TomTom 2011 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2011 TomTom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

TomTom Annual Report and Accounts 2011

50

Notes to the Consolidated Financial Statements | continued

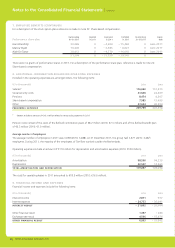

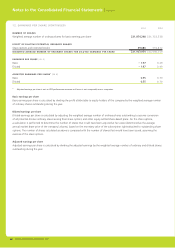

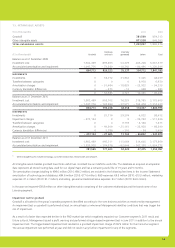

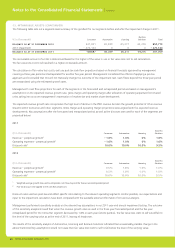

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

The gain or loss arising on disposal or retirement of an item of property, plant and equipment is determined as the difference between

the sales proceeds and the carrying amount of the asset and is recognised in profi t or loss.

Impairment of tangible and intangible assets

Assets, such as goodwill, that have an indefi nite useful life are not subject to amortisation and are tested annually for impairment. Assets

that are subject to amortisation are tested for impairment whenever events or changes in circumstances indicate that the carrying amount

may not be recoverable. An impairment loss is recognised for the amount by which the asset’s carrying amount exceeds its recoverable

amount.

The recoverable amount is the higher of an asset’s fair value, less costs to sell and value in use. In estimating the fair value less costs to

sell, the estimated future cash fl ows are discounted to their present value, using a post-tax discount rate that refl ects current market

assessments of the time-value of money and the risks specifi c to the asset for which the estimates of future cash fl ows have not been

adjusted.

For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifi able cash fl ows

(cash-generating units). Goodwill is tested at the operating segment level.

An impairment loss is recognised immediately in the income statement.

Non-fi nancial assets, other than goodwill that suffered an impairment, are reviewed for possible reversal of the impairment at each

reporting date.

Financial assets

The group classifi es its fi nancial assets in the following categories: at fair value through profi t or loss and loans and receivables.

The classifi cation depends on the purpose for which the fi nancial assets were acquired. Management determines the classifi cation of its

fi nancial assets at initial recognition. The fair values and classifi cation of the fi nancial instruments used by the group are disclosed in note 33.

Regular purchases and sales of fi nancial assets are recognised on the trade date – the date on which the group commits to purchase or sell

the asset.

Financial assets at fair value through profi t or loss

Derivatives are categorised at fair value through profi t or loss unless they are designated as hedges. Derivatives are recorded as fi nancial

assets when their fair value is a positive number; otherwise the derivative is classifi ed as a fi nancial liability.

Financial assets carried at fair value through profi t or loss are initially measured at fair value on the contract date and are marked to fair

value at subsequent reporting dates. Transaction costs are expensed in the income statement. Financial assets are derecognised when the

rights to receive cash fl ows from the investments have expired or have been transferred and the group has transferred substantially all risks

and rewards of ownership.

Gains or losses arising from changes in fair value of derivatives are recognised in income statement in the period in which they arise, except

for derivatives that are highly effective and qualify for cash fl ow hedge accounting.

Loans and receivables

Loans and receivables are non-derivative fi nancial assets with fi xed or determinable payments that are not quoted in an active market.

They are included in current assets, except for maturities greater than twelve months after the balance sheet date, which are classifi ed as

non-current assets. Loans and receivables are measured at amortised cost (if the effect of time value is material) using the effective interest

method, less any impairment. The group’s fi nancial assets classifi ed in the category ‘loans and receivables’ comprise ‘trade receivables’ and

‘cash and cash equivalents’ in the balance sheet (notes 17 and 20).

Inventories

Inventories are stated at the lower of cost and net realisable value. The cost of inventories comprises costs of purchase, assembly and

conversion to fi nished products. The cost of inventories is determined using the fi rst-in, fi rst-out (FIFO) method, net of reserves for

obsolescence and any excess stock. Net realisable value represents the estimated selling price less an estimate of the costs of completion

and direct selling costs.