Cincinnati Bell 2011 Annual Report Download - page 164

Download and view the complete annual report

Please find page 164 of the 2011 Cincinnati Bell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

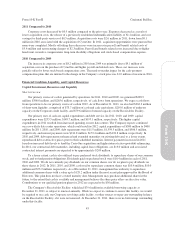

Management believes that cash on hand, cash generated from operations, and cash from its credit facilities

will be adequate to meet the Company’s investing and financing needs for 2012.

Long-term view, including debt covenants

As of December 31, 2011, the Company had $2.5 billion of outstanding indebtedness and an accumulated

deficit of $3.2 billion. A significant amount of indebtedness was previously incurred from the purchase and

operation of a national broadband business, which was sold in 2003.

In addition to the uses of cash described in the Short-term view section above, the Company has significant

long-term debt maturities that come due after 2012. Contractual debt maturities, including capital lease

obligations, are $18.9 million in 2013, $6.3 million in 2014, $253.2 million in 2015, $6.0 million in 2016 and

$2.2 billion thereafter. In addition, we have ongoing obligations to fund our qualified pension plans. Based on

current legislation and current actuarial assumptions, we estimate these contributions to approximate $200

million over the period from 2012 to 2019. It is also possible that we will use a portion of our cash flows for

de-leveraging in the future, including discretionary, opportunistic repurchases of debt prior to their scheduled

maturities.

The Corporate revolving credit facility, which expires in June 2014, contains financial covenants that

require us to maintain certain leverage and interest coverage ratios, and limits our cumulative spending on capital

expenditures. For the period from October 1, 2011 to June 11, 2013, capital expenditures are permitted as long as

they do not exceed $1.0 billion in the aggregate. The facility also has certain covenants, which, among other

things, limit our ability to incur additional debt or liens, pay dividends, repurchase Company common stock, sell,

transfer, lease, or dispose of assets, and make investments or merge with another company. If the Company were

to violate any of its covenants and were unable to obtain a waiver, it would be considered a default. If the

Company were in default under its credit facility, no additional borrowings under the credit facility would be

available until the default was waived or cured. The Company is in compliance and expects to remain in

compliance with its Corporate credit facility covenants.

Various issuances of the Company’s public debt, which include the 7% Senior Notes due 2015, the 8

1

⁄

4

%

Senior Notes due 2017, the 8

3

⁄

4

% Senior Subordinated Notes due 2018, and the 8

3

⁄

4

% Senior Notes due 2020,

contain covenants that, among other things, limit the Company’s ability to incur additional debt or liens, pay

dividends or make other restricted payments, sell, transfer, lease, or dispose of assets and make investments or

merge with another company. The Company is in compliance and expects to remain in compliance with its

public debt indentures.

The Company’s most restrictive covenants are generally included in its Corporate credit facilities. In order to

continue to have access to the amounts available to it under the Corporate revolving credit facility, the Company

must remain in compliance with all covenants. The following table presents the calculation of the most restrictive

debt covenant, the Consolidated Total Leverage Ratio, as of and for the year ended December 31, 2011:

(dollars in millions)

Consolidated Total Leverage Ratio as of December 31, 2011 ......... 4.75

Maximum ratio permitted for compliance ........................ 6.00

Consolidated Funded Indebtedness additional availability ........... $ 659.9

Consolidated EBITDA clearance over compliance threshold ......... $ 110.0

Definitions and components of this calculation are detailed in our credit agreement and can be found in the

Company’s Form 8-K filed June 11, 2010 and Form 8-K filed on November 3, 2011.

In various issuances of the Company’s public debt indentures, a financial covenant exists that permits the

incurrence of additional Indebtedness up to a 4:00 to 1:00 Consolidated Adjusted Senior Debt to EBITDA ratio

(as defined by the individual indentures). Once this ratio exceeds 4:00 to 1:00, the Company is not in default;

however, additional Indebtedness may only be incurred in specified permitted baskets, including a Credit

Agreement basket providing full access to the Corporate revolving credit facility. Also, the Company’s ability to

46

Form 10-K Part II Cincinnati Bell Inc.