TomTom 2011 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2011 TomTom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

TomTom Annual Report and Accounts 2011

48

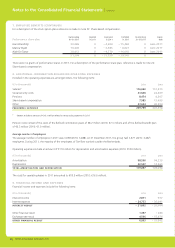

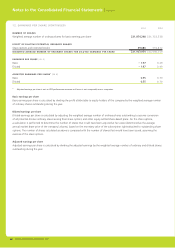

Notes to the Consolidated Financial Statements | continued

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Pension costs

The group operates various defi ned contribution plans and a defi ned benefi t plan for a German subsidiary. For defi ned contribution plans,

the group pays contributions to publicly or privately administered pension insurance plans on a mandatory, contractual or voluntary basis.

The group has no further payment obligations once the contributions have been paid. The contributions are recognised as employee

benefi t expenses when they are due. Prepaid contributions are recognised as an asset to the extent that a cash refund or reduction of

future payments is available.

The assets of the German defi ned benefi t scheme are held separately from those of the group in independently administered funds.

Contributions are charged to the income statement as they become payable, in accordance with the rules of the scheme. The contributions

are included in employee benefi t expense. Full-defi ned benefi t disclosures are not provided given the fact that the plan is not signifi cant.

In Italy, employees are paid a staff leaving indemnity on termination of employment. This is a statutory payment based on Italian civil

law. An amount is accrued each year based on the employee’s remuneration and previously revalued accruals. The indemnity has the

characteristics of a defi ned contribution obligation and is an unfunded, but fully provided liability. The costs of providing benefi ts under the

plans are determined separately for each plan.

Stock compensation expense

The group operates a number of equity-settled plans, as well as a cash-settled performance share plan.

Equity-settled plans

Equity-settled share-based payments are measured at fair value at the date of grant. The fair value determined at the grant date of the

equity-settled share-based payments is expensed on a straight-line basis over the vesting period. The costs are determined based on the

fair value of the granted instruments and the number expected to vest. At each balance sheet date, the entity revises its estimates of

the number of instruments expected to vest.

Performance share plan

Cash-settled share-based payments are initially recognised at the fair value of the liability and are expensed over the vesting period.

The liability is remeasured at each balance sheet date to its fair value, with all changes recognised immediately as either a profi t or

a loss.

Taxation

Income tax expense represents the sum of the tax currently payable and deferred tax. The group’s income tax expense is calculated using

tax rates that have been enacted or substantively enacted at the balance sheet date.

Deferred taxes are calculated using the liability method. Deferred income taxes refl ect the net tax effects of temporary differences between

the carrying amounts of assets and liabilities for fi nancial reporting purposes and the amounts used for income tax purposes. Deferred tax

assets and liabilities are measured using the tax rates expected to apply to taxable income in the years in which those temporary differences

are expected to be recovered or settled, using tax rates (and laws) that have been enacted or substantially enacted by the balance sheet

date. The measurement of deferred tax liabilities and deferred tax assets refl ects the tax consequences that would follow from the manner

in which the group expects, at the balance sheet date, to recover or settle the carrying amount of its assets and liabilities.

Deferred tax assets are recognised when it is probable that suffi cient taxable profi ts will be available against which the deferred tax assets

can be utilised. The carrying amounts of deferred tax assets are reviewed at each balance sheet date and reduced to the extent that it is no

longer probable that suffi cient taxable profi ts will be available to allow all or part of the asset to be recovered.

Current and deferred taxes are recognised as an expense or income in the profi t and loss account, except when they relate to items

credited or debited directly to equity. In this case, the tax is also recognised directly in equity, or where it arises from the initial accounting

for a business combination.

Goodwill

Goodwill represents the excess of the cost of an acquisition over the fair value of the group’s share of the net identifi able assets of the

acquired subsidiary/associate at the date of acquisition.

Goodwill on acquisitions is tested at least annually for impairment and carried at cost less accumulated impairment losses. Goodwill is

allocated to operating segments for the purpose of impairment testing. The allocation is made to those operating segments that are

expected to benefi t from the business combination in which the goodwill arose.