WeightWatchers 2003 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2003 WeightWatchers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

base rate plus 1.25%. In addition to paying interest on outstanding principal under the Credit Facility,

we are required to pay a commitment fee to the lenders under the Revolver with respect to the unused

commitments at a rate equal to 0.50% per year.

Our Credit Facility contains covenants that restrict our ability to incur additional indebtedness, pay

dividends on and redeem capital stock, make other restricted payments, including investments, sell our

assets and enter into consolidations, mergers and transfers of all or substantially all of our assets. Our

Credit Facility also requires us to maintain specified financial ratios and satisfy financial condition tests.

Our obligations under the remaining Notes ($15.7 million at January 3, 2004) are subordinate and

junior in right of payment to all of our existing and future senior indebtedness, including all

indebtedness under the Credit Facility. We or our affiliates, including entities related to Artal

Luxembourg, may from time to time, depending on market conditions, purchase the Notes in the open

market or by other means.

In 2003, both Moody’s and Standard and Poor’s upgraded our credit ratings. Our credit ratings by

Moody’s at December 28, 2002 for the Credit Facility and Notes were ‘‘Ba1’’ and ‘‘Ba3,’’ respectively.

On March 20, 2003, Moody’s upgraded its ratings for the Notes to ‘‘Ba2,’’ raised our senior implied

rating to ‘‘Ba1’’ and confirmed its ‘‘Ba1’’ ratings for the Credit Facility. Our credit ratings by

Standard & Poor’s at December 28, 2002 for the Credit Facility and Notes were ‘‘BB-’’ and ‘‘B,’’

respectively. On March 11, 2003, Standard & Poor’s upgraded its corporate credit and Credit Facility

ratings to ‘‘BB’’ and upgraded its rating for the Notes to ‘‘B+ .’’ On July 24, 2003, both Standard &

Poor’s and Moody’s confirmed these aforementioned ratings.

In January 2004, we entered into another refinancing to move a large portion of our debt from

fixed Term Loans to Revolver. This provides us with a greater degree of flexibility and the ability to

more efficiently manage cash. Under the refinancing, our term loans have been reduced from

$454.2 million to $150.0 million and our Revolver capacity has increased from $45.0 million to

$350.0 million. To complete the refinancing, we drew down $310.0 million of the Revolver. In

connection with this refinancing, we incurred expenses of approximately $3.0 million in the first quarter

of 2004.

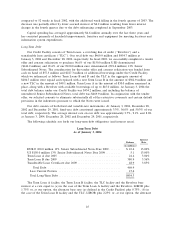

Contractual Obligations

We are obligated under non-cancelable operating leases primarily for office and rent facilities.

Rent expense charged to operations under all our leases for the fiscal year ended January 3, 2004 was

approximately $17.4 million.

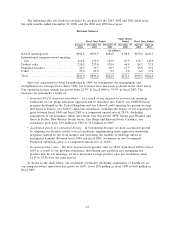

The impact that our contractual obligations as of January 3, 2004 are expected to have on our

liquidity and cash flow in future periods is as follows:

Payment Due by Period

Less than More than

Total 1 Year 1-3 Years 3-5 Years 5 Years

(in millions)

Long-Term Debt ........................... $469.9 $15.6 $21.8 $ 8.6 $423.9

Operating Leases .......................... 78.0 21.5 27.3 11.4 17.8

Total ................................. $547.9 $37.1 $49.1 $20.0 $441.7

Debt obligations due to be repaid in the 12 months following January 3, 2004 are expected to be

satisfied with operating cash flows. We believe that cash flows from operating activities, together with

borrowings available under our Revolver, will be sufficient for the next 12 months to fund currently

anticipated capital expenditure requirements, debt service requirements and working capital

requirements.

26