Volvo 2007 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2007 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

Trucks

– the strong market in

Europe and Asia continued

The world market for heavy trucks in 2007 was somewhat lower

compared with 2006, due to the downturn in the North American

market. Demand was strong in most markets throughout the rest

of the world.

The Volvo Group’s four truck brands have broadened

and strengthened their product ranges in recent

years and entered 2008 with the strongest line-ups

thus far.

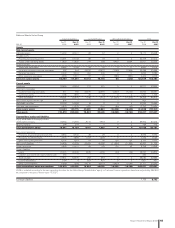

Net sales as percentage of

Volvo Group’s sales Operating margin1,2,3, %Net sales1,3, SEK bn Operating income1,2,3, SEK bn

0706050403

187.9171.3155.4136.9117.0

0706050403

15.214.811.79.04.0

66%

0706050403

8.18.77.56.63.4

1 Years 2004–2007 are reported in accordance with IFRS and 2003 in accordance with prevailing Swedish GAAP. See Note 1 and 3.

2 Excluding adjustment of goodwill in 2006.

3 Years 2006–2007 are reported according to a new reporting structure. See Note 7.

Total market

Europe’s strong economy moved at high

speed, with growth fi gures being revised

upwards, during 2007. High consumption and

construction rates generated strong demand

for various types of truck transports, which in

turn positively impacted sales of heavy

trucks.

Demand for heavy trucks rose in practically

all European markets. The industry as a whole

has been limited by insuffi cient manufactur-

ing capacity. Very strong demand was reported

in Eastern Europe as well as in Russia and the

Ukraine.

During 2007, the total market for heavy

trucks in Europe (EU-countries plus Norway

and Switzerland) amounted to approximately

329,000 vehicles, an increase of 9%. Within

Western Europe, the increase was 2%, while

there was a 57% increase in the new EU

countries.

The total European market is currently limit-

ed by the production capacity of the industry,

where order backlogs are substantial and deliv-

ery times are long. The strained production in

Europe affects the supply of trucks also on

markets in Asia, the Middle East and South

America. Order backlogs for 2008 indicate a

continued growth in the European heavy truck

market by some 5–10% compared with 2007.

In the medium-heavy segment, 10 to 15.9 tons,

the market in Western Europe remained

unchanged compared with 2006.

During 2007, the total market for heavy

trucks (Class 8) in North America declined by

40% to 208,000 trucks, compared with

349,000 trucks in 2006. The decrease is a

consequence of large pre-buy volumes during

2006 and the softer US economy. Forecast-

ing the market is diffi cult, but current expect-

ations are a demand for trucks in 2008 on the

same level as in 2007.

In Brazil, the overall market increased by

45% to 58,000 heavy trucks. Among the

larger Asian markets, China posted a 58%

increase to a new record level of 490,000

trucks over 14 tons (310,000). The market for

heavy trucks in India continued on a high level

of 193,000 vehicles during 2007 (197,000).

In Japan, the overall market for heavy trucks

fell 13% to 43,000 trucks (49,000).

Market shares

In 2007, Volvo Trucks’ market share for heavy

trucks in Europe 29 increased to 14.6% (14.3).

Renault Trucks’ market share in Europe

decreased to 9.7% for heavy trucks (10.6). In

the medium-duty truck segment, Renault Trucks’

market share was 12.5% (14.3) and Volvo

Trucks’ market share was 5.7% (3.7).

In Eastern Europe, Volvo’s market share

increased to 18.2% (17.5) and Renault’s share

was 7.9% (10.2).

During 2007, Volvo Trucks’ and Mack Trucks’

market shares in North America declined to

9.3% (10.2) and 7.3% (9.2) respectively.

In Japan, Nissan Diesel’s market share

amounted to 21.6% (20.7).

In the Brazilian market, Volvo’s share

declined by 1.7% to 13.6%.

52 Business areas 2007