The Hartford 2008 Annual Report Download - page 321

Download and view the complete annual report

Please find page 321 of the 2008 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

311 -

312

312 -

313

313 -

314

314 -

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

-

565

-

566

-

567

-

568

-

569

-

570

-

571

-

572

-

573

-

574

-

575

-

576

-

577

-

578

-

579

-

580

-

581

-

582

-

583

-

584

-

585

-

586

-

587

-

588

-

589

-

590

-

591

-

592

-

593

-

594

-

595

-

596

-

597

-

598

-

599

-

600

-

601

-

602

-

603

-

604

-

605

-

606

-

607

-

608

-

609

-

610

-

611

-

612

-

613

-

614

-

615

-

616

-

617

-

618

-

619

-

620

-

621

-

622

-

623

-

624

-

625

-

626

-

627

-

628

-

629

-

630

-

631

-

632

-

633

-

634

-

635

-

636

-

637

-

638

-

639

-

640

-

641

-

642

-

643

-

644

-

645

-

646

-

647

-

648

-

649

-

650

-

651

-

652

-

653

-

654

-

655

-

656

-

657

-

658

-

659

-

660

-

661

-

662

-

663

-

664

-

665

-

666

-

667

-

668

-

669

-

670

-

671

-

672

-

673

-

674

-

675

-

676

-

677

-

678

-

679

-

680

-

681

-

682

-

683

-

684

-

685

-

686

-

687

-

688

-

689

-

690

-

691

-

692

-

693

-

694

-

695

-

696

-

697

-

698

-

699

-

700

-

701

-

702

-

703

-

704

-

705

-

706

-

707

-

708

-

709

-

710

-

711

-

712

-

713

-

714

-

715

-

716

-

717

-

718

-

719

-

720

-

721

-

722

-

723

-

724

-

725

-

726

-

727

-

728

-

729

-

730

-

731

-

732

-

733

-

734

-

735

-

736

-

737

-

738

-

739

-

740

-

741

-

742

-

743

-

744

-

745

-

746

-

747

-

748

-

749

-

750

-

751

-

752

-

753

-

754

-

755

-

756

-

757

-

758

-

759

-

760

-

761

-

762

-

763

-

764

-

765

-

766

-

767

-

768

-

769

-

770

-

771

-

772

-

773

-

774

-

775

-

776

-

777

-

778

-

779

-

780

-

781

-

782

-

783

-

784

-

785

-

786

-

787

-

788

-

789

-

790

-

791

-

792

-

793

-

794

-

795

-

796

-

797

-

798

-

799

-

800

-

801

-

802

-

803

-

804

-

805

-

806

-

807

-

808

-

809

-

810

-

811

-

812

-

813

-

814

-

815

|

|

Table of Contents

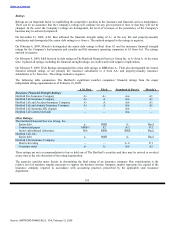

The table below sets forth statutory surplus for the Company’s insurance companies. The statutory surplus amounts as of

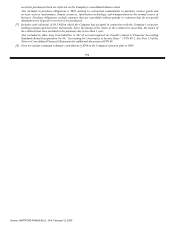

December 31, 2007 in the table below are based on actual statutory filings with the applicable regulatory authorities. The

statutory surplus amounts as of December 31, 2008 are estimates, as the respective 2008 statutory filings have not yet been

made.

2008 2007

Life Operations $ 6,047 $ 5,786

Japan Life Operations 1,718 1,620

Property & Casualty Operations 6,012 8,509

Total $ 13,777 $ 15,915

The Company has received approval from the Connecticut Insurance Department regarding the use of two permitted

practices in the statutory financial statements of its Connecticut-domiciled life insurance subsidiaries as of December 31,

2008. The first permitted practice relates to the statutory accounting for deferred income taxes. Specifically, this permitted

practice modifies the accounting for deferred income taxes prescribed by the NAIC by increasing the realization period for

deferred tax assets from one year to three years and increasing the asset recognition limit from 10% to 15% of adjusted

statutory capital and surplus. The benefits of this permitted practice may not be considered by the Company when

determining surplus available for dividends. The second permitted practice relates to the statutory reserving requirements for

variable annuities with guaranteed living benefit riders. Actuarial guidelines prescribed by the NAIC require a stand-alone

asset adequacy analysis reflecting only benefits, expenses and charges that are associated with the riders for variable

annuities with guaranteed living benefits. The permitted practice allows for all benefits, expenses and charges associated

with the variable annuity contract to be reflected in the stand-alone asset adequacy test. These permitted practices resulted in

an increase to Life operations estimated statutory surplus of $987 as of December 31, 2008. The effects of these permitted

practices are included in the 2008 Life operations surplus amount in the table above.

Statutory Capital

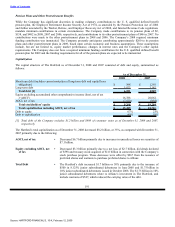

The Company’s stockholders’ equity, as prepared using U.S. GAAP was $9.3 billion as of December 31, 2008. The

Company’s estimated aggregate statutory capital and surplus, as prepared in accordance with the National Association of

Insurance Commissioners’ Accounting Practices and Procedures Manual (“US STAT”) was $13.8 billion as of

December 31, 2008. Significant differences between U.S. GAAP stockholders’ equity and aggregate statutory capital and

surplus prepared in accordance with US STAT include the following:

• Costs incurred by the Company to acquire insurance policies are deferred under U.S. GAAP while those costs are

expensed immediately under US STAT.

• Temporary differences between the book and tax basis of an asset or liability which are recorded as deferred tax assets

are evaluated for recoverability under U.S. GAAP while those amounts deferred are subject to limitations under US

STAT.

• Certain assumptions used in the determination of Life benefit reserves are prescribed under US Stat and are intended to

be conservative, while the assumptions used under U.S. GAAP are generally the Company’s best estimates. In addition,

the methodologies used for determining life reserve amounts are different between US Stat and U.S. GAAP. Annuity

reserving and cash-flow testing for death and living benefit reserves under US STAT are generally addressed by the

Commissioners’ Annuity Reserving Valuation Methodology and the related Actuarial Guidelines. Under these

Actuarial Guidelines, in general, future cash flows associated with the variable annuity business are included in these

methodologies with estimates of future fee revenues, claim payments, expenses, reinsurance impacts and hedging

impacts. At December 31, 2008, in determining the cash-flow impacts related to future hedging, assumptions were

made in the scenarios that generate reserve requirements, about the potential future decreases in the hedge benefits and

increases in hedge costs which resulted in increased reserve requirements. Reserves for death and living benefits under

U.S. GAAP are either considered embedded derivatives and recorded at fair value or they may be considered SOP 03-1

reserves.

• The difference between the amortized cost and fair value of fixed maturity and other investments, net of tax, is recorded

as an increase or decrease to the carrying value of the related asset and to equity under U.S. GAAP, while US STAT

only records certain securities at fair value, such as equity securities and certain lower rated bonds required by the

NAIC to be recorded at the lower of amortized cost or fair value. In the case of the Company’s market value adjusted

(MVA) fixed annuity products, invested assets are marked to fair value (including the impact of credit spreads) and

liabilities are marked to fair value (but generally actual credit spreads are not fully reflected) for statutory purposes

only.

• US STAT for life insurance companies establishes a formula reserve for realized and unrealized losses due to default

and equity risks associated with certain invested assets (the Asset Valuation Reserve), while U.S. GAAP does not.

Also, for those realized gains and losses caused by changes in interest rates, US STAT for life insurance companies

defers and amortizes the gains and losses, caused by changes in interest rates, into income over the original life to

Source: HARTFORD FINANCIAL S, 10-K, February 12, 2009