United Healthcare 2006 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2006 United Healthcare annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

compensation cost on the termination of employment if, absent the acceleration, the award would have been

forfeited pursuant to its original terms. Under FAS 123, the performance targets were taken into

consideration when determining the expected term of the award and therefore the acceleration of vesting was

not considered to be a modification of the terms.

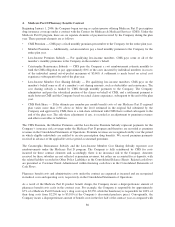

Other Modifications of Option Terms. The Company has also determined that certain other actions were taken

that resulted in the modification of option terms, as follows:

•Options Modified Upon Terminations. On approximately 75 occasions from 1998 to 2005, the Company

entered into amended employment or separation agreements with employees that resulted in the modification

of vesting or cancellation terms of their stock option agreements. Under APB 25, the potential compensation

expense of the modification should have been measured at the date of the modification and recognized if the

employee ultimately received a benefit on the termination date. Under FAS 123, the modification should have

been recognized at the date of the modification based upon the incremental fair value provided to the

employee.

•1999 Cancellation and Reissuance of Options. In the fourth quarter of 1999, the Company issued stock

options to acquire an aggregate of 400,000 shares of Company common stock (3.2 million shares on a split-

adjusted basis) to approximately 65 employees in exchange for the cancellation of an equal number of stock

options that had previously been granted to those employees at various times earlier in 1999. The reissued

stock options had a stated grant date of October 13, 1999 and an exercise price equal to $40.125 ($5.0156 on

a split-adjusted basis), which was lower than the exercise price of the cancelled options. The Company has

determined that, under APB 25, this constituted a “re-pricing”, resulting in variable accounting for each

option until exercise, forfeiture or expiration. Additionally, the Company has concluded that, under FAS 123,

this would also be viewed as a modification to the award and the incremental fair value in addition to the

originally measured fair value should have been recognized over the remaining vesting period.

Related Tax Adjustments. The restatement in this Form 10-K also reflects the estimated loss of certain tax

deductions and additional interest expense related to the exercise of stock options granted to certain of the

Company’s executive officers that — as a result of the revision of measurement dates — no longer qualify as

deductible performance-based compensation in accordance with Internal Revenue Code section 162(m).

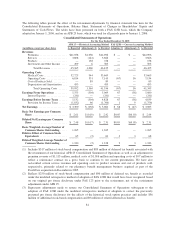

Restatement Adjustments

The following table sets forth, on a year-by-year basis, the impact under FAS 123R and APB 25 of recognizing

additional stock-based compensation expense and related tax effects as a result of historic stock option practices

as well as immaterial adjustments unrelated to historic stock option practices that were identified through a

review of the Company’s accounting practices. The impact under FAS 123R of all errors is $43 million ($57

million net of tax) in 2005, $40 million ($44 million net of tax) in 2004, and an aggregate of $453 million ($313

million net of tax) for 2003 and all prior years. The impact under APB 25 of all errors is $304 million ($238

million net of tax) in 2005, $200 million ($158 million net of tax) in 2004, and an aggregate of $1,056 million

($738 million net of tax) for 2003 and all prior years.

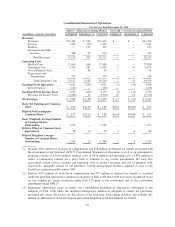

Additionally, on January 1, 2006, our Uniprise business segment began reporting premiums and expenses on a

gross basis for a large account where we have employed third-party reinsurance. Historically, revenues and

expenses associated with this account were reported net of amounts ceded to an unaffiliated reinsurer. While the

reinsurance contract has been in place for a number of years, recent accounting interpretations suggest this

reinsurance arrangement be presented on a gross versus net basis. Prior period amounts have been restated to

conform to the 2006 presentation. The restatement has no effect on our net earnings or shareholders’ equity as

previously reported.

77