WeightWatchers 2003 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2003 WeightWatchers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

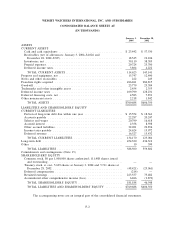

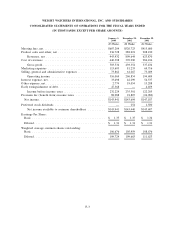

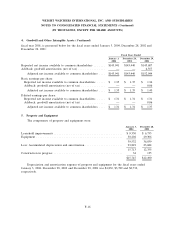

WEIGHT WATCHERS INTERNATIONAL, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(IN THOUSANDS, EXCEPT PER SHARE AMOUNTS)

2. Summary of Significant Accounting Policies (Continued)

Cash Equivalents:

Cash and cash equivalents are defined as highly liquid investments with original maturities of three

months or less. Cash balances may, at times, exceed insurable amounts. The Company believes it

mitigates this risk by investing in or through major financial institutions.

Inventories:

Inventories, which consist of finished goods, are stated at the lower of cost or market on a first-in,

first-out basis, net of reserves for obsolescence and shrinkage.

Property and Equipment:

Property and equipment are recorded at cost. For financial reporting purposes, equipment is

depreciated on the straight-line method over the estimated useful lives of the assets (3 to 10 years).

Leasehold improvements are amortized on the straight-line method over the shorter of the term of the

lease or the useful life of the related assets (generally 5 to 10 years). Expenditures for new facilities

and improvements that substantially extend the useful life of an asset are capitalized. Ordinary repairs

and maintenance are expensed as incurred. When assets are retired or otherwise disposed of, the cost

and related depreciation are removed from the accounts and any related gains or losses are included in

income.

Impairment of Long Lived Assets:

The Company reviews long-lived assets, including finite-lived intangible assets, for impairment

whenever events or changes in business circumstances indicate that the carrying amount of the assets

may not be fully recoverable.

Effective December 30, 2001, the Company adopted Statement of Financial Accounting Standard

(‘‘SFAS’’) No. 144, ‘‘Accounting for the Impairment or Disposal of Long-Lived Assets,’’ which replaces

SFAS No. 121, ‘‘Accounting for the Impairment of Long-Lived Assets to be Disposed Of.’’ SFAS

No. 144 provides updated guidance concerning the recognition and measurement of an impairment loss

for certain types of long-lived assets, expands the scope of a discontinued operation to include a

component of an entity and eliminates the exemption to consolidate when control over a subsidiary is

likely to be temporary. The adoption of this new standard did not have a material impact on the

consolidated financial position, results of operations or cash flows of the Company.

Intangibles Assets:

Effective December 30, 2001, the Company adopted SFAS No. 141, ‘‘Business Combinations’’ and

SFAS No. 142, ‘‘Goodwill and Other Intangible Assets.’’ As a result, the Company is no longer

required to amortize goodwill and other indefinite-lived intangible assets but is required to conduct an

annual review of these assets for potential impairment. Finite-lived intangible assets are amortized

using the straight-line method over their estimated useful lives of three to 20 years.

The Company accounts for software costs under the American Institute of Certified Public

Accountants Statement of Position No. 98-1, ‘‘Accounting for the Costs of Computer Software

Developed or Obtained for Internal Use,’’ which requires capitalization of certain costs incurred in

F-8