HSBC 2015 Annual Report Download - page 327

Download and view the complete annual report

Please find page 327 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

HSBC HOLDINGS PLC

325

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

When planning the audit, I considered if multiple errors may exist which, when aggregated, could exceed $1,050m. In order to

reduce the risk of multiple errors which could aggregate to this amount I used a lower level of materiality, known as

performance materiality, of $788m to identify the individual balances, classes of transactions and disclosures that were subject

to audit. I asked each of the partners reporting to me on the subsidiaries of HSBC to work to assigned materiality levels

reflecting the size of the operations they audited. These ranged from $67m (HSBC Mexico S.A.) to $840m (The Hongkong and

Shanghai Banking Corporation Limited).

Where the audit identified some items that were not reflected appropriately in the audited financial information, I considered

these items carefully to assess if they were individually or in aggregate material. I reported any such items which exceeded

$50m to the GAC, who were responsible for deciding whether adjustments should be made to the financial statements in

respect of those items. The Directors have concluded that all items which remained unadjusted were not material to the

financial statements, either individually or in aggregate. I agree with their conclusion.

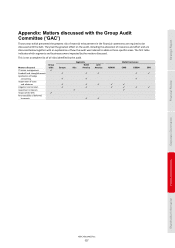

Matters discussed with the GAC

I attended each of the seven GAC meetings held during the year. Part of each meeting involved a discussion with me without

management present. I also met with members of the Committee on an ad hoc basis. During these various conversations we

discussed my observations on a variety of accounting matters, and initial observations on controls over financial reporting.

In November 2014, the Committee held a special meeting to understand and challenge the audit plan. The plan included the

matters which I considered presented the highest risk to the audit and other information on our audit approach such as our

approach to the audit of journals, interest income and financial instrument valuation, and where the latest technology would

be used to obtain better quality audit evidence.

The areas of highest risk to the audit and where I focused most effort and resource, were:

• Access to technology applications and data

• Carrying value of goodwill

• Application of hedge accounting

• Impairment of loans and advances

• Litigation and conduct

• Investment in Bank of Communications Co., Ltd (‘BoCom’)

• Impact of the deferred prosecution agreement (‘DPA’)

• Recoverability of deferred tax assets.

To help you understand their impact on the audit, I have listed them in order of decreasing audit effort. Some of them are

common with other international banks, and some are specific to HSBC. I have included at the end of this report an

explanation of each item, why it was discussed and how the audit approach was tailored to address the concerns.

Going concern

The Directors have made a statement on page 277 regarding going concern. This statement is based on their belief that the

Group and Parent Company intend to, and have sufficient resources to remain in business for 12 months from the date of this

report. I am required to review this statement, and in doing so I have considered HSBC’s budgets, cash flows, capital plan and

stress tests. I have nothing to report as a result of my review. I also have nothing material to add or draw attention to in

relation to the statement.

Other reporting

The Annual Report and Accounts also contains a considerable amount of other information that is required by various

regulators or standard setters. In respect of this information my responsibilities and my reporting are set out in the table

below.