Volvo 2007 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2007 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

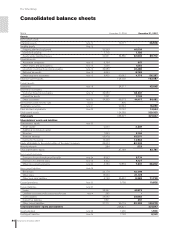

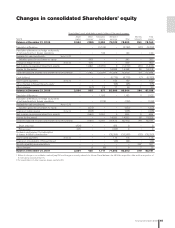

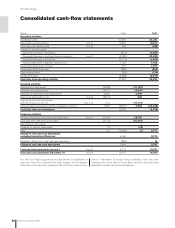

Financial information 2007 87

Notes to consolidated fi nancial statements

Note 1 Accounting principles

The consolidated fi nancial statements for AB Volvo and its subsidiar-

ies have been prepared in accordance with International Financial

Reporting Standards (IFRS) issued by the International Accounting

Standards Board (IASB), as adopted by the EU. The portions of IFRS

not adopted by the EU have no material effect on this report. This

annual report is prepared in accordance with IAS 1 Presentation of

Financial Statements and in accordance with the Swedish Companies

Act. In addition, RR30 Supplementary Rules for Groups, has been

applied, issued by the Swedish Financial Accounting Standards Council.

In the preparation of these fi nancial statements, the company man-

agement has made certain estimates and assumptions that affect the

value of assets and liabilities as well as contingent liabilities at the

balance sheet date. Reported amounts for income and expenses in

the reporting period are also affected. The actual future outcome of

certain transactions may differ from the estimated outcome when

these fi nancial statements were issued. Any such differences will

affect the fi nancial statements for future accounting periods. The key

sources of estimation uncertainty are set out in Note 2.

Changes of accounting principles

Effective in 2005 Volvo has applied International Financial Reporting

Standards (IFRS) in its fi nancial reporting. In accordance with the

IFRS transition rules in IFRS 1, Volvo applies retroactive application

from the IFRS transition date at January 1, 2004. The details of the

transition from Swedish GAAP to IFRS are set out in Note 3 in the

annual reports of 2005 and 2006. Refer to the 2004 Annual Report

for a description of the previous Swedish accounting principles applied

by Volvo.

New accounting principles in 2007

In accordance with considerations presented in the Annual Report,

Note 1, regarding new accounting principles for 2007, Volvo applies

the new standard IFRS 7, Financial instruments: Disclosures and clas-

sifi cation, as well as Amendments to IAS 1, Presentation of fi nancial

statements. IFRS 7 does not entail any change in the reporting and

valuation of fi nancial instruments. On the other hand, certain dis-

closure requirements have been expanded, compared with earlier

requirements under IAS 32, particularly as concerns the exposure and

management of risk relating to fi nancial instruments. The Amend-

ments to IAS 1 entail expanded additional disclosure regarding elem-

ents such as the defi nition of capital, capital structure and capital

management policies. In addition to IFRS 7 and the Amendment to

IAS 1, there are four IFRIC interpretations – IFRIC 7, Applying the

Restatement Approach under IAS 29 Financial Reporting in Hyperin-

fl ationary Economies; IFRIC 8, Scope of IFRS 2; IFRIC 9, Reassess-

ment of Embedded Derivatives; and IFRIC 10, Interim Financial

Reporting and Impairment. The application of IFRS 7, Amendment to

IAS 1 and IFRIC 7, 8, 9 and 10, has not had any impact on Volvo’s

fi nancial position or earnings.

New accounting principles 2008 and 2009

When preparing the consolidated accounts as of December 31, 2007,

a number of standards and interpretations have been published, but

have not yet become effective. The following is a preliminary assess-

ment of the effect the implementation of these standards and state-

ments could have on the Volvo Group’s fi nancial statements.

IFRS 8 Operating segments

The standard becomes effective on January 1, 2009 and applies for

the fi scal years beginning on that date. The standard addresses the

distribution of the company’s operations in different segments. In

accordance with the standard, the company shall adopt an approach

based on the internal reporting structure and determine the report-

able segments based on this structure. Volvo does not expect the

adoption of IFRS 8 to result in any change in the number of seg-

ments.

IFRIC 11 IFRS 2 Group and Treasury Share Transactions

The interpretation becomes effective on March 1, 2007 and applies to

fi scal years beginning after that date. The interpretation clarifi es treat-

ment regarding classifi cation of share-based payments in which the

company repurchases shares to settle its undertaking and reporting

of options programs in subsidiaries that apply IFRS. The Group will

apply IFRIC 11 as of January 1, 2008, but this is not expected to have

any impact on the Group’s fi nancial statements.

IFRIC 12 Service Concession Arrangements*

The interpretation becomes effective on January 1, 2008 and applies

to fi scal years beginning after that date. IFRIC 12 addresses arrange-

ments in which a private company shall establish an infrastructure to

provide public service for a specifi ed period. The company is paid for

this service during the term of the contract. The Group will apply IFRIC

12 as of January 1, 2008, but this is not expected to have any impact

on the Group’s fi nancial statements.

IFRIC 14 IAS 19 The limit on a defi ned benefi t asset, minimum

funding requirements and their interaction.*

The interpretation becomes effective on January 1, 2008 and applies

to fi scal years beginning after that date. The interpretation discusses

funding of defi ned benefi t pension plans and minimum funding

requirements in connection to IAS 19 and the limit on the measure-

ment for a defi ned benefi t asset. The Group will apply IFRIC 14 as of

January 1, 2008, but this is not expected to have a signifi cant impact

on the Group’s fi nancial statements.

IAS 23 amendment Borrowing costs*

The interpretation becomes effective on January 1, 2008 and applies

to fi scal years beginning after that date. The amendment states that

borrowing costs that are directly attributable to the acquisition, con-

struction or production of a qualifying asset form part of the cost of

that asset. The Group will apply the amendment as of January 1,

2009. According to the current accounting principle applied by Volvo,

borrowing costs are expensed. The amendment will result in a change

of accounting principle for the Volvo group, but is not expected to have

a signifi cant impact on the Group’s fi nancial statements.

IAS 1 amendment Presentation of fi nancial statements*

The amendment becomes effective on January 1, 2009 and applies

to fi scal years beginning after that date. The amendment concerns the

form for presentation of fi nancial position, comprehensive income and

cash fl ow. The Group will apply the amendment as of January 1, 2009,

which will not have a signifi cant impact on the Group’s fi nancial state-

ments, but only to a limited extent affect the form of presentation for

the group fi nancial statements.

Amounts in SEK M unless otherwise specifi ed. The amounts within parentheses refer to the preceding year, 2006.

* These standards/interpretations have not been adopted by the EU at this time. Accordingly, stated dates for adoption may change as a consequence of

decisions within the EU endorsement process.