Volvo 2007 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2007 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

Financial information 2007 91

for at fair value at each reporting date and provided for as an accrued

expense over the vesting period, which is applied for the employee

stock option program. See Note 34.

Pensions and similar obligations (Postemployment benefi ts)

Volvo applies IAS 19, Employee Benefi ts, for pensions and similar

obligations. In accordance with IAS 19, actuarial calculations should

be made for all defi ned-benefi t plans in order to determine the present

value of obligations for benefi ts vested by its current and former

employees. The actuarial calculations are prepared annually and are

based upon actuarial assumptions that are determined close to the

balance sheet date each year. Changes in the present value of obliga-

tions due to revised actuarial assumptions are treated as actuarial

gains or losses which are amortized over the employees’ average

remaining service period to the extent these exceed the corridor value

for each plan. Deviations between expected return on plan assets and

actual return are treated as actuarial gains or losses. Provisions for

post-employment benefi ts in Volvo’s balance sheet correspond to the

present value of obligations at year-end, less fair value of plan assets,

unrecognized actuarial gains or losses and unrecognized unvested

past service costs. See Note 24.

As a supplement to IAS 19, Volvo applies URA 43 in accordance

with the recommendation from the Swedish Financial Accounting

Standards Council in calculating the Swedish pension liabilities.

For defi ned contribution plans premiums are expensed as incurred.

Provisions for residual value risks

Residual value risks are attributable to operational leasing contracts

and sales transactions combined with buy-back agreements or resid-

ual value guarantees. Residual value risks are the risks that Volvo in

the future would have to dispose used products at a loss if the price

development of these products is worse than what was expected

when the contracts were entered. Provisions for residual value risks

are made on a continuing basis based upon estimations of the used

products’ future net realizable values. The estimations of future net

realizable values are made with consideration of current prices,

expected future price development, expected inventory turnover

period and expected variable and fi xed selling expenses. If the resid-

ual value risks are pertaining to products that are reported as tangible

assets in Volvo’s balance sheet, these risks are refl ected by deprecia-

tion or write-down of the carrying value of these assets. If the residual

value risks are pertaining to products, which are not reported as

assets in Volvo’s balance sheet, these risks are refl ected under the

line item short-term provisions.

Warranty expenses

Estimated costs for product warranties are charged to operating

expenses when the products are sold. Estimated costs include both

expected contractual warranty obligations as well as expected good-

will warranty obligations. Estimated costs are determined based upon

historical statistics with consideration of known changes in product

quality, repair costs or similar. Costs for campaigns in connection with

specifi c quality problems are charged to operating expenses when the

campaign is decided and announced.

Restructuring costs

Restructuring costs are reported as a separate line item in the income

statement if they relate to a considerable change of the Group struc-

ture. Other restructuring costs are included in Other operating income

and expenses. A provision for decided restructuring measures is

reported when a detailed plan for the implementation of the measures

is complete and when this plan is communicated to those who are

affected.

Deferred taxes, allocations and untaxed reserves

Tax legislation in Sweden and other countries sometimes contains

rules other than those identifi ed with generally accepted accounting

principles, and which pertain to the timing of taxation and measure-

ment of certain commercial transactions. Deferred taxes are provided

for on differences that arise between the taxable value and reported

value of assets and liabilities (temporary differences) as well as on

tax-loss carryforwards. However, with regard to the valuation of

deferred tax assets, that is, the value of future tax reductions, these

items are recognized provided that it is probable that the amounts can

be utilized against future taxable income.

Deferred taxes on temporary differences on participations in sub-

sidiaries and associated companies are only reported when it is prob-

able that the difference will be recovered in the near future.

Tax laws in Sweden and certain other countries allow companies to

defer payment of taxes through allocations to untaxed reserves.

These items are treated as temporary differences in the consolidated

balance sheet, that is, a split is made between deferred tax liability

and equity capital. In the consolidated income statement an allocation

to, or withdrawal from, untaxed reserves is divided between deferred

taxes and net income for the year.

Cash-fl ow statement

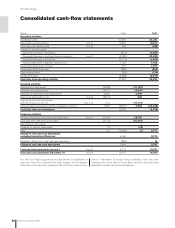

The cash-fl ow statement is prepared in accordance with IAS 7, Cash

Flow Statement, indirect method. The cash-fl ow statements of foreign

Group companies are translated at the average rate. Changes in

Group structure, acquisitions and divestments, are reported net,

excluding cash and cash equivalents, in the item Acquisition and

divestment of subsidiaries and other business units and are included

in Cash Flow from Investing Activities.

Cash and cash equivalents include cash, bank balances and parts

of Marketable Securities, with date of maturity within three months at the

time for investment. Marketable Securities comprise interest-bearing

securities, the majority of which with terms exceeding three years.

However, these securities have high liquidity and can easily be con-

verted to cash. In accordance with IAS 7, certain investment in mar-

ketable securities are excluded from the defi nition of cash and cash

equivalents in the cash-fl ow statement if the date of maturity of such

instruments is later than three months after the investment was

made.

Earnings per share

Earnings per share is calculated as the income for the period attrib-

uted to the shareholders of the parent company, divided with the aver-

age number of outstanding shares per reporting period. On April 26

2007, Volvo’s share split 6:1 with automatic redemption in which the

sixth share was redeemed by AB Volvo for SEK 25 per share took

effect, with the effect that the number of shares were fi vefold. To cal-

culate the diluted earnings per share, the average number of shares is

adjusted with the value of the share based incentive program and

employee stock option program recalculated to number of shares.

See Note 23 Shareholders’ equity.