Airtran 2010 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2010 Airtran annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

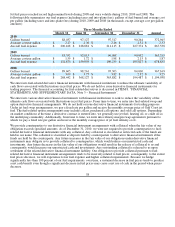

We have variable interests in our aircraft leases. The lessors are trusts established specifically to purchase, finance, and

lease aircraft to us. The trusts are considered variable interest entities (VIEs) and in accordance with the guidance

provided under Financial Accounting Standards Board Accounting Standards Codification 810 “Consolidation”

(Consolidation Topic), we are required to assess if we are the primary beneficiary of these VIE’s. The assessment

considers both quantitative and qualitative factors, including whether we have the power to direct the activities of the VIE,

including but not limited to, determine or limiting the scope or purpose of the VIE, selling or transferring property owned

or controlled by the VIE or arranging financing for the VIE. We also considered whether we had the obligation to absorb

the losses of, or the right to receive benefits from, the VIE.

Our leases generally contain lease terms which are consistent with market terms at the inception of the lease and do not

include a residual value guarantee, a fixed-price purchase option, or similar feature that obligates us to absorb decreases in

value or entitles us to participate in increases in the value of the aircraft. However, we have two aircraft leases that contain

fixed-price purchase options that allow us to purchase the aircraft at predetermined prices on specified dates during the

lease term. Even taking into consideration these purchase options, we are not the primary beneficiary based on our cash

flow analysis, and we do not have the risk of gain or loss or the power to direct the activities of the trust.

We have concluded that we are not the primary beneficiary of any of the trusts and, therefore, we have not consolidated

any of the trusts.

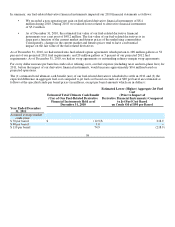

Critical Accounting Policies and Estimates

General. The discussion and analysis of our financial condition and results of operations is based upon our Consolidated

Financial Statements, which have been prepared in accordance with accounting principles generally accepted in the

United States. The preparation of these financial statements requires us to make estimates and judgments that affect the

reported amount of assets and liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities

at the date of our financial statements.

Our actual results may differ from these estimates under different assumptions or conditions. Critical accounting policies

are defined as those that are reflective of significant judgments and uncertainties and are sufficiently sensitive to result in

materially different results under different assumptions and conditions. The following is a description of what we believe

to be our most critical accounting policies and estimates. See Notes to the Consolidated Financial Statements for a

description of our financial accounting policies.

Revenue Recognition. Passenger revenue is recognized when transportation is provided. Ticket sales for transportation

which has not yet been provided are recorded as air traffic liability. Air traffic liability represents tickets sold for future

travel dates. The balance of the air traffic liability fluctuates throughout the year based on seasonal travel patterns and fare

sale activity. Passenger revenue accounting is inherently complex and the measurement of the air traffic liability is subject

to some uncertainty.

A nonrefundable ticket expires at the date of scheduled travel unless the customer exchanges the ticket in advance of such

date for a credit to be used by the customer as a form of payment for another ticket. We recognize as revenue the value of

a non-refundable ticket at the date of scheduled travel unless the customer exchanges his or her ticket for credit. A percent

of credits expire unused. We recognize as revenue over time, in proportion to the credits that are used, the value of credits

that we expect to go unused based on historical experience. Estimating the amount of credits that will go unused involves

some level of subjectivity and judgment. Changes in our estimate of the amount of unused credits could have an effect on

our revenues.

54