HSBC 2015 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

HSBC HOLDINGS PLC

117

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

Other entities in the Group, including The Hongkong

and Shanghai Banking Corporation Limited and HSBC Bank

plc, continue to participate in regulatory stress tests

conducted at a subsidiary level by local regulators.

In October 2015, the BoE published details of its medium-

term approach to stress testing the UK banking system. Key

features of the approach include an annual cyclical stress

test and a biennial exploratory stress test, starting in 2017.

The EBA plan to conduct stress tests in 2016. Details of their

proposed approach were published by them in November

2015.

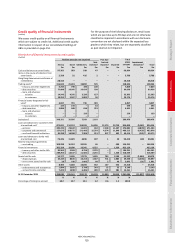

Oil and gas prices

Oil and commodity prices have remained low since the

middle of 2014 as a result of existing global supply and

demand imbalances, with significant price declines in late

2015 and early 2016. Continued lower oil prices cause

increased credit risks within oil-related industries together

with fiscal and financing challenges for energy exporters.

The overall portfolio of exposures directly exposed to oil and

gas companies had drawn risk exposures amounting to

about $29bn (2014: $34bn) with sub-sectoral distributions as

follows: integrated producers 48%, service companies 28%,

pure producers 17% and infrastructure companies 7%.

The credit quality distribution of the oil and gas portfolio was

as follows: ‘strong’ and ‘good’ categories made up 56% of

the portfolio, ‘satisfactory’ 35%, ‘sub-standard’ 7% and

‘impaired’ 2%. The majority of the exposures were located in

North America, Asia and Europe.

Oil and gas related counterparties have responded rapidly to

the changing economic outlook, cutting back on capital

expenditure as well as reducing operating expenses in order

to manage cash flows and sustain profitability.

Large integrated producers remained resilient. Within the

pure producers sector, the higher cost entities such as shale

and oil sands producers showed more evidence of stress,

resulting in credit grade deterioration. Similarly, service

companies continued to be more vulnerable as producers

curtailed capital expenditures.

Individually assessed loan impairment charges in 2015

remained contained at approximately $0.3bn. Oil prices are

now predicted to remain lower for longer and the oil price

recovery is dependent on the removal of the excess supply

that currently exists in the market. In view of these factors

collective allowances for exposures related to oil and gas

were increased by $0.2bn at the end of the year. Total

allowances in respect of the oil and gas portfolio were

$0.6bn.

The sector remains under enhanced monitoring with risk

appetite and new lending has been significantly curtailed.

Metals and mining

Metals prices declined during 2015 although the pace and

extent of the price decline was more gradual than for oil

and gas.

Precious metals, copper, nickel and zinc prices are generally

forecast to improve slightly in 2016. The outlook for steel,

aluminium and bulk metals is more negative due to a

combination of oversupply and reduction in demand. The

low oil and gas prices benefit most metals and mining

customers given that they are large consumers of energy.

Our total drawn risk exposure to metals and mining was

$18bn (steel and aluminium $9bn, copper, nickel and zinc

$4bn, iron ore and metallurgical coal $3bn, precious metals

$2bn). Individually assessed loan impairments were $0.1bn.

Given the pressures in metals prices the metals and mining

sector is under heightened management review.

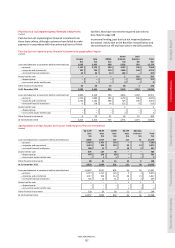

Mainland China exposures

Mainland China’s economic growth rate slowed in 2014 and

2015 with a gross domestic product of 6.9% in 2015

compared with 7.3% in 2014 (2013: 7.7%). China’s economic

growth rate remains very strong when compared with

developed western economies. Although the largest foreign

bank in China, HSBC’s overall lending market share is very

small at about 0.2%. This allows us to be selective in our

lending to mainland China-related exposures, targeting high

quality lending centred around specific priority sectors.

The portfolio has continued to perform well with loan

impairment charges remaining at their existing low levels.

The total mainland China portfolio had drawn risk exposures

of $143bn, of which $77bn was booked onshore, with the

remainder mainly booked in Hong Kong. Retail lending

amounted to $8bn, focused primarily on residential

mortgages in selected geographical areas. Wholesale lending

amounted to $135bn. 51% of the wholesale portfolio was

corporate lending with 26% to banks and the remainder to

China sovereign. The lending to banks was 99% investment

grade. The corporate portfolio was also of high quality with

62% of the portfolio of investment grade. Only 2% of the

corporate portfolio was rated substandard which compares

favourably with the Group as a whole. The corporate

portfolio was well diversified with less than 40% of lending to

state owned enterprises. The corporate real estate portfolio

amounted to about $15bn. This portfolio which is primarily

focused on tier 1 and tier 2 cities and the Pearl River Delta,

was managed carefully under a series of caps ensuring that

the lending to this sector remained within our risk appetite.

Our resultant ability to be selective in our lending and apply

our traditionally strong underwriting standards means we

have a high quality portfolio which we would expect to be

resilient even in a situation where mainland China’s growth

rate slows further.