Volvo 2007 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2007 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

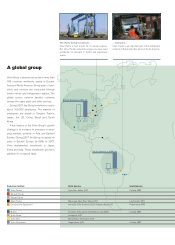

CEO comment

The Volvo Group had an intense 2007. During the year we carried out several

major acquisitions, established a strong presence in Asia, advanced our positions

in important product segments and launched many new products. We also

managed widely shifting demand trends in our main markets – with continued

growth in Europe, Asia and South America and a sharp decline in North America.

Strong growth

Following the acquisitions of Nissan Diesel,

Lingong and Ingersoll Rand’s road develop-

ment division, we now have a signifi cant

industrial structure in Asia, with a presence in

Japan, China and, when the expected coop-

eration with Eicher is in operation, also in

India. These are rapidly growing markets and

we want to be part of that growth. Our oper-

ations are now anchored on a strong global

base, in which growth in Eastern Europe and

Asia currently offsets the weak development

in North America. During the year, more than

40% of sales were from markets outside our

traditional home markets in Western Europe

and North America.

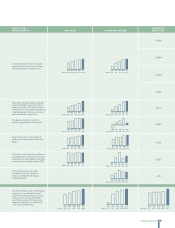

The Group’s sales rose 10% to slightly more

than SEK 285 billion, while operating income

was up 9% to more than SEK 22 billion. The

operating margin of 7.8% was at the 2006

level. The margin was negatively affected by

the weak development in North America and

substantial integration costs, which initially

result in lower profi tability in acquired com-

panies. Our Industrial operations continue to

generate a strong cash fl ow, SEK 15.2 billion

during 2007, which creates opportunities to

both provide our shareholders with a good yield

and for the Group to invest for the future.

Strong Europe and weak North America

The shifting market conditions are most appar-

ent in our truck operations. We have good sta-

bility and high profi tability in Europe, where we

increased deliveries despite already strained

production. We are now investing to expand

capacity and improve productivity. In Kaluga,

south of Moscow, we are constructing a new

assembly plant for both Volvo Trucks and

Renault Trucks, which also signed a coopera-

tion agreement with Turkish Karsan covering

production of Renault trucks to the growing

markets in Turkey and neighboring countries.

Combined with previously decided invest-

ments in engine manufacturing among other

areas, this means that the capacity of the truck

operations is being increased to capitalize on

the growth possibilities that exist in many mar-

kets around the world.

Following the acquisition of Nissan Diesel,

Asia is our second largest truck market.

Nissan Diesel has a strong market position in

many countries in the region, with a distinct

leadership in the environmental area. There

are many important growth markets in Asia

– China is already the world’s largest truck

market. The potential is also great in India and

in December we signed a letter of intent with

Indian Eicher Motors Limited covering coop-

eration within trucks and buses.

In North America, we introduced a new gen-

eration of engines that comply with the world’s

most stringent emission legislation, which

marked the fi nal step in the transition to one

global engine platform for our truck operations.

At the same time we carried out signifi cant

changeovers in the industrial system. Com-

bined with the weak demand, these measures

adversely affected profi tability. We had

expected that the market would improve dur-

ing the year, but the weak development of the

US economy thwarted a recovery.

We estimate that the truck market in Europe

will grow by 5–10% compared with 2007, with

the industry’s delivery capacity as the limiting

factor. The North American truck market is dif-

fi cult to assess, but we estimate that it will

achieve about the same level as in 2007, when it

amounted to slightly more than 205,000 trucks.

Further on, I am optimistic that the market will

return to its long-term trend curve, with a total

market of about 250,000 trucks per year.

Important acquisitions for

Construction Equipment

Construction Equipment’s net sales rose 27%

– a growth that was both organic and driven by

acquisitions. The business area made major

advances in Asia following the acquisition of

Lingong and Ingersoll Rand’s road development

division, while at the same time product renewal

was substantial. In most areas of the world, the

demand for construction equipment was strong

and Volvo’s CE’s manufacturing was heavily

strained after having hit capacity limits. This

led to increased production costs which in

combination with integration costs and unfa-

vourable currencies decreased profi tability.

Buses had a struggling year and strong

measures are required for profi tability to reach

satisfactory levels. During the year, Buses

introduced the new Euro 4 engines based on

the new engine platforms and they are far

ahead in the environment area, including

hybrid buses in the commercial phase. Buses

is now being integrated closer to the truck

companies and their purchasing organization,

with a focus on joint solutions, reduced costs

and increased profi tability.

Penta captures market shares

Volvo Penta’s marine engines continue to cap-

ture market shares, due particularly to the

revolutionary IPS propulsion system, which

8 A global group 2007