognised at 31 December 2015 within ‘Accruals, deferred income and other liabilities’ for the repayment of interest to

customers (2014: $379m), primarily where annual statements did not remind them of their right to partially prepay the loan,

notwithstanding that the customer loan documentation did refer to this right. The cumulative liability to date was $569m

(2014: $591m), of which payments of $414m (2014: $212m) have been made to customers. There is uncertainty as to whether

other technical requirements of the CCA have been met.