HSBC 2015 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

HSBC HOLDINGS PLC

137

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

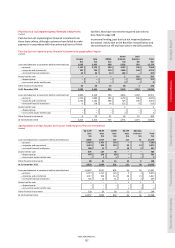

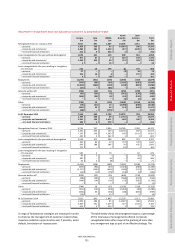

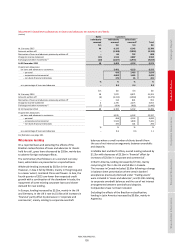

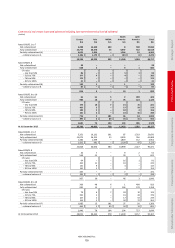

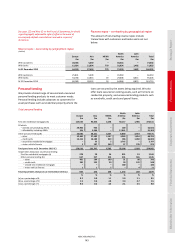

Commercial real estate

Commercial real estate lending

Europe Asia MENA

North

America

Latin

America Total

$m $m $m $m $m $m

Neither past due nor impaired 24,533 32,182 466 6,659 1,086 64,926

Past due but not impaired 89 119 25 212 9 454

Impaired loans 1,634 70 199 161 482 2,546

Total gross loans and advances at 31 December 2015 26,256 32,371 690 7,032 1,577 67,926

Of which:

–

renegotiated loans12 1,586 6182 150 210 2,134

Impairment allowances 613 35 145 76 343 1,212

Neither past due nor impaired 25,860 35,430 333 6,136 1,535 69,294

Past due but not impaired 18 170 47 100 28 363

Impaired loans 2,309 78 199 322 728 3,636

Total gross loans and advances at 31 December 2014 28,187 35,678 579 6,558 2,291 73,293

Of which:

–

renegotiated loans12 1,954 19 183 191 377 2,724

Impairment allowances 909 44 147 101 476 1,677

For footnote, see page 191.

Commercial real estate lending includes the financing of

corporate, institutional and high net worth individuals who

are investing primarily in income-producing assets and, to a

lesser extent, in their construction and development. The

business focuses mainly on traditional core asset classes

such as retail, offices, light industrial and residential

building projects. The portfolio is globally diversified with

larger concentrations in Hong Kong, the UK, the US and

Canada.

In more developed markets, our exposure mainly

comprises the financing of investment assets, the

redevelopment of existing stock and the augmentation

of both commercial and residential markets to support

economic and population growth. In lesser developed

commercial real estate markets our exposures comprise

lending for development assets on relatively short tenors

with a particular focus on supporting the larger, better

capitalised developers involved in residential construction

or in assets supporting economic expansion.

Our global exposure is centred largely on cities representing

key locations of economic, political or cultural significance.

In many lesser developed markets, industry is evolving to

move away from the development and rapid construction

of recent years to increasingly focus on investment stock

consistent with more developed markets.

Excluding the effects of the Brazilian reclassification,

commercial real estate lending was lower by $4.5bn

including decreases of $3.2bn relating to adverse foreign

exchange movements.

The commentary that follows is on a constant currency

basis, while tables are presented on a reported basis.

The commercial real estate lending was lower by $1.3bn,

largely due to a decrease of $2.6bn in Asia, mainly in

Hong Kong and, to a lesser extent, mainland China and

Singapore. The decrease in Asia was mainly due to the

repayment and maturity of loans and was partly offset by

increases of $1.0bn in North America and $0.4bn in

Mexico. Europe and Middle East and Africa remained

largely unchanged.

Refinance risk in commercial real estate

Commercial real estate lending tends to require the

repayment of a significant proportion of the principal at

maturity. Typically, a customer will arrange repayment

through the acquisition of a new loan to settle the existing

debt. Refinance risk is the risk that a customer, being unable

to repay the debt on maturity, fails to refinance it at

commercial rates. We monitor our commercial real estate

portfolio closely, assessing those drivers that may indicate

potential issues with refinancing. The principal driver is the

vintage of the loan, when origination reflected previous

market norms which do not apply in the current market.

Examples might be higher loan-to-value (‘LTV’) ratios and/or

lower interest cover ratios. The range of refinancing sources

in the local market is also an important consideration, with

risk increasing when lenders are restricted to banks and

when bank liquidity is limited. In addition, underlying

fundamentals such as the reliability of tenants, the ability to

let and the condition of the property are important as they

influence property values.