Volvo 2007 Annual Report Download - page 127

Download and view the complete annual report

Please find page 127 of the 2007 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

Financial information 2007 123

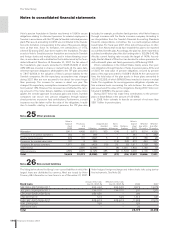

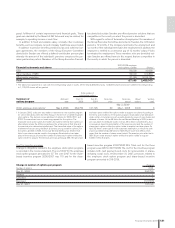

Note 35 Fees to the auditors

Note 36 Goals and policies in fi nancial risk management

Audit fees 2006 2007

Audit fees to PricewaterhouseCoopers 130 109

Audit fees to other audit fi rms 1 3

Total 131 112

Other fees to PricewaterhouseCoopers

Fees for audit related services 20 97

Fees for tax services 14 12

Total 34 109

Fees and other remuneration to

external auditors total 165 221

Auditing assignments involve examination of the annual report and

fi nancial accounting and the administration by the Board and the

President, other tasks related to the duties of a company auditor and

consultation or other services that may result from observations noted

during such examination or implementation of such other tasks. All

other tasks are defi ned as other assignments.

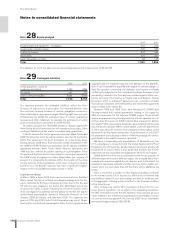

Apart from derivatives, Volvo’s fi nancial instruments consist of bank

loans, fi nancial leasing contracts, accounts payable, accounts receiv-

able, shares and participations, as well as cash and short-term invest-

ments.

The primary risks deriving from the handling of fi nancial instru-

ments are interest-rate risk, currency risk, liquidity risk and credit risk.

All of these risks are handled in accordance with an established fi nan-

cial policy.

Interest-rate risk

Interest-rate risk refers to the risk that changed interest-rate levels will

affect consolidated earnings and cash fl ow (cash-fl ow risks) or the fair

value of fi nancial assets and liabilities (price risks). Matching the inter-

est-fi xing terms of fi nancial assets and liabilities reduces the expos-

ure. Interest-rate swaps are used to change/infl uence the interest-

fi xing term for the Group’s fi nancial assets and liabilities. Currency

interest-rate swaps permit borrowing in foreign currencies from differ-

ent markets without introducing currency risk. Volvo also has stand-

ardized interest-rate forward contracts (futures) and FRAs (forward-

rate agreements). Most of these contracts are used to hedge

interest-rate levels for short-term borrowing or investment.

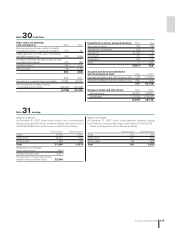

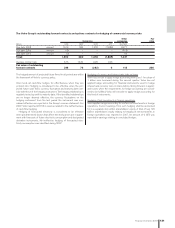

Cash-fl ow risks

The effect of changed interest-rate levels on future currency and

interest-rate fl ows refers mainly to the Group’s customer fi nancing

operations and net fi nancial items. Within the customer fi nance oper-

ations the degree of matching interest-rate fi xing on borrowing and

lending is measured. The calculation of the matching degree excludes

equity, which in the customer fi nance operations amount to between

8 and 10%. According to the Group’s policy, the degree of matching

for interest-rate fi xing on borrowing and lending in the customer-fi -

nancing operations must exceed 80%. At year-end 2007, the degree

of such matching was 100% (100). A part of the short-term fi nancing

of the customer fi nancing operations is however pertaining to internal

loans from the industrial operations, why the matching ratio in the

Volvo group was slightly lower. At year-end 2007, in addition to the

assets in its customer-fi nancing operations, Volvo’s interest-bearing

assets consisted primarily of liquid assets invested in short-term inter-

est-bearing securities. The objective is to achieve an interest-fi xing

term of six months for the liquid assets in Volvo’s industrial operations

through the use of derivatives. On December 31, 2007, after taking

derivatives into account, the average interest on these assets was

4.4% (3.5). Apart from loans raised to fi nance the credit portfolio of

the customer-fi nancing operations, at this same point in time, Volvo’s

fi nancial liabilities consisted primarily of provisions for pensions and

similar commitments. After taking derivatives into account, outstand-

ing loans had interest terms corresponding to an interest-rate fi xing

term of six months and the average interest at year-end amounted to

4,5% (6.3).

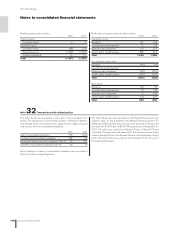

Price risks

Exposure to price risks as result of changed interest-rate levels refers

to fi nancial assets and liabilities with a lower interest-rate fi xing term

(fi xed interest). A comparison of the reported values and the fair val-

ues of all of Volvo’s fi nancial assets and liabilities, as well as its deriva-

tives, is given in Note 37, Financial instruments. After the transition to

IFRS in 2005, the market values agree with the book values.

Assuming that the market interest rates for all currencies suddenly

rose by one percentage point (100 interest-rate points) over the inter-

est-rate level on December 31, 2007, over a 12-month period, all other

variables remaining unchanged, Volvo’s net interest income would be

favorably impacted by 108 (236). Assuming that the market interest

rates for all currencies fell in a similar manner by one percentage point

(100 interest-rate points), Volvo’s net interest income would be

adversely impacted by a corresponding amount.

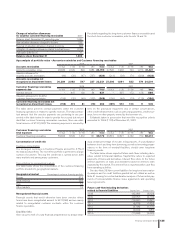

The following table shows the effect on earnings in Volvo’s key cur-

rencies that would result is the interest-rate level were to change by

1 percentage point.

SEK M Effect on earnings

SEK 225

USD 10

EUR (116)

CAD (10)

JPY (121)

KRW 7

The above sensitivity analysis is based on assumptions that rarely

occur in reality. It is not unreasonable that market interest rates

change with 100 interest-rate points over a 12-month period. How-

ever, in reality, market interest rates usually do not rise or fall at one

point in time. Moreover, the sensitivity analysis also assumes a parallel

shift in the yield curve and an identical effect of changed market inter-

est rates on the interest-rates of both assets and liabilities. Conse-

quently, the effect of actual interest-rate changes may deviate from

the above analysis. Volvo uses derivatives to hedge currency and interest

rate risks.