Volvo 2007 Annual Report Download - page 130

Download and view the complete annual report

Please find page 130 of the 2007 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

The Volvo Group

126 Financial information 2007

Notes to consolidated fi nancial statements

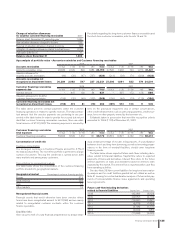

Note 37 Financial instruments

The fi nancial assets treated within the framework of IAS 39 are clas-

sifi ed either as fi nancial assets at fair value through profi t and loss, as

claims under a loan and receivables, as investments held to maturity

or as available-for-sale fi nancial assets.

Transaction expenses are included in the asset’s fair value except

in cases in which the change in value is recognized in the income

statement. The transaction costs arising in conjunction with assuming

fi nancial liabilities are amortized over the term of the loan as a fi nan-

cial cost. Embedded derivatives are detached from the related main

contract, if applicable. Contracts containing embedded derivatives are

valued at fair value in the income statement if the contracts inherent

risk and other characteristics indicate a close relation to the embed-

ded derivative. Classifi cations made of fi nancial instruments are evalu-

ated each quarter and, if necessary, the classifi cation is adjusted.

Purchases and sales of fi nancial assets and liabilities are recog-

nized on the transaction date. A fi nancial asset is derecognized (extin-

guished) in the balance sheet when all signifi cant risks and benefi ts

linked to the asset have been transferred to a third party.

The fair value of assets is determined based on the market prices

in such cases they exist. If market prices are unavailable, the fair value

is determined for each asset using various valuation techniques.

Financial assets at fair value through profi t and loss

A fi nancial asset recognized at fair value in the income statement is

categorized as follows: Either (1) it is recognized with the fi nancial

instruments or in accordance with (2) the so-called fair value option

on initial recognition has been designated as such. For the fi rst cat-

egory to apply, it is required that the asset is acquired with the main

purpose of being sold in the near future and that it is part of a port-

folio and there is a proven pattern of short-term capitalization of gains.

All of Volvo’s fi nancial assts that are recognized at fair value in the

income statement are in category 1.

Derivatives, included embedded derivatives detached from the host

contract, are classifi ed as held-for-trading if the are part of an evi-

dently effective hedge accounting or are a fi nancial guarantee. Gains

and losses on these assets are recognized in the income statement.

A fi nancial contract containing one or more embedded derivatives

is classifi ed in its entirety as a fi nancial asset whose value change is

recognized in the income statement if not the embedded derivative

does not affect future cash fl ow attributable to the fi nancial asset or

separation of the embedded instrument is required.

Short-term investments are valued at fair value and the changes in

this value are recognized in the income statement. Short-term invest-

ments that mainly consist of interest-bearing fi nancial instruments are

reported in Note 21.

Volvo classifi es fi nancial derivatives as fi nancial assets whose value

changes are reported in the income statements if they evidently are

not used in hedge accounting. All derivatives are reported in this note

below.

Financial assets held to maturity

Held-to-maturity investments are assets with fi xed payments and

term and that Volvo intends and is able to hold to maturity. After initial

valuation, these assets are valued at accrued acquisition value in

accordance with the effective interest method, with adjustment for

any impairment. Gains and losses are recognized in the income state-

ment when assets are divested or impaired as well as in pace with the

accrued interested being reported. At year end 2007 Volvo did not

have any fi nancial instruments classifi ed in this category.

Loan receivables and other receivables

Loans and receivables are non-derivative fi nancial assets with fi xed or

determinable payments, originated or acquired, that are not quoted in

an active market. After initial recognition, loans and receivables are

valued at accrued acquisition value in accordance with the effective

interest method. Gains and losses are recognized in the income state-

ment when the loans or receivables are divested or impaired as well

as in pace with the accrued interested being reported.

Accounts receivables are recognized initially at fair value, which

normally corresponds to the nominal value. In the event that the pay-

ment terms exceed one year, the receivable is recognized at the dis-

counted present value. Provisions for doubtful receivables are made

continuously after assessment of whether the customer’s payment

capacity has changed.

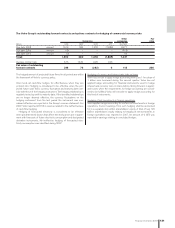

Volvo reports different loans and receivables. Note 16, Long-term

receivables in customer fi nancing operations presents mainly receiva-

bles related to installment purchases and fi nance leasing. Note 17,

Other long-term receivable, presents, among other items, Other loans

to external parties. Note 19, Current receivables in customer fi nan-

cing operations, presents installment purchases, fi nance leasing and

dealer fi nancing and Note 20, Other current receivables, is mainly

accounts receivable.

Available-for-sale assets

This category includes assets available for sales or those that have

not been classifi ed in any of the other three categories. These assets

are initially measured at fair value. Fair value changes are recognized

directly in shareholders’ equity. The cumulative gain or loss that was

recognized in equity is recognized in profi t or loss when an available-

for-sale fi nancial asset is sold. Unrealized value declines are recog-

nized in equity, if the decline is not considered temporary. If the value

decline is signifi cant and has lasted for a longer period, the value

impairment is recognized in the income statement. If the event caus-

ing the impairment no longer exists, impairment can be reversed in the

income statement if it does not involve an equity instrument.

Earned or paid interest attributable to these assets is recognized in

the income statement as part of net fi nancial items in accordance with

the effective interest method. Dividends received attributable to these

assts are recognized in the income statement as Earnings from other

shares and participations.

Volvo reports shares and participations in listed companies at mar-

ket value on the balance-sheet date, with the exception of investments

classed as associated companies and joint ventures. Companies

listed on fi nancial marketplaces are reported at market value on the

balance-sheet date. Holdings in unlisted companies for which a mar-

ket value is unavailable, are recognized at acquisition value. Volvo

classifi es these types of investments as assets available for sale. Note

15 Shares and participations lists Volvo’s holdings of shares and par-

ticipations in listed companies.

Impairments

Financial assets at fair value through profi t and loss

Impairments do not need to be reported for this category of assets

since they are continuously revalued at their fair value in the income

statement.