Volvo 2007 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2007 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

The Volvo Group

114 Financial information 2007

Notes to consolidated fi nancial statements

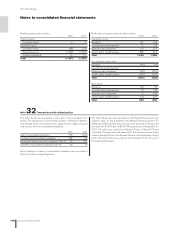

Volvo’s pension foundation in Sweden was formed in 1996 to secure

obligations relating to retirement pensions for salaried employees in

Sweden in accordance with the ITP plan (a Swedish individual pension

plan). Plan assets amounting to 2,456 was contributed to the founda-

tion at its formation, corresponding to the value of the pension obliga-

tions at that time. Since its formation, net contributions of 1,472,

whereof 52 during 2007, have been made to the foundation. The plan

assets in Volvo’s Swedish pension foundation are invested in Swedish

and foreign stocks and mutual funds, and in interest-bearing secur-

ities, in accordance with a distribution that is determined by the foun-

dation’s Board of Directors. At December 31, 2007, the fair value of

the foundation’s plan assets amounted to 6,648 (6,394), of which

43% (45) was invested in shares or mutual funds. At the same date,

retirement pension obligations attributable to the ITP plan amounted

to 7,847 (6,560). In the valuation of Volvo’s pension liability for the

Swedish companies, the life-expectancy assumptions was changed

during 2007. Men are now assumed to live about two years longer

than previously. The increase for women is about one year. The

changed life-expectancy assumptions increased the pension obliga-

tion by about 14%. However, this increase has not affected the carry-

ing amount of the Volvo Group’s liabilities immediately since Volvo

applies the corridor approach to actuarial gains and losses. Swedish

companies can secure new pension obligations through balance

sheet provisions or pension fund contributions. Furthermore, a credit

insurance must be taken out for the value of the obligations. In add-

ition to benefi ts relating to retirement pensions, the ITP plan also

includes, for example, a collective family pension, which Volvo fi nances

through insurance with the Alecta insurance company. According to

an interpretation from the Swedish Financial Accounting Standards

Council’s interpretations committee, this is a multi-employer defi ned

benefi t plan. For fi scal year 2007, Volvo did not have access to infor-

mation from Alecta that would have enabled this plan to be reported

as a defi ned benefi t plan. Accordingly, the plan has been reported as

a defi ned contribution plan. Alecta’s funding ratio is 152,0% (143.1%).

Alecta’s current funding ratio exceeds the target of 140%. Accord-

ingly, Alecta’s Board of Directors has decided to reduce premiums for

defi ned benefi t plans and family pensions by 40% during 2008.

Volvo’s subsidiaries in the United States mainly secure their pen-

sion obligations through transfer of funds to pension plans. At the end

of 2007, the total value of pension obligations secured by pension

plans of this type amounted to 10,928 (11,830). At the same point in

time, the total value of the plan assets in these plans amounted to

12,195 (12,226), of which 58% (60) was invested in shares or mutual

funds. The regulations for securing pension obligations stipulate cer-

tain minimum levels concerning the ratio between the value of the

plan assets and the value of the obligations. During 2007, Volvo con-

tributed 0 (2,858) to the pension plans.

During 2007 Volvo has made extra contributions to the pension-

plans in Great Britain in the amount of 135 (646).

In 2008, Volvo estimate to transfer an amount of not more than

SEK 1 billion to pension plans.

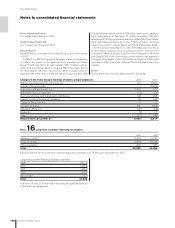

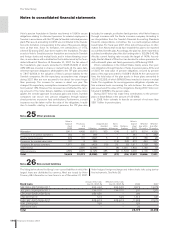

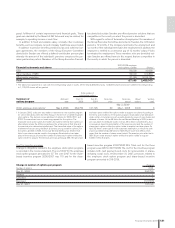

Note 25 Other provisions

Note 26 Non-current liabilities

Value in Value in

balance Provisions Acquired and Trans- blance Whereof Whereof

sheet and divested lation Reclassi- sheet due within due after

2006 reversal Utilization companies differences fi cations 2007 12 months 12 months

Warranties 8,411 4,495 (3,811) 300 (24) 2 9,373 5,014 4,359

Provisions in insurance operations 362 91 (66) – – – 387 5 382

Restructuring measures 429 101 (322) 5 4 (3) 214 186 28

Provisions for residual value risks 781 8 (56) – (13) (50) 670 433 237

Provisions for service contracts 1,677 626 (400) (13) 23 (2) 1,911 1,128 783

Dealer bonus – 2,681 (2,438) – (8) 1,567 1,802 1,784 18

Other provisions 4,889 2,070 (2,195) 385 (9) (1,540) 3,600 2,106 1,494

Total 16,549 10,072 (9,288) 677 (27) (26) 17,957 10,656 7,301

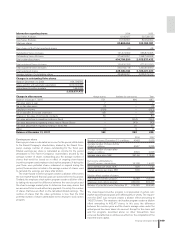

The listing below shows the Group’s non-current liabilities in which the

largest loans are distributed by currency. Most are issued by Volvo

Treasury AB. Information on loan terms is as of December 31, 2007.

Volvo hedges foreign-exchange and interest-rate risks using deriva-

tive instruments. See Note 36.

Actual interest rate, Effective interest rate,

Bond loans Dec 31, 2007, % Dec 31, 2007, % 2006 2007

SEK 2004–2007/2009–2017 4.00–4.94 4.00–5.02 8,973 13,378

JPY 2001–2006/2009–2011 1.39–2.70 1.39–2.70 231 1,203

CZK 2003–2005/2009–2010 2.69–4.50 – 389 –

USD 2007/2010 5.13 5.22 1,614 647

EUR 1997–2007/2009–2017 4.06–6.13 4.06–6.13 11,623 27,070

NOK 2006/2009 3.59 – 329 –

Other bond loans – – 20 –

Total 23,179 42,298