Supercuts 2006 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2006 Supercuts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

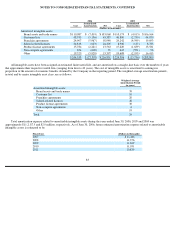

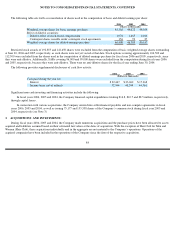

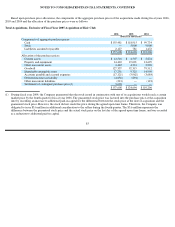

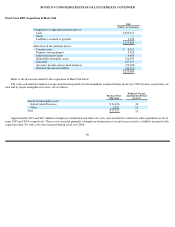

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS, CONTINUED

variability (created by the risks identified in the first step) that the entity is designed to create and pass along to its interest holders. This FSP

should be applied prospectively to all entities with which that enterprise first becomes involved, and to all entities previously required to be

analyzed under FIN 46R when a reconsideration event occurs (as defined by FIN 46R), beginning the first day of the first reporting period

beginning after June 15, 2006 (i.e., the beginning of the Company’s fiscal year 2007). The application of this FSP is not expected to have a

material impact on the Company’s Consolidated Financial Statements.

In June 2006, the EITF reached a consensus on EITF Issue No. 06-3, Disclosure Requirements for Taxes Assessed by a Governmental

Authority on Revenue

-Producing Transactions (EITF No. 06-3). EITF No. 06-3 addresses externally-imposed taxes on revenue-producing

transactions. It mandates disclosure of the accounting policy elected for these taxes (i.e., gross versus net presentation in the income statement),

as well as disclosure of the amount of such taxes by companies following a policy of gross presentation. If ratified by the FASB, this consensus

will be effective for interim and annual periods beginning after December 15, 2006 (i.e., the third quarter of the Company’s fiscal year 2007).

The Company currently presents taxes within the scope of EITF No. 06-3 on a net basis, and has disclosed this policy within its accounting

policy footnote. Other than this additional disclosure requirements, EITF No. 06-3 had no impact on the Company’s Consolidated Financial

Statements.

On July 13, 2006, FASB Interpretation No. 48, Accounting for Uncertainty in Income Taxes—An Interpretation of FASB Statement

No. 109

(FIN 48) , was issued. FIN 48 clarifies the accounting for uncertainty in income taxes recognized in an enterprise’s financial

statements in accordance with FASB Statement No. 109, Accounting for Income Taxes. FIN 48 also prescribes a recognition threshold and

measurement attribute for the financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return.

The new FASB standard provides guidance on derecognition, classification, interest and penalties, accounting in interim periods, disclosure,

and transition. The provisions of FIN 48 are effective for fiscal years beginning after December 15, 2006 (i.e., the third quarter of the

Company’s fiscal year 2007), and the provisions are to be applied to all tax positions upon initial adoption of this standard. Only tax positions

that meet the more-likely-than-not recognition threshold at the effective date may be recognized or continue to be recognized upon adoption of

FIN 48. The cumulative effect of applying the provisions of FIN 48 should be reported as an adjustment to the opening balance of retained

earnings for that fiscal year. The Company is currently evaluating the impact of FIN 48 on the Company’s Consolidated Financial Statements.

81