Dish Network 2004 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2004 Dish Network annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

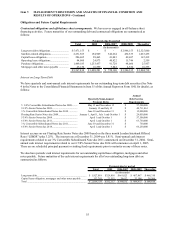

Item 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS - Continued

59

• Valuation of Long-Lived Assets. We evaluate the carrying value of long-lived assets to be held and used,

other than goodwill and intangible assets with indefinite lives, when events and circumstances warrant such

a review. The carrying value of a long-lived asset is considered impaired when the anticipated

undiscounted cash flow from such asset is less than its carrying value. In that event, a loss is recognized

based on the amount by which the carrying value exceeds the fair value of the long-lived asset. Fair value

is determined primarily using the estimated cash flows associated with the asset under review, discounted

at a rate commensurate with the risk involved. Losses on long-lived assets to be disposed of by sale are

determined in a similar manner, except that fair values are reduced for selling costs. Changes in estimates

of future cash flows could result in a write-down of the asset in a future period.

• Valuation of Goodwill and Intangible Assets with Indefinite Lives. We evaluate the carrying value of

goodwill and intangible assets with indefinite lives annually in the fourth quarter, and also when events and

circumstances warrant. We use estimates of fair value to determine the amount of impairment, if any, of

recorded goodwill and intangible assets with indefinite lives. Fair value is determined primarily using the

estimated future cash flows, discounted at a rate commensurate with the risk involved. Changes in our

estimates of future cash flows could result in a write-down of goodwill and intangible assets with indefinite

lives in a future period, which could be material to our consolidated results of operations and financial

position.

• Smart card replacement. We use conditional access technology, including embedding microchips in credit

card-sized access cards, or “smart cards,” to encrypt our programming so only those who pay can receive it.

Our signal encryption has been pirated, allowing illegal receipt of our programming, and our security

systems could be further compromised in the future. Theft of our programming reduces future potential

revenue and increases our net subscriber acquisition costs. In addition, theft of our competitors’

programming can also increase our churn. Compromises of our encryption technology could also adversely

affect our ability to contract for video and audio services provided by programmers. To further combat

piracy and maintain the functionality of active set-top boxes, we are in the process of replacing older

generation smart cards with newer generation smart cards. We have accrued a liability for the replacement

of smart cards in satellite receivers sold to and owned by subscribers based on the estimated number of

cards that will be needed to execute our plan. This estimate is based on a number of variables, including

historical subscriber churn trends and the estimated per card costs for smart card replacements. Changes in,

among other things, the timing of the replacement plan could result in increases or decreases in the smart

card replacement reserve. We expect to complete the replacement of older generation smart cards during

the second half of 2005.

• Allowance for Doubtful Accounts. Management estimates the amount of required allowances for the

potential non-collectibility of accounts receivable based upon past collection experience and consideration of

other relevant factors. However, past experience may not be indicative of future collections and therefore

additional charges could be incurred in the future to reflect differences between estimated and actual

collections.

• Income taxes. Our income tax policy is to record the estimated future tax effects of temporary differences

between the tax bases of assets and liabilities and amounts reported in the accompanying consolidated balance

sheets, as well as operating loss and tax credit carryforwards. We follow the guidelines set forth in Statement

of Financial Accounting Standards No. 109, “Accounting for Income Taxes” regarding the recoverability of

any tax assets recorded on the balance sheet and provide any necessary valuation allowances as required.

Determining necessary valuation allowances requires us to make assessments about the timing of future

events, including the probability of expected future taxable income and available tax planning opportunities.

In accordance with SFAS 109, we periodically evaluate our need for a valuation allowance based on both

historical evidence, including trends, and future expectations in each reporting period. Future performance

could have a significant effect on the realization of tax benefits, or reversals of valuation allowances, as

reported in our results of operations. Reversing our current recorded valuation allowance would have a

material positive impact on our “Net income (loss)” for future periods.