HSBC 2015 Annual Report Download - page 206

Download and view the complete annual report

Please find page 206 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

Report of the Directors: Risk (continued)

Appendix to Risk – Policies and practices

HSBC HOLDINGS PLC

204

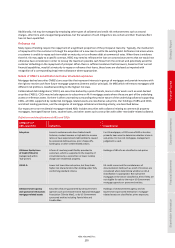

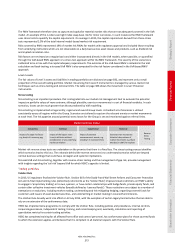

Categories of ABSs and CDOs Definition Classification

UK non-conforming mortgages

(categorised within ‘Sub-prime’)

UK mortgages that do not meet normal lending criteria.

Examples include mortgages where the expected level of

documentation is not provided (such as income with self-

certification), or where poor credit history increases risk and

results in pricing at a higher than normal lending rate.

UK non-conforming mortgages are

treated as sub-prime exposures.

Other residential mortgages Residential mortgages, including prime mortgages, that do not

meet any of the classifications described above.

Prime residential mortgage-related

assets are included in this category.

Liquidity and funding

The management of liquidity and funding is primarily undertaken locally (by country) in our operating entities in compliance

with the Group’s Liquidity and Funding Risk Management Framework (the ‘LFRF’), and with practices and limits set by the GMB

through the RMM and approved by the Board. These limits vary according to the depth and the liquidity of the markets in

which the entities operate. Our general policy is that each defined operating entity should be self-sufficient in funding its own

activities. Where transactions exist between operating entities, they are reflected symmetrically in both entities.

As part of our Asset, Liability and Capital Management (‘ALCM’) structure, we have established ALCOs at Group level, in the

regions and in operating entities. The terms of reference of all ALCOs include the monitoring and control of liquidity and

funding.

The primary responsibility for managing liquidity and funding within the Group’s framework and risk appetite resides with the

local operating entities’ ALCOs. Our most significant operating entities are overseen by regional ALCOs, Group ALCO and the

RMM. The remaining smaller operating entities are overseen by regional ALCOs, with appropriate escalation of significant

issues to Group ALCO and the RMM.

Operating entities are predominately defined on a country basis to reflect our local management of liquidity and funding.

Typically, an operating entity will be defined as a single legal entity. However, to take account of the situation where

operations in a country are booked across multiple subsidiaries or branches:

• an operating entity may be defined as a wider sub-consolidated group of legal entities if they are incorporated in the same

country, liquidity and funding are freely fungible between the entities and permitted by local regulation, and the definition

reflects how liquidity and funding are managed locally; or

• an operating entity may be defined more narrowly as a principal office (branch) of a wider legal entity operating in multiple

countries, reflecting the local country management of liquidity and funding.

The RMM reviews and agrees annually the list of entities it directly oversees and the composition of these entities.

Primary sources of funding

Customer deposits in the form of current accounts and savings deposits payable on demand or at short notice form a

significant part of our funding, and we place considerable importance on maintaining their stability. For deposits, stability

depends upon maintaining depositor confidence in our capital strength and liquidity, and on competitive and transparent

pricing.

We also access wholesale funding markets by issuing senior secured and unsecured debt securities (publically and privately)

and borrowing from the secured repo markets against high quality collateral, in order to obtain funding for non-banking

subsidiaries that do not accept deposits, to align asset and liability maturities and currencies and to maintain a presence in

local wholesale markets.

The management of liquidity and funding risk

Inherent liquidity risk categorisation

We place our operating entities into one of two categories (low and medium) to reflect our assessment of their inherent

liquidity risk considering political, economic and regulatory factors within the host country and factors specific to the operating

entities themselves, such as their local market, market share and balance sheet strength. The categorisation involves

management judgement and is based on the perceived liquidity risk of an operating entity relative to other entities in the

Group. The categorisation is intended to reflect the possible impact of a liquidity event, not the probability of an event, and

forms part of our risk appetite. It is used to determine the prescribed stress scenario that we require our operating entities to

be able to withstand and manage to.

Core deposits

A key element of our internal framework is the classification of customer deposits into core and non-core based on our

expectation of their behaviour during periods of liquidity stress. This characterisation takes into account the inherent liquidity