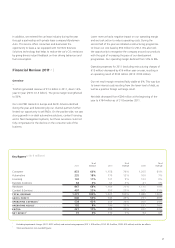

TomTom 2011 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2011 TomTom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

TomTom Annual Report and Accounts 2011

16

solutions, such as smart phone navigation and built in automotive

systems.

The diffi culty to accurately predict the decline in PND demand in

Europe and the US creates uncertainties as to the extent that we

can invest in new technologies and new markets. Any entry into a

new market or a new technology requires substantial investment

prior to break-even being attained.

Non-PND business

The navigation experience for our end-users is similar, whether

the navigation system is built in the dash or provided on a PND.

The dynamics of being a supplier in the automotive industry are,

however, vastly different from those for delivering mass-market

consumer electronics. The design costs of supplying to the

automotive industry present challenges in growing our automotive

business and maintaining profi tability over the longer term.

Some of our digital map competitors have historically been

TomTom customers and can be expected to reduce or cease their

licensing of TomTom maps in the future.

TomTom has seen rapid expansion of its fl eet management

business, although the size of our fl eet management operations is

still relatively small compared to the decline in our PND business.

Geographical sustainability

The North American market presents substantial business

opportunities for the sale of navigation solutions. We view

maintaining, or preferably growing, market share as a vital

component to being successful in the US market.

We may not be able to maintain our volume and profi ts in the

region and our retailer support for our products and services could

decline. Even if we maintain successful market share and average

selling prices in the US, a further slowdown in consumer spending

than anticipated could lead to a volume decrease in the navigation

solutions sold in North America, which would adversely impact

our anticipated revenues and profi ts from the region.

Dependency on GPS satellites

For our navigation products and services we depend on GPS

satellite transmissions to provide position data to our customers.

GPS satellites are funded and maintained by the US government

and we have no control over their maintenance, support or repair.

The free use and availability of GPS signals to the level of accuracy

required for commercial use remains at the sole discretion of the

US government.

GPS signals are carried on radio frequency bands. Any reallocation

of, or interference with, these bands could impair the use of

our products. Alternate systems are all in various stages of

Global economics

The majority of our sales are generated in Europe, which makes

us vulnerable to the debt crisis in the European Union. The US is

also an important market for us; further deterioration in consumer

demand in the US would also have a negative impact on our

fi nancial results.

Any devaluation of the Euro would negatively impact our

profi tability, as the majority of our purchases are made in USD.

Although we use foreign exchange contracts to hedge activities,

these are short term in nature. Any material structural reduction in

the value of the Euro against the US Dollar would have a negative

impact on our profi tability.

Operations could be hindered by potential cash shortages were

it to become more diffi cult to obtain funding from banks that

are short on cash or are regulated in providing loans.

Brand

We use one brand for all of the products and services that we

deliver to market. This leads to brand concentration risk. Factors

that negatively affect our reputation or brand image, such as

adverse consumer publicity, inferior product quality or poor service

could have a material adverse effect on our business, results

of operations or fi nancial condition.

We are constantly striving to increase awareness of our brand and

strengthen our reputation for providing smart, easy-to-use, high-

quality, desirable navigation solutions that meet customer needs

in innovative ways. We aim to enhance our full user experience

through our services and customer support.

Innovation

Our markets are characterised by rapid technological change

requiring the delivery of highly competitive products. We continue

to focus on producing high-quality navigation solutions, however,

there can be no guarantee that our products will compete

successfully against current or new market entrants or competing

technologies.

Our success depends on our ability to rapidly develop and

commercialise new and upgraded products and services; the

timing of releases of these; our ability to accurately forecast

market demand; our product mix relative to that of our

competitors; and our ability to understand and meet changing

consumer preferences.

PND market

A number of factors impact the demand for our PND hardware.

These include the product life cycle, which is approaching a

mature phase. We are therefore experiencing a natural decline

in demand, as well as diffi culty in predicting the replenishment

market and the competitive landscape for alternative navigation

Business Risks | continued