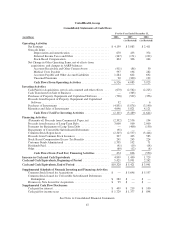

United Healthcare 2006 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2006 United Healthcare annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

date. In 2002, the Company changed to a practice of determining grant dates for new hires and promotions to

be the date of the lowest closing price of the Company’s common stock between the start date of employment

or date of promotion and the end of the quarter in which the employee started work or was promoted. The

Company historically used these stated grant dates as the measurement dates for accounting purposes.

The Company has concluded that the measurement dates used with respect to nearly all of the New Hire and

Promotion Grants during the Independent Review Period were not correct because the Company’s practice

was to determine grant dates with the benefit of hindsight. The Company has determined that the appropriate

measurement date for each New Hire and Promotion Grant was the date on which the Company set the terms

of the award, or where the Company could not identify such date based on all available evidence, the last date

of the fiscal quarter in which a particular New Hire or Promotion Grant was made.

1999 Grant of Supplemental Options. In the fourth quarter of 1999, following a decline in its stock price, the

Company granted “supplemental” stock options to acquire 2.2 million shares of Company common stock (17.6

million shares on a split-adjusted basis) to a broad group of employees, including our former chief executive

officer and other Section 16 officers. The supplemental options were granted in connection with the suspension

of the vesting and exercisability of an equal number of options with exercise prices above $46.50 ($5.8125 on a

split-adjusted basis) that had previously been granted to those employees (the “Suspended Options”). The

supplemental options had a stated grant date of October 13, 1999 and an exercise price equal to $40.125 ($5.0156

on a split-adjusted basis).

After taking into account all available evidence regarding the Suspended Options, the Company has concluded

that, under APB 25, the grant of the supplemental options constituted an effective re-pricing subject to variable

accounting for each option until exercise, forfeiture or expiration. Additionally, the Company has determined

that, under FAS 123, the grant of the supplemental options was a modification that required an incremental fair

value charge to be recognized over the related vesting period.

2000 Reactivation of Suspended Options. In 2000, the Company reactivated the vesting and exercisability of

the Suspended Options. The Company has determined that, under APB 25 and FAS 123, the reactivation of the

vesting and exercisability of the Suspended Options was a new stock option grant that should have had a new

measurement date, and the Company has determined that the appropriate measurement date is the date grantees

were again permitted to exercise their previously vested awards.

Cliff Vesting Options. Prior to April 2000, the Company granted to employees certain stock options that vested

100% on the sixth or ninth anniversary of the date of grant (the “Cliff Vesting Options”). Under the terms of the

options, the Company could elect to accelerate the vesting of all or a portion of the Cliff Vesting Options at its

discretion. The Company followed a policy of accelerating the vesting of a consistent percentage of the Cliff

Vesting Options, unless the option holder was subject to disciplinary action or performing at a less than

satisfactory level. This resulted in nearly all option holders having their Cliff Vesting Options accelerated so that

they actually vested as if they had a 20% or 25% per year time-based vesting schedule (i.e., a four-year or five-

year vesting period).

•Grant of Cliff Vesting Options. Under APB 25, an award should be accounted for as a performance award if

its cliff vesting terms are not considered to be substantive. Based on numerous factors, including evaluation

of employee turnover rates, the Company has determined that the nine-year vesting term was not substantive

in grants after January 1995 to middle management employees. Accordingly, these options should have been

subject to variable accounting until each of their vesting dates. With respect to substantially all other Cliff

Vesting Options, the Company has concluded that the cliff vesting term is substantive.

•Acceleration of Cliff Vesting Options. In accordance with the provisions of Financial Accounting Standards

Board Interpretation No. 44, “Accounting for Certain Transactions Involving Stock Compensation (An

Interpretation of APB Opinion No. 25)” (FIN 44), subsequent to July 1, 2000, the acceleration of the six- or

nine-year cliff vesting term of a stock option constituted a modification. Accordingly, the Company should

have measured the intrinsic value of the award at the date of the modification and recognized this amount as

76