HSBC 2015 Annual Report Download - page 380

Download and view the complete annual report

Please find page 380 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

370 -

371

371 -

372

372 -

373

373 -

374

374 -

375

375 -

376

376 -

377

377 -

378

378 -

379

379 -

380

380 -

381

381 -

382

382 -

383

383 -

384

384 -

385

385 -

386

386 -

387

387 -

388

388 -

389

389 -

390

390 -

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

Notes on the Financial Statements (continued)

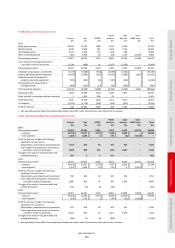

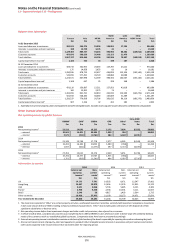

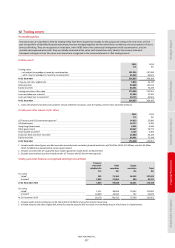

13 – Fair values of financial instruments carried at fair value

HSBC HOLDINGS PLC

378

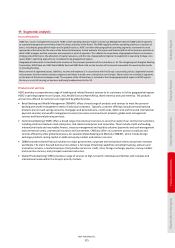

13 Fair values of financial instruments carried at fair value

Accounting policy

All financial instruments are recognised initially at fair value. Fair value is the price that would be received to sell an asset or paid to transfer

a liability in an orderly transaction between market participants at the measurement date. The fair value of a financial instrument on initial

recognition is generally its transaction price (that is, the fair value of the consideration given or received). However, sometimes the fair value

will be based on other observable current market transactions in the same instrument, without modification or repackaging, or on a

valuation technique whose variables include only data from observable markets, such as interest rate yield curves, option volatilities and

currency rates. When such evidence exists, HSBC recognises a trading gain or loss at inception (‘day 1 gain or loss’), being the difference

between the transaction price and the fair value. When significant unobservable parameters are used, the entire day 1 gain or loss is

deferred and is recognised in the income statement over the life of the transaction until the transaction matures or is closed out, the

valuation inputs become observable or HSBC enters into an offsetting transaction.

The fair value of financial instruments is generally measured on an individual basis. However, in cases where HSBC manages a group of

financial assets and liabilities according to its net market or credit risk exposure, the fair value of the group of financial instruments is

measured on a net basis but the underlying financial assets and liabilities are presented separately in the financial statements, unless they

satisfy the IFRSs offsetting criteria as described in Note 32.

Critical accounting estimates and judgements

Valuation of financial instruments

The best evidence of fair value is a quoted price in an actively traded principal market. The fair values of financial instruments that are

quoted in active markets are based on bid prices for assets held and offer prices for liabilities issued. When a financial instrument has a

quoted price in an active market, the fair value of the total holding of the financial instrument is calculated as the product of the number of

units and the quoted price. The judgement as to whether a market is active may include, but is not restricted to, consideration of factors

such as the magnitude and frequency of trading activity, the availability of prices and the size of bid/offer spreads. The bid/offer spread

represents the difference in prices at which a market participant would be willing to buy compared with the price at which they would be

willing to sell. Valuation techniques may incorporate assumptions about factors that other market participants would use in their valuations,

including:

• the likelihood and expected timing of future cash flows on the instrument. Judgement may be required to assess the counterparty’s

ability to service the instrument in accordance with its contractual terms. Future cash flows may be sensitive to changes in market rates;

• selecting an appropriate discount rate for the instrument. Judgement is required to assess what a market participant would regard as the

appropriate spread of the rate for an instrument over the appropriate risk-free rate; and

• judgement to determine what model to use to calculate fair value in areas where the choice of valuation model is particularly subjective,

for example, when valuing complex derivative products.

A range of valuation techniques is employed, dependent on the instrument type and available market data. Most valuation techniques are

based upon discounted cash flow analyses, in which expected future cash flows are calculated and discounted to present value using a

discounting curve. Prior to considering credit risk, the expected future cash flows may be known, as would be the case for the fixed leg of an

interest rate swap, or may be uncertain and require projection, as would be the case for the floating leg of an interest rate swap. ‘Projection’

utilises market forward curves, if available. In option models, the probability of different potential future outcomes must be considered. In

addition, the value of some products is dependent on more than one market factor, and in these cases it will typically be necessary to

consider how movements in one market factor may affect the other market factors. The model inputs necessary to perform such calculations

include interest rate yield curves, exchange rates, volatilities, correlations and prepayment and default rates. For interest rate derivatives

with collateralised counterparties and in significant currencies, HSBC uses a discounting curve that reflects the overnight interest rate.

The majority of valuation techniques employ only observable market data. However, certain financial instruments are valued on the basis of

valuation techniques that feature one or more significant market inputs that are unobservable, and for them the measurement of fair value

is more judgemental. An instrument in its entirety is classified as valued using significant unobservable inputs if, in the opinion of

management, a significant proportion of the instrument’s inception profit or greater than 5% of the instrument’s valuation is driven by

unobservable inputs. ‘Unobservable’ in this context means that there is little or no current market data available from which to determine

the price at which an arm’s length transaction would be likely to occur. It generally does not mean that there is no data available at all upon

which to base a determination of fair value (consensus pricing data may, for example, be used).

Control framework

Fair values are subject to a control framework designed to ensure that they are either determined or validated by a function

independent of the risk taker.

For all financial instruments where fair values are determined by reference to externally quoted prices or observable pricing

inputs to models, independent price determination or validation is utilised. In inactive markets HSBC will source alternative

market information to validate the financial instrument’s fair value, with greater weight given to information that is considered

to be more relevant and reliable. The factors that are considered in this regard are, inter alia:

• the extent to which prices may be expected to represent genuine traded or tradeable prices;

• the degree of similarity between financial instruments;

• the degree of consistency between different sources;

• the process followed by the pricing provider to derive the data;

• the elapsed time between the date to which the market data relates and the balance sheet date; and