HSBC 2015 Annual Report Download - page 244

Download and view the complete annual report

Please find page 244 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

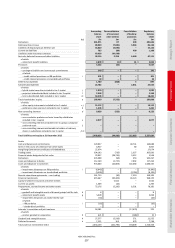

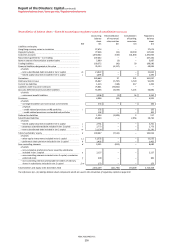

Report of the Directors: Capital (continued)

Regulatory developments / Appendix to Capital

HSBC HOLDINGS PLC

242

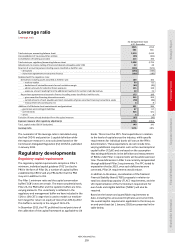

It is anticipated that a minimum leverage ratio

requirement, including potential buffers for G-SIBs, will

be consulted upon by the Basel Committee in 2016 and a

formal Pillar 1 measure finalised by 1 January 2018.

Total loss absorbing capacity proposals

As part of Recovery and Resolution frameworks both in

the EU and internationally, there have been various

developments in relation to TLAC. In the EU, the Bank

Recovery and Resolution Directive introduces an MREL.

In July 2015, the EBA published a final draft Regulatory

Technical Standard (‘RTS’) for MREL which seeks to provide

additional clarity on the criteria that resolution authorities

should take into account when setting a firm specific MREL

requirement. The EBA notes that it aims to implement the

MREL in a way which is consistent with the finalised

international standard on TLAC.

In November 2015, the FSB published finalised proposals

on TLAC for G-SIBs to be applied in accordance with

individual bank resolution strategies. This set out a

requirement of 16% of RWAs and a TLAC leverage ratio

of 6% to be met from 1 January 2019, increasing to 18%

and 6.75% respectively, from 1 January 2022. Existing

regulatory capital buffers will need to be met in addition to

the minimum TLAC requirement. A breach of TLAC will be

treated as severely as a breach of minimum capital

requirements.

In November 2015, the Basel Committee also published a

consultation on the treatment of banks’ holdings of TLAC

instruments issued by a G-SIB, which proposed new

deductions from regulatory capital. Once finalised, any

additional requirements in relation to TLAC are expected to

be reflected in MREL and to be implemented in the UK.

In December 2015, the Bank of England published a

consultation paper on the UK’s implementation of MREL.

The Bank of England stated that it intends to set MREL

consistent with both TLAC and the final EBA RTS expected

to be published later this year. The MREL is expected to

comprise a loss absorption amount which reflects existing

regulatory capital requirements and a recapitalisation

amount which reflects the capital that a firm is likely to

need post resolution. The latter can be met with both

regulatory capital and eligible liabilities.

While MREL is to be set on an individual basis, the Bank

of England generally expects MREL for banks whose

appropriate resolution strategy is bail-in, to be equivalent

to twice the current minimum capital requirements. A

finalised Statement of Policy is expected by mid-2016. The

Bank of England is also expected to provide firms with an

indication of their prospective 2020 MREL during 2016, and

will set MREL on a transitional basis until then. For G-SIBs,

MREL is proposed to apply from 2019, consistent with FSB

timelines.

In parallel to the above, the PRA separately published a

consultation paper on the interaction between MREL and

capital buffers and how it would treat a breach of MREL

requirements. This proposed that banks should not be able

to meet MREL requirements with CET1 used to meet

existing capital and leverage ratio buffers.

Structural reform and recovery and

resolution planning

Globally there have been a number of developments relating

to banking structural reform and the introduction of

recovery and resolution regimes. As part of recovery and

resolution planning, some regulators and national authorities

have also required changes to the corporate structures of

banks. These include requiring the local incorporation of

banks or ring-fencing of certain businesses.

In 2013 and 2014, UK legislation was enacted requiring large

banking groups to ring-fence UK retail and SME banking

activity in a separately incorporated banking subsidiary

(a ‘ring-fenced bank’) that is prohibited from engaging in

significant trading activity. Ring-fencing is to be completed by

1 January 2019. The legislation also detailed the applicable

individual customers to be transferred to the ring-fenced

bank. In addition, the legislation places restrictions on the

activities and geographical scope of ring-fenced banks.

Throughout 2015 the PRA published a number of

consultations on the implementation of ring-fencing

requirements and the finalisation of rules is expected to

continue in 2016.

The key proposals included near final rules published in

May 2015 on legal structure, corporate governance, and

continuity of services and facilities.

Additionally, in October 2015, the PRA issued a consultation

on the application of capital and liquidity rules for ring-

fenced banks, management of intra-group exposures, and

use of financial market infrastructures. The PRA intends to

undertake a further consultation in 2016 in respect of

reporting and disclosure, and publish finalised rules and

supervisory statements thereafter, with implementation by

1 January 2019.

We are working with our primary regulators to develop and

agree a resolution strategy for HSBC. It is our view that a

strategy by which the Group breaks up at a subsidiary bank

level at the point of resolution (referred to as a Multiple

Point of Entry) is the optimal approach, as it is aligned to

our existing legal and business structure. Similarly to all

G-SIBs, we are working with our regulators to mitigate

or remove critical inter-dependencies between our

subsidiaries to further facilitate the resolution of the

Group. In particular, in order to remove operational

dependencies (where one subsidiary bank provides critical

services to another), we are in the process of transferring

critical services from our subsidiary banks to a separate

internal group of service companies (‘ServCo group’).

During 2015, more than 18,000 employees performing

shared services in the UK were transferred to the ServCo

group. Further transfers of employees, critical shared

services and assets in the UK, Hong Kong and other

jurisdictions will occur in due course.