Bed, Bath and Beyond 2011 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2011 Bed, Bath and Beyond annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

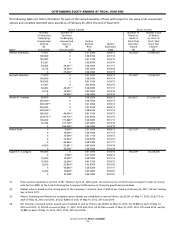

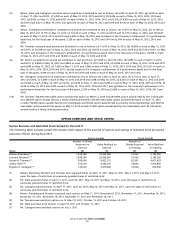

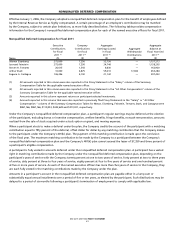

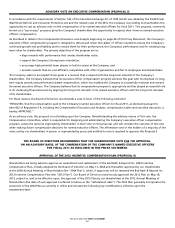

BED BATH & BEYOND PROXY STATEMENT

69

Incentive Stock Options. The grant or exercise of an ISO generally has no income tax consequences for the optionee or the

Company. No taxable income results to the optionee upon the grant or exercise of an ISO. However, the amount by which the

fair market value of the stock acquired pursuant to the exercise of an ISO exceeds the exercise price is an adjustment item and

will be considered income for purposes of alternative minimum tax.

The aggregate fair market value of common stock (determined at the time of grant) with respect to which ISOs can be

exercisable for the first time by an optionee during any calendar year cannot exceed $100,000. Any excess will be treated as a

non-qualified stock option.

The sale of common stock received pursuant to the exercise of an option that satisfied all of the ISO requirements, as well as

the holding period requirement described below, will result in a long-term capital gain or loss equal to the difference between

the amount realized on the sale and the exercise price. To receive ISO treatment, an optionee must be an employee of the

Company (or certain subsidiaries) at all times during the period beginning on the date of the grant of the ISO and ending on

the day three months before the date of exercise, and the optionee must not dispose of the common stock purchased pursuant

to the exercise of an option either (i) within two years from the date the ISO was granted, or (ii) within one year from the

date of exercise of the ISO. Any gain or loss realized upon a subsequent disposition of the shares will be treated as a long-term

capital gain or loss to the optionee (depending on the applicable holding period). The Company will not be entitled to a tax

deduction upon such exercise of an ISO, or upon a subsequent disposition of the shares, unless such disposition occurs prior to

the expiration of the holding period described above.

In general, if the optionee does not satisfy the foregoing holding periods, any gain (in an amount equal to the lesser of the fair

market value of the common stock on the date of exercise (or, with respect to officers subject to Section 16(b) of the Exchange

Act, the date that sale of such common stock would not create liability, referred to as Section 16(b) liability, under Section 16(b)

of the Exchange Act) minus the exercise price, or the amount realized on the disposition minus the exercise price) will constitute

ordinary income. In the event of such a disposition before the expiration of the holding periods described above, subject to

the limitations under Code Sections 162(m) and 280G (as described below), the Company is generally entitled to a deduction at

that time equal to the amount of ordinary income recognized by the optionee. Any gain in excess of the amount recognized

by the optionee as ordinary income would be taxed to the optionee as short-term or long-term capital gain (depending on the

applicable holding period).

Section 16(b). Any of our officers and directors subject to Section 16(b) of the Exchange Act may be subject to Section 16(b)

liability with regard to both ISOs and non-qualified stock options as a result of special tax rules regarding the income tax

consequences concerning their stock options.

Section 162(m) of the Code. Section 162(m) of the Code denies a deduction to any publicly held corporation for compensation

paid to certain “covered employees” in its taxable year to the extent that such compensation exceeds $1,000,000 and is not

“performance-based compensation.” “Covered employees” are a company’s chief executive officer on the last day of the

taxable year and the three other most highly paid executive officers (other than the chief financial officer) whose compensation

is required to be reported to stockholders in its proxy statement under the Exchange Act. Compensation paid to covered

employees as a result of the exercise of non-qualified stock options granted in accordance with the terms of the 2012 Plan are

intended to be “performance-based compensation” enabling the Company to receive a deduction for the full amount of such

compensation without regard to the $1,000,000 cap.

Parachute Payments. In the event that the payment of any award under the 2012 Plan is accelerated because of a change in

ownership (as defined in Code Section 280G(b)(2)) and such payment of an award, either alone or together with any other

payments made to the certain participants, constitutes parachute payments under Section 280G of the Code, then, subject to

certain exceptions, a portion of such payments would be nondeductible to the Company and the participant would be subject

to a 20% excise tax on such portion.

Section 409A of the Code. Section 409A provides that all amounts deferred under a nonqualified deferred compensation

plan are includible in a participant’s gross income to the extent such amounts are not subject to a substantial risk of forfeiture,

unless certain requirements are satisfied. If the requirements are not satisfied, in addition to current income inclusion, interest