Volvo 2007 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2007 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

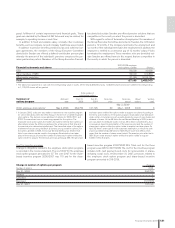

Financial information 2007 125

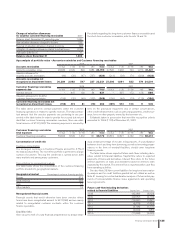

Age analysis of portfolio value – Accounts receivables and Customer fi nancing receivables

2006 2007

Accounts receivables not due 1–30 31–90 >90 Total not due 1–30 31–90 >90 Total

Accounts receivables gross 20,383 2,129 594 1,084 24,190 27,520 1,930 704 1,273 31,427

Valuation allowance for

doubtful accounts receivables (99) (36) (47) (757) (939) (214) (39) (71) (599) (923)

Accounts receivables not

recognized as impairment losses 20,284 2,093 547 327 23,251 27,306 1,891 633 674 30,504

Customer fi nancing receivables 2006 2007

payments due not due 1–30 31–90 >90 Total not due 1–30 31–90 >90 Total

Overdue amount – 447 130 54 631 – 597 173 126 896

Valuation allowance for doubtful

customer fi nancing receivables (155) (32) (49) (132) (368) (159) (46) (70) (115) (390)

Customer fi nancing receivables not

recognized as impairment losses (155) 415 81 (78) 263 (159) 551 103 11 506

Customer fi nancing receivables 2006 2007

total exposure not due 1–30 31–90 >90 Total not due 1–30 31–90 >90 Total

Customer fi nancing receivables 55,303 8,726 1,412 731 66,172 66,812 10,527 2,162 709 80,210

Concentration of credit risk

Customer concentration

The ten largest customers in Customer Finance account for 4.7% of

the total asset portfolio. The rest of the portfolio is pertinent to a large

number of customer. This way the credit risk is spread across both

many markets and among many customers.

Concentration by geographical markets

The table below shows the concentration of the customer fi nancing

portfolio divided into geographical markets.

Geographical market Percentage of customer fi nancing portfolio

Europe 57.5

North America 29.9

Asia 5.6

Other markets 7.0

Renegotiated fi nancial assets

Financial assets that would otherwise have been overdue whose

terms have been renegotiated amount to 937 (996) and are mainly

related to renegotiated customer contracts within the customer

fi nance operations.

Liquidity risks

Volvo assures itself of sound fi nancial preparedness by always keep-

Change of valuation allowances

for doubtful customer fi nancing receivables 2007

Balance sheet, December 31, preceding year 1,430

New valuation allowance charged to income 235

Reversal of valuation allowance charged to income (92)

Utilization of valuation allowance related to actual losses (227)

Translation differences 17

Balance sheet, December 31 1,363

For details regarding the long-term customer fi nance receivables and

the short-term customer receivables, refer to note 16 and 19.

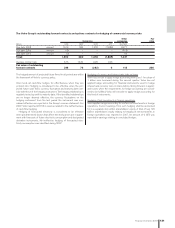

The table above presents overdue payments within the customer

fi nancing operations in relation to specifi c reserves. The total contrac-

tual amount that the overdue payments are pertaining to are pre-

sented in the table below. In order to provide for occured but not yet

identifi ed customer fi nancing receivables overdues, there are addi-

tional reserves of 973 (1,062). The remaining exposure is secured by

liens on the purchased equipment, and, in certain circumstances,

other credit enhancements such as personal guarantees, credit insur-

ance, liens on other property owned by the borrower etc.

Collaterals taken in possession that meet the recognition criteria

amounted to 129.9 (111.9) at December 31, 2007.

ing a certain percentage of its sales in liquid assets. A sound balance

between short- and long-term borrowing, as well as borrowing prepar-

edness in the form of overdraft facilities, should cover long-term

fi nancing needs.

The table below shows expected future cash-fl ows including deriv-

atives related to fi nancial liabilities. Capital fl ow refers to expected

payments of loans and derivatives. Interest fl ow refers to the future

interest payments on loans and derivatives based on interests rates

expected by the market. The interest fl ow is reported within cash fl ow

from operating activities.

See also Note 26 Non-current liabilities for long-term loans matur-

ity analysis and for credit facilities granted but not utilized as well as

Note 31 Leasing for contractual duration analysis of future rental pay-

ments of noncancellable fi nance lease agreements and operating

lease agreements.

Future cash-fl ow including derivatives

related to fi nancial liabilities Capital fl ow Interest fl ow

2008 (42,380) (3,928)

2009 (22,557) (2,716)

2010 (12,661) (1,891)

2011 (5,678) (1,426)

2012 (3,196) (1,171)

2013 (2,604) (986)

2014– (17,693) (2,425)