HSBC 2015 Annual Report Download - page 391

Download and view the complete annual report

Please find page 391 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

381 -

382

382 -

383

383 -

384

384 -

385

385 -

386

386 -

387

387 -

388

388 -

389

389 -

390

390 -

391

391 -

392

392 -

393

393 -

394

394 -

395

395 -

396

396 -

397

397 -

398

398 -

399

399 -

400

400 -

401

401 -

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

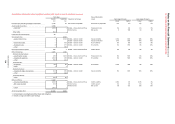

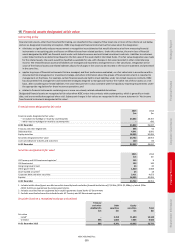

HSBC HOLDINGS PLC

389

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

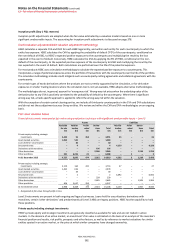

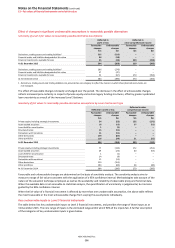

Private equity including strategic investments

Given the bespoke nature of the analysis in respect of each holding, it is not practical to quote a range of key unobservable

inputs.

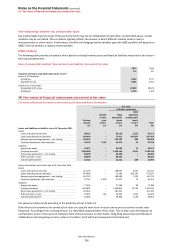

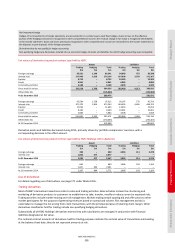

Prepayment rates

Prepayment rates are a measure of the anticipated future speed at which a loan portfolio will be repaid in advance of the due

date. They are an important input into modelled values of ABSs. A modelled price may be used where insufficient observable

market prices exist to enable a market price to be determined directly. Prepayment rates are also an important input into the

valuation of derivatives linked to securitisations. They vary according to the nature of the loan portfolio and expectations of

future market conditions, and may be estimated using a variety of evidence, such as prepayment rates implied from proxy

observable security prices, current or historical prepayment rates and macroeconomic modelling.

Market proxy

Market proxy pricing may be used for an instrument for which specific market pricing is not available, but evidence is available

in respect of instruments that have some characteristics in common. In some cases it might be possible to identify a specific

proxy, but more generally evidence across a wider range of instruments will be used to understand the factors that influence

current market pricing and the manner of that influence.

The range of prices used as inputs into a market proxy pricing methodology may therefore be wide. This range is not indicative

of the uncertainty associated with the price derived for an individual security.

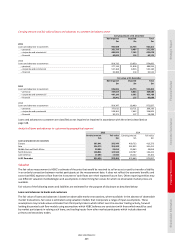

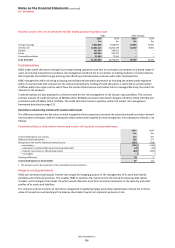

Volatility

Volatility is a measure of the anticipated future variability of a market price, tending to increase in stressed market conditions

and decrease in calmer market conditions. It is an important input in the pricing of options. In general, the higher the volatility,

the more expensive the option will be. This reflects both the higher probability of an increased return from the option and the

potentially higher costs that HSBC may incur in hedging the risks associated with the option. If option prices become more

expensive, this increases the value of HSBC’s long option positions (i.e. the positions in which HSBC has purchased options),

while HSBC’s short option positions (i.e. the positions in which HSBC has sold options) suffer losses.

Volatility varies by underlying reference market price, and by strike and maturity of the option. Volatility also varies over time.

As a result, it is difficult to make general statements regarding volatility levels.

Certain volatilities, typically those of a longer-dated nature, are unobservable. The unobservable volatility is then estimated

from observable data. The range of unobservable volatilities quoted in the table on page 387 reflects the wide variation in

volatility inputs by reference market price. The core range is significantly narrower than the full range because these examples

with extreme volatilities occur relatively rarely within the HSBC portfolio. For any single unobservable volatility, the

uncertainty in the volatility determination is significantly less than the range quoted above.

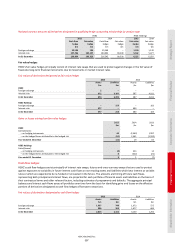

Correlation

Correlation is a measure of the inter-relationship between two market prices and is expressed as a number between minus

one and one. A positive correlation implies that the two market prices tend to move in the same direction, with a correlation

of one implying that they always move in the same direction. A negative correlation implies that the two market prices tend

to move in opposite directions, with a correlation of minus one implying that the two market prices always move in opposite

directions. Correlation is used to value more complex instruments where the payout is dependent upon more than one market

price. There is a wide range of instruments for which correlation is an input, and consequently a wide range of both same-asset

correlations (e.g. equity-equity correlation) and cross-asset correlations (e.g. foreign exchange rate-interest rate correlation) is

used. In general, the range of same-asset correlations will be narrower than the range of cross-asset correlations.

Correlation may be unobservable. Unobservable correlations may be estimated based upon a range of evidence, including

consensus pricing services, HSBC trade prices, proxy correlations and examination of historical price relationships.

The range of unobservable correlations quoted in the table reflects the wide variation in correlation inputs by market price

pair. For any single unobservable correlation, the uncertainty in the correlation determination is likely to be less than the range

quoted above.

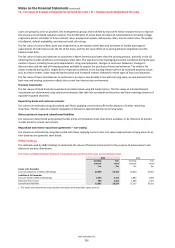

Credit spread

Credit spread is the premium over a benchmark interest rate required by the market to accept lower credit quality. In

a discounted cash flow model, the credit spread increases the discount factors applied to future cash flows, thereby reducing

the value of an asset. Credit spreads may be implied from market prices. Credit spreads may not be observable in more illiquid

markets.