HSBC 2015 Annual Report Download - page 157

Download and view the complete annual report

Please find page 157 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

HSBC HOLDINGS PLC

155

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

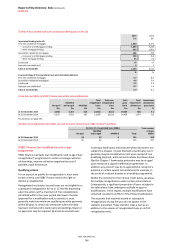

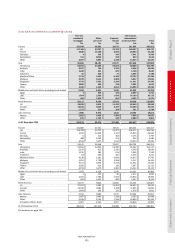

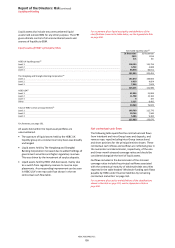

Liquidity and funding

Liquidity risk is the risk that the Group will not have

sufficient financial resources to meet its obligations as

they fall due, or will have to do so at an excessive cost.

The risk arises from mismatches in the timing of cash

flows.

The risk arises when the funding needed for illiquid

asset positions cannot be obtained at the expected

terms and when required.

A summary of our current policies and practices regarding liquidity

and funding is provided in the Appendix to Risk on page 204.

Liquidity and funding risk management framework

The objective of our liquidity framework is to allow us to

withstand very severe liquidity stresses. It is designed to be

adaptable to changing business models, markets and

regulations.

Our Liquidity and Funding Risk Management Framework

(‘LFRF’) requires:

• liquidity to be managed by operating entities on a

stand-alone basis with no implicit reliance on the Group

or central banks;

• all operating entities to comply with their limits for the

advances to core funding ratio; and

• all operating entities to maintain a positive stressed

cash flow position out to three months under prescribed

Group stress scenarios.

Liquidity and funding in 2015

The liquidity position of the Group remained strong in

2015. Our ratio of customer advances to customer deposits

was 72% (2014: 72%). Both customer loans and customer

accounts fell on a reported basis with these movements

including:

• the transfer to ‘Assets held for sale’ and ‘Liabilities of

disposal groups held for sale’ of balances relating to the

planned disposal of our operations in Brazil;

• a reduction in corporate overdraft and current account

balances relating to a small number of clients in our

Payments and Cash Management business in the UK

who settled their overdraft and deposit balances on a

net basis, with customers increasing the frequency with

which they settled their positions; and

• movements in currency markets, which changed the

value of our customer loans and customer accounts

when translated from their local currency into US

dollars.

The HSBC UK liquidity group recorded an increase in

its advances to core funding (‘ACF’) ratio to 101%

at 31 December 2015 (2014: 97%), mainly because of

higher wholesale lending while core funding remained

unchanged.

The Hongkong and Shanghai Banking Corporation recorded

a decrease in its ACF ratio to 69% at 31 December 2015

(2014: 75%), mainly because of an increase in core deposits

coupled with a decrease in corporate loans.

HSBC USA recorded a decrease in its ACF ratio to 89%

at 31 December 2015 (2014: 100%), mainly because of

growth in core funding, which was partially offset by higher

loans to customers.

The HSBC UK liquidity group, The Hongkong and Shanghai Banking

Corporation and HSBC USA are defined in footnotes 19 to 21 on

page 191. The ACF ratio is discussed on page 205.

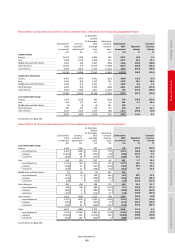

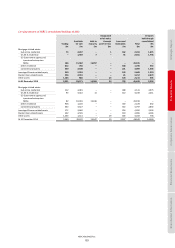

Wholesale senior funding markets

Conditions in the bank wholesale debt markets were

generally positive in 2015. Periods of volatility remained,

however, particularly during the latter months of the year

when concerns over the decline in oil prices and economic

growth in Europe and mainland China combined with a

variety of other factors to leave the outlook uncertain,

affecting market confidence.

In 2015, a number of Group entities issued the equivalent

of $22bn (2014: $20bn) of long-term debt securities in the

public capital markets in a range of currencies and

maturities.

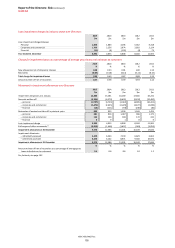

Liquidity regulation

Under European Commission (‘EC’) Delegated Regulation

2015/61, the consolidated liquidity coverage ratio (‘LCR’)

became a minimum regulatory standard from 1 October

2015.

The European calibration of the net stable funding ratio

(‘NSFR’) is still pending following the Basel Committee’s

final recommendation in October 2014, and therefore

external disclosure of this metric is currently on hold.

Non-EU regulators are expected to apply the LCR and NSFR

reporting requirement locally and there is the potential for

local requirements to diverge from the rules applicable to

the Group.

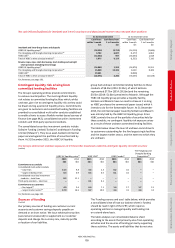

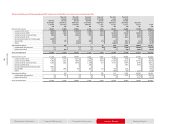

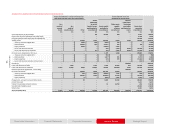

Liquidity coverage ratio – EC LCR Delegated

Regulation

The calculation of the EC LCR metric involves two key

assumptions: the definition of operational deposits and the

ability to transfer liquidity from non-EU legal entities.

• We define operational deposits as transactional

(current) accounts arising from the provision of custody

services by HSBC Security Services or Payments and

Cash Management services, where the operational

component is assessed to be the lower of the current

balance and the separate notional values of debits and

credits across the account in the previous calculation

period.

• No transferability of liquidity from non-EU entities is

assumed other than to the extent currently permitted.

This results in $94bn of high-quality liquid assets

(‘HQLA’) being excluded from the Group’s LCR.

On the basis of these assumptions, we reported to the PRA

a Group EC LCR at 31 December 2015 (on the basis of the

Delegated Regulation) of 116%.

The ratio of total consolidated HQLAs to the EC LCR

denominator at 31 December 2015 was 142%, reflecting

the additional $94bn of HQLAs excluded from the Group

LCR.