Cigna 2010 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2010 Cigna annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

CIGNA CORPORATION 2010 Form 10K 69

PART II

ITEM 7 Management’s Discussion and Analysis of Financial Condition and Results of Operations

Market Risk

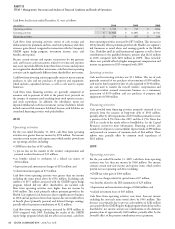

Financial Instruments

e Company’s assets and liabilities include fi nancial instruments

subject to the risk of potential losses from adverse changes in market

rates and prices. e Company’s primary market risk exposures are:

•Interest-rate risk on fi xed-rate, domestic, medium-term

instruments. Changes in market interest rates aff ect the value of

instruments that promise a fi xed return and impact the value of

liabilities for reinsured GMDB and GMIB contracts.

•Foreign currency exchange rate risk of the U.S. dollar primarily

to the South Korean won, euro, Taiwan dollar, British pound, New

Zealand dollar, and Hong Kong dollar. An unfavorable change in

exchange rates reduces the carrying value of net assets denominated

in foreign currencies.

•Equity price risk for domestic equity securities and for the value of

reinsured GMDB and GMIB contracts resulting from unfavorable

changes in variable annuity account values based on underlying

mutual fund investments.

For further discussion of reinsured contracts, see Note 7 for GMDB

contracts and Note 11 for GMIB contracts in the Consolidated

Financial Statements.

e Company’s Management of Market Risks

e Company predominantly relies on three techniques to manage

its exposure to market risk:

•Investment/liability matching. e Company generally selects

investment assets with characteristics (such as duration, yield,

currency and liquidity) that correspond to the underlying

characteristics of its related insurance and contractholder liabilities

so that the Company can match the investments to its obligations.

Shorter-term investments support generally shorter-term life and

health liabilities. Medium-term, fi xed-rate investments support

interest-sensitive and health liabilities. Longer-term investments

generally support products with longer pay out periods such as

annuities and long-term disability liabilities.

•Use of local currencies for foreign operations. e Company

generally conducts its international business through foreign

operating entities that maintain assets and liabilities in local

currencies. While this technique does not reduce the Company’s

foreign currency exposure of its net assets, it substantially limits

exchange rate risk to those net assets.

•Use of derivatives. e Company generally uses derivative fi nancial

instruments to minimize certain market risks.

See Notes 2(C) and 13 to the Consolidated Financial Statements

for additional information about fi nancial instruments, including

derivative fi nancial instruments.

Eff ect of Market Fluctuations on the Company

e examples that follow illustrate the eff ect of hypothetical changes

in market rates or prices on the fair value of certain fi nancial

instruments including:

•hypothetical changes in market interest rates, primarily for fi xed

maturities and commercial mortgage loans, partially off set by

liabilities for long-term debt and GMIB contracts;

•hypothetical changes in market rates for foreign currencies,

primarily for the net assets of foreign subsidiaries denominated in a

foreign currency; and

•hypothetical changes in market prices for equity exposures,

primarily for equity securities and GMIB contracts.

In addition, hypothetical eff ects of changes in equity indices and

foreign exchange rates are presented separately for futures contracts

used in the GMDB equity hedge program.

Management believes that actual results could diff er materially from

these examples because:

•these examples were developed using estimates and assumptions;

•changes in the fair values of all insurance-related assets and liabilities

have been excluded because their primary risks are insurance rather

than market risk;

•changes in the fair values of investments recorded using the

equity method of accounting and liabilities for pension and other

postretirement and postemployment benefi t plans (and related

assets) have been excluded, consistent with the disclosure guidance;

and

•changes in the fair values of other signifi cant assets and liabilities

such as goodwill, deferred policy acquisition costs, taxes, and

various accrued liabilities have been excluded; because they are not

fi nancial instruments, their primary risks are other than market risk.

e eff ects of hypothetical changes in market rates or prices on the

fair values of certain of the Company’s fi nancial instruments, subject

to the exclusions noted above (particularly insurance liabilities),

would have been as follows as of December 31:

Market scenario for certain non-insurance nancial instruments (in millions)

Loss in fair value

2010 2009

100 basis point increase in interest rates $ 700 $ 700

10% strengthening in U.S. dollar to foreign currencies $ 190 $ 160

10% decrease in market prices for equity exposures $ 50 $ 50

e Company’s foreign operations hold investment assets, such

as fi xed maturities, that are generally invested in the currency of

the related liabilities. Due to the increase in the fair value of these

investments in 2010, which are primarily denominated in the South

Korean won, the eff ect of a hypothetical 10% strengthening in U.S.

dollar to foreign currencies at December 31, 2010 was greater than

that eff ect at December 31, 2009.