Cigna 2008 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2008 Cigna annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

100

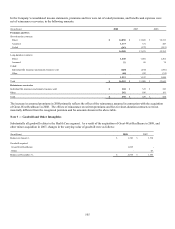

The corresponding impact of prior year development on net income was $7 million in 2008 and $8 million in 2007. The change in the

amount of the incurred claims related to prior years in the medical claims payable liability does not directly correspond to an increase

or decrease in the Company's net income recognized for the following reasons:

First, due to the nature of the Company's retrospectively experience-rated business, only adjustments to medical claims payable on

accounts in deficit affect net income. An increase or decrease to medical claims payable on accounts in deficit, in effect, accrues to

the Company and directly impacts net income. An account is in deficit when the accumulated medical costs and administrative

charges, including profit charges, exceed the accumulated premium received. Adjustments to medical claims payable on accounts in

surplus accrue directly to the policyholder with no impact on the Company’s net income. An account is in surplus when the

accumulated premium received exceeds the accumulated medical costs and administrative charges, including profit charges.

Second, the Company consistently recognizes the actuarial best estimate of the ultimate liability within a level of confidence, as

required by actuarial standards of practice, which require that the liabilities be adequate under moderately adverse conditions. As the

Company establishes the liability for each incurral year, the Company ensures that its assumptions appropriately consider moderately

adverse conditions. When a portion of the development related to the prior year incurred claims is offset by an increase deemed

appropriate to address moderately adverse conditions for the current year incurred claims, the Company does not consider that offset

amount as having any impact on net income.

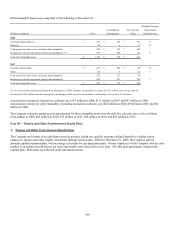

Note 6 — Initiatives to Lower Operating Expenses

The Company has undertaken several initiatives to realign its organization and consolidate support functions in an effort to increase

efficiency and responsiveness to customers.

In 2008, the Company conducted a comprehensive review of its ongoing businesses with an emphasis on reducing operating expenses

in the Health Care segment. As a result of the review, during the fourth quarter of 2008, the Company committed to a plan to reduce

operating costs in order to meet the challenges and opportunities presented by the current market environment. The Company

anticipates the plan will be substantially complete by the end of 2009. As a result, the Company recognized in other operating

expenses a total charge of $55 million pre-tax ($35 million after-tax), which included $44 million pre-tax ($28 million after-tax) for

severance and other related costs resulting from reductions of approximately 1,100 positions in its workforce and $11 million pre-tax

($7 million after-tax) resulting from consolidation of facilities. The Company expects to pay $53 million in cash related to this charge,

most of which will occur in 2009. The Health Care segment reported $44 million pre-tax ($27 million after-tax) of the total charge.

The remainder was reported as follows: Disability and Life: $3 million pre-tax ($2 million after-tax), and International: $8 million

pre-tax ($6 million after-tax).

In the fourth quarter of 2006, the Company completed a review of staffing levels in the health care operations and in supporting areas.

As a result, the Company recognized in other operating expenses a charge for severance costs of $37 million pre-tax ($23 million

after-tax). The Company substantially completed this program in 2007.

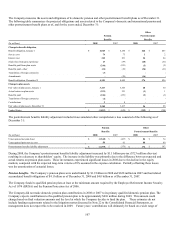

Note 7 ― Guaranteed Minimum Death Benefit Contracts

The Company’s reinsurance operations, which were discontinued in 2000 and are now an inactive business in run-off mode, reinsured

a guaranteed minimum death benefit (GMDB), also known as variable annuity death benefits (VADBe), under certain variable

annuities issued by other insurance companies. These variable annuities are essentially investments in mutual funds combined with a

death benefit. The Company has equity and other market exposures as a result of this product. In periods of declining equity markets

and in periods of flat equity markets following a decline, the Company’s liabilities for these guaranteed minimum death benefits

increase. Conversely, in periods of rising equity markets, the Company’s liabilities for these guaranteed minimum death benefits

decrease.

In order to substantially reduce the equity market exposures relating to guaranteed minimum death benefit contracts, the Company

operates a dynamic hedge program (GMDB equity hedge program), using exchange-traded futures contracts. The hedge program is

designed to offset both positive and negative impacts of changes in equity markets on the GMDB liability. The hedge program

involves detailed, daily monitoring of equity market movements and rebalancing the futures contracts within established parameters.

While the hedge program is actively managed, it may not exactly offset changes in the GMDB liability due to, among other things,

divergence between the performance of the underlying mutual funds and the hedge instruments, high levels of volatility in the equity

markets, and differences between actual contractholder behavior and what is assumed. The performance of the underlying mutual

funds compared to the hedge instruments is further impacted by a time lag, since the data is not reported and incorporated into the