HSBC 2015 Annual Report Download - page 421

Download and view the complete annual report

Please find page 421 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

411 -

412

412 -

413

413 -

414

414 -

415

415 -

416

416 -

417

417 -

418

418 -

419

419 -

420

420 -

421

421 -

422

422 -

423

423 -

424

424 -

425

425 -

426

426 -

427

427 -

428

428 -

429

429 -

430

430 -

431

431 -

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

HSBC HOLDINGS PLC

419

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

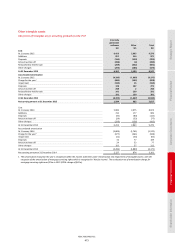

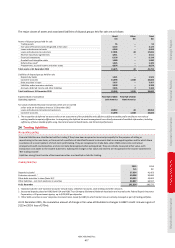

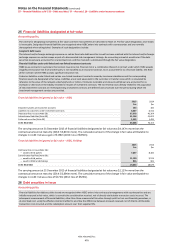

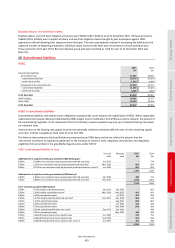

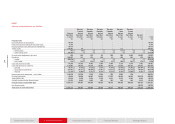

Debt securities in issue – HSBC

2015 2014

$m $m

Bonds and medium-term notes 128,348 132,539

Other debt securities in issue 28,804 43,374

157,152 175,913

Of which debt securities in issue reported as:

–

trading liabilities (Note 24) (30,525) (33,602)

–

financial liabilities designated at fair value (Note 25) (37,678) (46,364)

At 31 December 88,949 95,947

Debt securities in issue – HSBC Holdings

2015 2014

$m $m

Debt securities 8,857 9,194

Of which debt securities in issue reported as:

–

financial liabilities designated at fair value (Note 25) (7,897) (8,185)

At 31 December 960 1,009

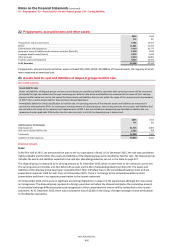

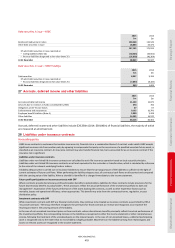

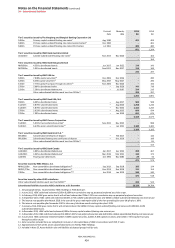

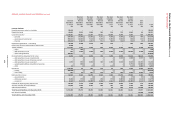

27 Accruals, deferred income and other liabilities

2015 2014

$m $m

Accruals and deferred income 11,129 15,075

Amounts due to investors in funds consolidated by HSBC 474 782

Obligations under finance leases 37 67

Endorsements and acceptances 9,135 10,760

Employee benefit liabilities (Note 6) 2,809 3,208

Other liabilities 14,532 16,570

At 31 December 38,116 46,462

Accruals, deferred income and other liabilities include $29,358m (2014: $39,846m) of financial liabilities, the majority of which

are measured at amortised cost.

28 Liabilities under insurance contracts

Accounting policy

HSBC issues contracts to customers that contain insurance risk, financial risk or a combination thereof. A contract under which HSBC accepts

significant insurance risk from another party by agreeing to compensate that party on the occurrence of a specified uncertain future event, is

classified as an insurance contract. An insurance contract may also transfer financial risk, but is accounted for as an insurance contract if the

insurance risk is significant.

Liabilities under insurance contracts

Liabilities under non-linked life insurance contracts are calculated by each life insurance operation based on local actuarial principles.

Liabilities under unit-linked life insurance contracts are at least equivalent to the surrender or transfer value, which is calculated by reference

to the value of the relevant underlying funds or indices.

A liability adequacy test is carried out on insurance liabilities to ensure that the carrying amount of the liabilities is sufficient in the light of

current estimates of future cash flows. When performing the liability adequacy test, all contractual cash flows are discounted and compared

with the carrying value of the liability. When a shortfall is identified it is charged immediately to the income statement.

Future profit participation on insurance contracts with DPF

Where contracts provide discretionary profit participation benefits to policyholders, liabilities for these contracts include provisions for the

future discretionary benefits to policyholders. These provisions reflect the actual performance of the investment portfolio to date and

management’s expectation of the future performance of the assets backing the contracts, as well as other experience factors such as

mortality, lapses and operational efficiency, where appropriate. This benefit may arise from the contractual terms, regulation, or past

distribution policy.

Investment contracts with DPF

While investment contracts with DPF are financial instruments, they continue to be treated as insurance contracts as permitted by IFRS 4

‘Insurance Contracts’. The Group therefore recognises the premiums for those contracts as revenue and recognises as an expense the

resulting increase in the carrying amount of the liability.

In the case of net unrealised investment gains on these contracts, whose discretionary benefits principally reflect the actual performance of

the investment portfolio, the corresponding increase in the liabilities is recognised in either the income statement or other comprehensive

income, following the treatment of the unrealised gains on the relevant assets. In the case of net unrealised losses, a deferred participating

asset is recognised only to the extent that its recoverability is highly probable. Movements in the liabilities arising from realised gains and

losses on relevant assets are recognised in the income statement.