HSBC 2015 Annual Report Download - page 208

Download and view the complete annual report

Please find page 208 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

Report of the Directors: Risk (continued)

Appendix to Risk – Policies and practices

HSBC HOLDINGS PLC

206

• the ability to access interbank funding and unsecured term debt markets ceases for the duration of the scenario;

• the ability to generate funds from illiquid asset portfolios (securitisation and secured borrowing) is restricted to 25-75% of

the lower of issues in the last six months or expected issues in the next six months. The restriction is based on current

market conditions and is dependent on the operating entity’s inherent liquidity risk categorisation;

• the ability to access repo funding ceases for any asset not classified as liquid under our liquid asset policy for the duration of

the scenario;

• drawdowns on committed lending facilities must be consistent with the severity of the market stress being modelled and

dependent on the inherent liquidity risk categorisation of the operating entity;

• outflows are triggered by a defined downgrade in long-term ratings. We maintain an ongoing assessment of the appropriate

number of notches to reflect;

• customer loans are assumed to be renewed at contractual maturity;

• interbank loans and reverse repos are assumed to run off contractually; and

• assets defined as liquid assets are assumed to be realised in cash ahead of their contractual maturity, after applying a

defined stressed haircut of up to 20%.

Liquid assets of HSBC’s principal operating entities

Stressed scenario analysis and the numerator of the coverage ratio include the assumed cash inflows that would be generated

from the realisation of liquid assets, after applying the appropriate stressed haircut. These assumptions are made on the basis

of management’s expectation of when an asset is deemed to be realisable.

Liquid assets are unencumbered assets that meet the Group’s definition of liquid assets and are either held outright or as a

consequence of a reverse repo transaction with a residual contractual maturity beyond the time horizon of the stressed

coverage ratio being monitored. Any unencumbered asset held as a result of reverse repo transactions with a contractual

maturity within the time horizon of the stressed coverage ratio being monitored is excluded from the stock of liquid assets and

is instead reflected as a contractual cash inflow.

Our framework defines the asset classes that can be assessed locally as high quality and realisable within one month and

between one month and three months. Each local ALCO has to be satisfied that any asset which may be treated as liquid in

accordance with the Group’s liquid asset policy will remain liquid under the stress scenario being managed to.

Inflows from the utilisation of liquid assets within one month can generally only be based on confirmed withdrawable central

bank deposits or the sale or repo of government and quasi-government exposures generally restricted to those denominated

in the sovereign’s domestic currency. High quality ABSs (predominantly US MBSs) and covered bonds are also included but

inflows assumed for these assets are capped.

Inflows after one month are also reflected for high quality non-financial and non-structured corporate bonds and equities

within the most liquid indices.

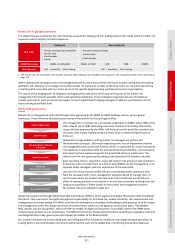

Internal categorisation Cash inflow recognised Asset classes

Level 1 Within one month • Central government

• Central bank (including confirmed withdrawable reserves)

• Supranationals

• Multilateral development banks

• Coins and banknotes

Level 2 Within one month but capped • Local and regional government

• Public sector entities

• Secured covered bonds and pass-through ABSs

• Gold

Level 3 From one to three months • Unsecured non-financial entity securities

• Equities listed on recognised exchanges and within liquid indices

Any entity owned and controlled by central or local/regional government but not explicitly guaranteed is treated as a public

sector entity.

Any exposure explicitly guaranteed is reflected as an exposure to the ultimate guarantor.

In terms of the criteria used to ensure liquid assets are of a high quality, the Group’s liquid asset policy sets out the following

additional criteria:

1. Central bank and central government exposures:

• denominated in the domestic currency of the related sovereign and held:

– onshore in the domestic banking system, qualify as Level 1 liquid assets.