Cincinnati Bell 2011 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2011 Cincinnati Bell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

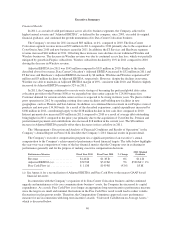

Although shareholders and proxy advisory companies tend to focus on “total shareholder return” (“TSR”) as

a major factor in judging a Company’s performance, we have historically adopted other measures of the

Company’s financial performance on the theory that using TSR as a financial metric might encourage a focus on

short-term results. For example, at a time when its core telecommunications business faced intense competitive

challenges, the Company has used its capital to seize the opportunity to become the premier data center

colocation provider to Fortune 1000 companies rather than pay dividends to its shareholders, which could be

detrimental to the Company’s long-term strategic opportunities. In addition, as a result of the scope of the

Company’s historical debt obligations and external economic factors (e.g., sovereign debt fears), the market price

of the Company’s common shares has been volatile and has not always fully reflected the Company’s operating

results and performance. Finally, the Committee questions the appropriateness of TSR as a financial metric given

its tendency to be influenced by external factors. As a result, the Company used the foregoing financial metrics to

measure its performance in 2011.

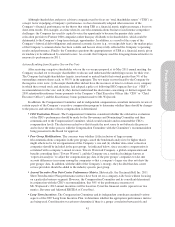

Actions Resulting from Negative Say-on-Pay Vote

After receiving a negative shareholder vote on the say-on-pay proposal at its May 2011 annual meeting, the

Company reached out to its major shareholders to discuss and understand the underlying reasons for their vote.

The Company had eight shareholders (equity, investment or mutual funds) that owned greater than 5% of the

outstanding common shares each, or 58.5% in the aggregate. The two major reasons heard by the Company for

the negative votes were: (i) the major shareholders did not have the resources or time to evaluate every company

in which they owned stock and, therefore, had adopted a policy of following ISS Corporate Services’ (“ISS”)

recommendation for the vote; and (ii) they did not understand the disclosures concerning, or did not support, the

2010 retention/discretionary bonus payments to the Company’s Chief Executive Officer (the “CEO” or “Chief

Executive Officer”) and the discretionary bonus payment made to Mr. Wojtaszek.

In addition, the Compensation Committee and its independent compensation consultant initiated a review of

certain aspects of the Company’s executive compensation program to determine whether there should be changes

to the process and substance of how compensation is determined.

•CEO Evaluation Process. The Compensation Committee considered whether the substantive evaluation

of the CEO’s performance should be made by the Governance and Nominating Committee and then

communicated to the Compensation Committee, which would consider and recommend the CEO’s

compensation levels. The decision reached was that it made the most sense to not bifurcate the process

and to leave the entire process with the Compensation Committee with the Committee’s recommendation

being presented to the Board for approval.

•Peer Group Modifications. The concerns were whether (i) the inclusion of large revenue

telecommunications companies in the peer groups caused the benchmark analysis to be higher than it

might otherwise be for an organization of the Company’s size and (ii) whether data center colocation

companies should be included in the peer groups. As indicated below, since executive compensation is

correlated with a company’s annual revenue, Towers Watson & Company, a global compensation and

benefits consulting firm (“Towers Watson”), and the Company use a statistical technique known as

“regression analysis” to adjust the compensation pay data of the peer groups’ companies to take into

account differences in revenue among the companies so that a company’s larger size does not skew the

peer groups’ data. In addition, with the shift of the Company’s strategy, they decided that data center

service providers should be added to the industry specific peer group.

•Annual Incentive Plan Data Center Performance Metrics. Historically, the Cincinnati Bell Inc. 2011

Short Term Incentive Plan performance metrics have been set on a company-wide basis without focusing

on a particular business segment. However, the Compensation Committee and its consultant determined,

in conjunction with the CEO’s recommendation, that 50% of the performance measures of

Mr. Wojtaszek’s 2012 annual incentives will be based on CyrusOne financial results (spread over two

metrics, Revenue and Adjusted EBITDA of CyrusOne).

•Long-Term Incentives. The Compensation Committee and its independent consultant examined various

aspects of the 2007 Long Term Incentive Plan, to determine whether the appropriate performance metrics

are being used. Consideration was given to determine if there is a proper correlation between risk and

41

Proxy Statement