Dollar General 2009 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2009 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

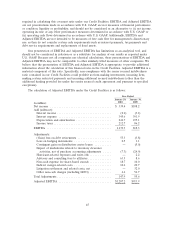

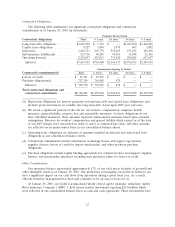

Interest Rate Swaps

We use interest rate swaps to minimize the risk of adverse changes in interest rates. These swaps

are intended to reduce risk by hedging an underlying economic exposure. Because of high correlation

between the derivative financial instrument and the underlying exposure being hedged, fluctuations in

the value of the financial instruments are generally offset by reciprocal changes in the value of the

underlying economic exposure. Our principal interest rate exposure relates to outstanding amounts

under our Credit Facilities. At January 29, 2010, we had interest rate swaps with a total notional

amount of approximately $1.42 billion. For more information see Item 7A ‘‘Quantitative and

Qualitative Disclosures about Market Risk’’ below.

Fair Value Accounting

We have classified our interest rate swaps, as further discussed in Item 7A. below, in Level 2 of

the fair value hierarchy, as the significant inputs to the overall valuations are based on market-

observable data or information derived from or corroborated by market-observable data, including

market-based inputs to models, model calibration to market-clearing transactions, broker or dealer

quotations, or alternative pricing sources with reasonable levels of price transparency. Where models

are used, the selection of a particular model to value a derivative depends upon the contractual terms

of, and specific risks inherent in, the instrument as well as the availability of pricing information in the

market. We use similar models to value similar instruments. Valuation models require a variety of

inputs, including contractual terms, market prices, yield curves, credit curves, measures of volatility, and

correlations of such inputs. For our derivatives, all of which trade in liquid markets, model inputs can

generally be verified and model selection does not involve significant management judgment.

We incorporate credit valuation adjustments to appropriately reflect both our own nonperformance

risk and the respective counterparty’s nonperformance risk in the fair value measurements of our

derivatives. The credit valuation adjustments are calculated by determining the total expected exposure

of the derivatives (which incorporates both the current and potential future exposure) and then

applying each counterparty’s credit spread to the applicable exposure. For derivatives with two-way

exposure, such as interest rate swaps, the counterparty’s credit spread is applied to our exposure to the

counterparty, and our own credit spread is applied to the counterparty’s exposure to us, and the net

credit valuation adjustment is reflected in our derivative valuations. The total expected exposure of a

derivative is derived using market-observable inputs, such as yield curves and volatilities. The inputs

utilized for our own credit spread are based on implied spreads from our publicly-traded debt. For

counterparties with publicly available credit information, the credit spreads over LIBOR used in the

calculations represent implied credit default swap spreads obtained from a third party credit data

provider. In adjusting the fair value of our derivative contracts for the effect of nonperformance risk,

we have considered the impact of netting and any applicable credit enhancements, such as collateral

postings, thresholds, mutual puts, and guarantees. Additionally, we actively monitor counterparty credit

ratings for any significant changes.

As of January 29, 2010, the net credit valuation adjustments reduced the settlement values of our

derivative liabilities by $2.0 million. Various factors impact changes in the credit valuation adjustments

over time, including changes in the credit spreads of the parties to the contracts, as well as changes in

market rates and volatilities, which affect the total expected exposure of the derivative instruments.

When appropriate, valuations are also adjusted for various factors such as liquidity and bid/offer

spreads, which factors we deemed to be immaterial as of January 29, 2010.

46