The Hartford 2008 Annual Report Download - page 204

Download and view the complete annual report

Please find page 204 of the 2008 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

-

565

-

566

-

567

-

568

-

569

-

570

-

571

-

572

-

573

-

574

-

575

-

576

-

577

-

578

-

579

-

580

-

581

-

582

-

583

-

584

-

585

-

586

-

587

-

588

-

589

-

590

-

591

-

592

-

593

-

594

-

595

-

596

-

597

-

598

-

599

-

600

-

601

-

602

-

603

-

604

-

605

-

606

-

607

-

608

-

609

-

610

-

611

-

612

-

613

-

614

-

615

-

616

-

617

-

618

-

619

-

620

-

621

-

622

-

623

-

624

-

625

-

626

-

627

-

628

-

629

-

630

-

631

-

632

-

633

-

634

-

635

-

636

-

637

-

638

-

639

-

640

-

641

-

642

-

643

-

644

-

645

-

646

-

647

-

648

-

649

-

650

-

651

-

652

-

653

-

654

-

655

-

656

-

657

-

658

-

659

-

660

-

661

-

662

-

663

-

664

-

665

-

666

-

667

-

668

-

669

-

670

-

671

-

672

-

673

-

674

-

675

-

676

-

677

-

678

-

679

-

680

-

681

-

682

-

683

-

684

-

685

-

686

-

687

-

688

-

689

-

690

-

691

-

692

-

693

-

694

-

695

-

696

-

697

-

698

-

699

-

700

-

701

-

702

-

703

-

704

-

705

-

706

-

707

-

708

-

709

-

710

-

711

-

712

-

713

-

714

-

715

-

716

-

717

-

718

-

719

-

720

-

721

-

722

-

723

-

724

-

725

-

726

-

727

-

728

-

729

-

730

-

731

-

732

-

733

-

734

-

735

-

736

-

737

-

738

-

739

-

740

-

741

-

742

-

743

-

744

-

745

-

746

-

747

-

748

-

749

-

750

-

751

-

752

-

753

-

754

-

755

-

756

-

757

-

758

-

759

-

760

-

761

-

762

-

763

-

764

-

765

-

766

-

767

-

768

-

769

-

770

-

771

-

772

-

773

-

774

-

775

-

776

-

777

-

778

-

779

-

780

-

781

-

782

-

783

-

784

-

785

-

786

-

787

-

788

-

789

-

790

-

791

-

792

-

793

-

794

-

795

-

796

-

797

-

798

-

799

-

800

-

801

-

802

-

803

-

804

-

805

-

806

-

807

-

808

-

809

-

810

-

811

-

812

-

813

-

814

-

815

|

|

Table of Contents

For hurricane Ike, the TWIA board indicated that the first $370 of TWIA losses from hurricane Ike would be covered by the

CRTF, but that the cost of TWIA losses and reinstatement premium above that amount would be funded by assessments. Of

the $430 in assessments, $230 is to fund the first $230 of TWIA losses in excess of the $370 available in the CRTF and $200

is to fund additional reinsurance premiums that TWIA must pay to reinstate a layer of coverage that reimburses TWIA for

up to $1.5 billion of TWIA losses in excess of $600 per occurrence. Thus, TWIA’s assessment notice for $430 is based on

an estimate that TWIA losses from hurricane Ike will total approximately $2.1 billion. If TWIA losses exceed $2.1 billion,

the entire amount in excess of $2.1 billion would be recovered from assessing member companies according to their market

share. In notifying member companies, TWIA’s board of directors stated that actual TWIA losses will likely be greater than

$2.1 billion and management has accrued a total of $27 in assessments for Ike based on an estimate that TWIA’s Ike losses

will be approximately $2.5 billion and that TWIA assessments to the industry will ultimately be approximately $830. Of the

$27 in assessments for Ike recorded in 2008, $7 has been recorded as incurred losses within current accident year

catastrophes and $20 has been recorded as insurance operating costs and expenses.

Through premium tax credits, member companies may recoup a portion of Ike-related assessments made to cover the first

$2.1 billion of TWIA losses and may recoup all of the Ike-related assessments made to fund losses in excess of that amount.

None of the assessments for hurricane Dolly may be recouped. Under generally accepted accounting principles, the

Company is required to accrue the assessments in the period the assessments become probable and estimable and the

obligating event has occurred. However, premium tax credits may not be recorded as an asset until the related premium is

earned and TWIA requires that premium tax credits be spread over a period of at least five years. The Company estimates

that of the $27 of accrued assessments for Ike, it will ultimately be able to recoup $20 through premium tax credits.

Florida Citizens Assessments

Citizens Property Insurance Corporation in Florida (“Citizens”) provides property insurance to Florida homeowners and

businesses that are unable to obtain insurance from other carriers, including for properties deemed to be “high risk”. Citizens

maintains a Personal Lines account, a Commercial Lines account and a High Risk account. If Citizens incurs a deficit in any

of these accounts, Citizens may impose a “regular assessment” on other insurance carriers in the state to fund the deficits,

subject to certain restrictions and subject to approval by the Florida Office of Insurance Regulation. Carriers are then

permitted to surcharge policyholders to recover the assessments over the next few years. Citizens may also opt to finance a

portion of the deficits through issuing bonds and may impose “emergency assessments” on other insurance carriers to fund

the bond repayments. Unlike with regular assessments, however, insurance carriers only serve as a collection agent for

emergency assessments and are not required to remit surcharges for emergency assessments to Citizens until they collect

surcharges from policyholders. Under generally accepted accounting principles, the Company is required to accrue for

regular assessments in the period the assessments become probable and estimable and the obligating event has occurred.

Surcharges to recover the amount of regular assessments may not be recorded as an asset until the related premium is

written. Emergency assessments that may be levied by Citizens are not recorded in the income statement.

In 2006, Citizens assessed the Company to fund deficits arising from hurricane losses in 2004 and 2005. In 2006, the

Company reduced its estimate of Citizens assessments by $41 from the amount that had been originally estimated in 2005.

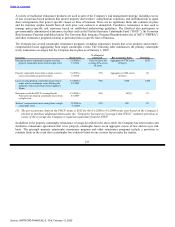

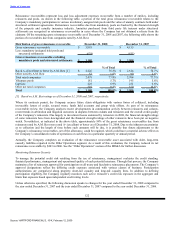

Reinsurance Recoverables

The following table shows the components of the gross and net reinsurance recoverable as of December 31, 2008 and 2007:

Reinsurance Recoverable December 31, 2008 December 31, 2007

Paid loss and loss adjustment expenses $ 326 $ 347

Unpaid loss and loss adjustment expenses 3,492 3,788

Gross reinsurance recoverable 3,818 4,135

Less: allowance for uncollectible reinsurance (379) (404)

Net reinsurance recoverable $ 3,439 $ 3,731

121

Source: HARTFORD FINANCIAL S, 10-K, February 12, 2009