Costco 2005 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2005 Costco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(dollars in thousands, except per share data) (Continued)

Note 1—Summary of Significant Accounting Policies (Continued)

progresses towards earning the rebate or discount and as a component of cost of sales as the merchandise is sold.

Other consideration received from vendors is generally recorded as a reduction of merchandise costs upon com-

pletion of contractual milestones, terms of the related agreement, or by other systematic and rational approach.

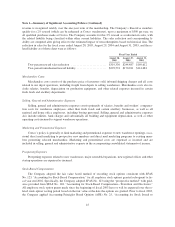

Merchandise Inventories

Merchandise inventories are valued at the lower of cost or market as determined primarily by the retail in-

ventory method, and are stated using the last-in, first-out (LIFO) method for substantially all U.S. merchandise

inventories. Merchandise inventories for all foreign operations are primarily valued by the retail method of ac-

counting, and are stated using the first-in, first-out (FIFO) method. The Company believes the LIFO method

more fairly presents the results of operations by more closely matching current costs with current revenues. The

Company records an adjustment each quarter if necessary, for the expected annual effect of inflation and these

estimates are adjusted to actual results determined at year-end. At August 28, 2005, merchandise inventories val-

ued at LIFO approximated FIFO after considering the lower of cost or market principle. At August 29, 2004,

merchandise inventories valued using LIFO exceeded the comparable FIFO value by approximately $13,410 due

to the aggregate effects of deflation.

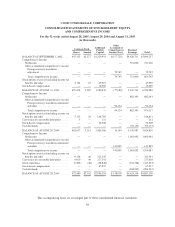

August 28,

2005

August 29,

2004

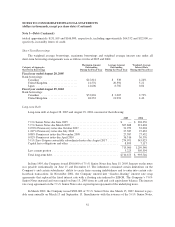

Merchandise inventories consist of:

United States (primarily LIFO) ........................ $3,155,462 $2,903,551

Foreign (FIFO) .................................... 859,237 740,034

Total ........................................ $4,014,699 $3,643,585

The Company provides for estimated inventory losses between physical inventory counts on the basis of a

standard percentage of sales. This provision is adjusted periodically to reflect the actual shrinkage results of the

physical inventory counts, which generally occur in the second and fourth quarters of the Company’s fiscal year.

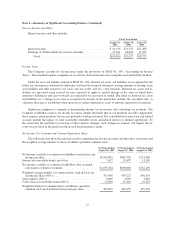

Property and Equipment

Property and equipment are stated at cost. Depreciation and amortization expenses are computed using the

straight-line method for financial reporting purposes. Buildings are generally depreciated over twenty-five to

thirty-five years; equipment and fixtures are depreciated over three to ten years; leasehold improvements are

amortized over the initial term of the lease or the useful lives of the assets if shorter. The Company capitalizes

certain costs related to the acquisition and development of software and amortizes those costs using the straight-

line method over their estimated useful lives, which range from three to five years.

Interest costs incurred on property during the construction period are capitalized. The amount of interest

costs capitalized was $7,226 in fiscal 2005, $4,155 in fiscal 2004, and $3,272 in fiscal 2003.

Impairment of Long-Lived Assets

The Company periodically evaluates the realizability of long-lived assets for impairment when management

makes the decision to relocate or close a warehouse or when events or changes in circumstances occur, which

may indicate the carrying amount of the asset may not be recoverable. The Company evaluates the carrying value

of the asset by comparing the estimated future undiscounted cash flows generated from the use of the asset and

42