Dollar General 2009 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2009 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

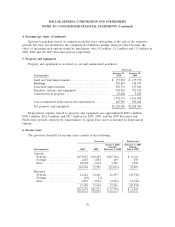

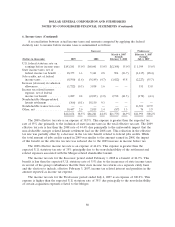

DOLLAR GENERAL CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

7. Current and long-term obligations (Continued)

unutilized commitments under the ABL Facility are equal to or less than 50% of the aggregate

commitments under the ABL Facility. The Company also must pay customary letter of credit fees.

The senior secured credit agreement for the Term Loan Facility requires the Company to prepay

outstanding term loans, subject to certain exceptions, with percentages of excess cash flow, proceeds of

non-ordinary course asset sales or dispositions of property, and proceeds of incurrences of certain debt.

In addition, the senior secured credit agreement for the ABL Facility requires the Company to prepay

the ABL Facility, subject to certain exceptions, with proceeds of non-ordinary course asset sales or

dispositions of property and any borrowings in excess of the then current borrowing base. The Term

Loan Facility can be prepaid in whole or in part at any time.

Beginning September 30, 2009, the Company was required to repay installments on the loans

under the Term Loan Facility in equal quarterly principal amounts in an aggregate amount per annum

equal to 1% of the total funded principal amount at July 6, 2007. During 2009, the Company paid two

such quarterly installments totaling $11.5 million. In addition, in January 2010 the Company voluntarily

prepaid $325 million of the principal balance of the Term Loan Facility, and as a result, no further

quarterly principal installments will be required prior to maturity of the Term Loan Facility on July 6,

2014. The Company incurred a pretax loss of $4.7 million for the write off of debt issuance costs

associated with this prepayment.

All obligations under the Credit Facilities are unconditionally guaranteed by substantially all of the

Company’s existing and future domestic subsidiaries (excluding certain immaterial subsidiaries and

certain subsidiaries designated by the Company under the Credit Facilities as ‘‘unrestricted

subsidiaries’’).

All obligations and guarantees of those obligations under the Term Loan Facility are secured by,

subject to certain exceptions, a second-priority security interest in all existing and after-acquired

inventory and accounts receivable; a first priority security interest in substantially all of the Company’s

and the guarantors’ tangible and intangible assets (other than the inventory and accounts receivable

collateral); and a first-priority pledge of the capital stock held by the Company. All obligations under

the ABL Facility are secured by all existing and after-acquired inventory and accounts receivable,

subject to certain exceptions.

The Credit Facilities contain certain covenants, including, among other things, covenants that limit

the Company’s ability to incur additional indebtedness, sell assets, incur additional liens, pay dividends,

make investments or acquisitions, or repay certain indebtedness.

Under the ABL facility, for the year ended January 29, 2010, the Company had no borrowings or

repayments; for the year ended January 30, 2009, the Company had no borrowings and repayments of

$102.5 million; and for the 2007 Successor period the Company had borrowings of $1.522 billion and

repayments of $1.420 billion. As of January 29, 2010 and January 30, 2009, respectively, the Company

had no borrowings, $85.1 million and $83.7 million of standby letters of credit, and $15.4 million and

$51.0 million of commercial letters of credit, outstanding under the ABL Facility, with excess

availability under the ABL Facility of $930.6 million and $932.8 million.

On July 6, 2007, in conjunction with the Merger, the Company issued $1.175 billion aggregate

principal amount of 10.625% senior notes due 2015 (the ‘‘Senior Notes’’) which were issued net of a

discount of $23.2 million and which mature on July 15, 2015 pursuant to an indenture, dated as of

July 6, 2007 (the ‘‘senior indenture’’), and $725 million aggregate principal amount of 11.875%/12.625%

86