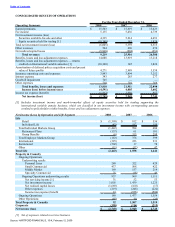

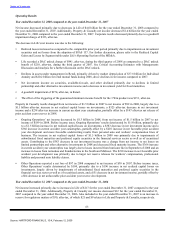

The Hartford 2008 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2008 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

-

565

-

566

-

567

-

568

-

569

-

570

-

571

-

572

-

573

-

574

-

575

-

576

-

577

-

578

-

579

-

580

-

581

-

582

-

583

-

584

-

585

-

586

-

587

-

588

-

589

-

590

-

591

-

592

-

593

-

594

-

595

-

596

-

597

-

598

-

599

-

600

-

601

-

602

-

603

-

604

-

605

-

606

-

607

-

608

-

609

-

610

-

611

-

612

-

613

-

614

-

615

-

616

-

617

-

618

-

619

-

620

-

621

-

622

-

623

-

624

-

625

-

626

-

627

-

628

-

629

-

630

-

631

-

632

-

633

-

634

-

635

-

636

-

637

-

638

-

639

-

640

-

641

-

642

-

643

-

644

-

645

-

646

-

647

-

648

-

649

-

650

-

651

-

652

-

653

-

654

-

655

-

656

-

657

-

658

-

659

-

660

-

661

-

662

-

663

-

664

-

665

-

666

-

667

-

668

-

669

-

670

-

671

-

672

-

673

-

674

-

675

-

676

-

677

-

678

-

679

-

680

-

681

-

682

-

683

-

684

-

685

-

686

-

687

-

688

-

689

-

690

-

691

-

692

-

693

-

694

-

695

-

696

-

697

-

698

-

699

-

700

-

701

-

702

-

703

-

704

-

705

-

706

-

707

-

708

-

709

-

710

-

711

-

712

-

713

-

714

-

715

-

716

-

717

-

718

-

719

-

720

-

721

-

722

-

723

-

724

-

725

-

726

-

727

-

728

-

729

-

730

-

731

-

732

-

733

-

734

-

735

-

736

-

737

-

738

-

739

-

740

-

741

-

742

-

743

-

744

-

745

-

746

-

747

-

748

-

749

-

750

-

751

-

752

-

753

-

754

-

755

-

756

-

757

-

758

-

759

-

760

-

761

-

762

-

763

-

764

-

765

-

766

-

767

-

768

-

769

-

770

-

771

-

772

-

773

-

774

-

775

-

776

-

777

-

778

-

779

-

780

-

781

-

782

-

783

-

784

-

785

-

786

-

787

-

788

-

789

-

790

-

791

-

792

-

793

-

794

-

795

-

796

-

797

-

798

-

799

-

800

-

801

-

802

-

803

-

804

-

805

-

806

-

807

-

808

-

809

-

810

-

811

-

812

-

813

-

814

-

815

|

|

Table of Contents

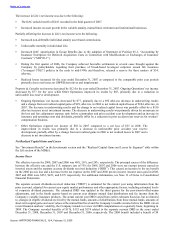

Pursuant to accounting principles related to the Company’s pension and other postretirement obligations to employees under

its various benefit plans, the Company is required to make a significant number of assumptions in order to calculate the

related liabilities and expenses each period. The two economic assumptions that have the most impact on pension and other

postretirement expense are the discount rate and the expected long-term rate of return on plan assets. In determining the

discount rate assumption, the Company utilizes a discounted cash flow analysis of the Company’s pension and other

postretirement obligations and currently available market and industry data. The yield curve utilized in the cash flow

analysis is comprised of bonds rated Aa or higher with maturities primarily between zero and thirty years. Based on all

available information, it was determined that 6.25% was the appropriate discount rate as of December 31, 2008 to calculate

the Company’s pension and other postretirement obligation. Accordingly, the 6.25% discount rate will also be used to

determine the Company’s 2009 pension and other postretirement expense. At December 31, 2007, the discount rate was also

6.25%.

As of December 31, 2008, a 25 basis point increase/decrease in the discount rate would decrease/increase the pension and

other postretirement obligations by $116 and $9, respectively. However, because the Company employs a duration overlay

program to adjust the duration of the fixed income component of the Plan assets to better match the duration of the

liabilities, the funded status of the pension benefits would only increase/decrease by $43.

The Company determines the expected long-term rate of return assumption based on an analysis of the Plan portfolio’s

historical compound rates of return since 1979 (the earliest date for which comparable portfolio data is available) and over

5 year and 10 year periods. The Company selected these periods, as well as shorter durations, to assess the portfolio’s

volatility, duration and total returns as they relate to pension obligation characteristics, which are influenced by the

Company’s workforce demographics. In addition, the Company also applies long-term market return assumptions utilized in

Life’s DAC analysis to an investment mix that generally anticipates 60% fixed income securities, 20% equity securities and

20% alternative assets to derive an expected long-term rate of return. Based upon these analyses, management maintained

the long-term rate of return assumption at 7.30% as of December 31, 2008. This assumption will be used to determine the

Company’s 2009 expense. The long-term rate of return assumption at December 31, 2007, that was used to determine the

Company’s 2008 expense, was also 7.30%.

Pension expense reflected in the Company’s net income was $122, $131 and $152 in 2008, 2007 and 2006, respectively. The

Company estimates its 2009 pension expense will be approximately $134, based on current assumptions. To illustrate the

impact of these assumptions on annual pension expense for 2009 and going forward, a 25 basis point decrease in the

discount rate will increase pension expense by approximately $12 and a 25 basis point change in the long-term asset return

assumption will increase/decrease pension expense by approximately $9.

In 2008, the deterioration of the global economy, together with the current credit crisis, caused significant volatility in

interest rates and equity prices, which caused actual asset returns of the Plan’s investment portfolios to be less than expected.

As provided for under SFAS No. 87, the Company uses a five-year averaging method to determine the market-related value

of Plan assets, which is used to determine the expected return component of pension expense. Under this methodology, asset

gains/losses that result from returns that differ from the Company’s long-term rate of return assumption are recognized in

the market-related value of assets on a level basis over a five year period. The difference between actual asset returns for the

plans of $(441) and $331 for the years ended December 31, 2008 and 2007, respectively, as compared to expected returns of

$279 and $283 for the years ended December 31, 2008 and 2007, respectively, will be fully reflected in the market-related

value of plan assets over the next five years using the methodology described above. The level of actuarial net losses

continues to exceed the allowable amortization corridor as defined under SFAS No. 87. Based on the 6.25% discount rate

selected as of December 31, 2008 and taking into account estimated future minimum funding, the difference between actual

and expected performance in 2008 will increase annual pension expense in future years. The increase in pension expense

will be approximately $30 in 2009 and will increase ratably to an increase of approximately $205 in 2014.

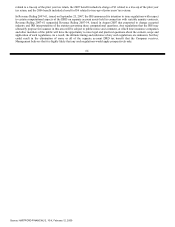

Contingencies Relating to Corporate Litigation and Regulatory Matters

Management follows the requirements of SFAS No. 5 “Accounting for Contingencies.” This statement requires management

to evaluate each contingent matter separately. A loss is recorded if probable and reasonably estimable. Management

establishes reserves for these contingencies at its “best estimate,” or, if no one number within the range of possible losses is

more probable than any other, the Company records an estimated reserve at the low end of the range of losses.

The Company has a quarterly monitoring process involving legal and accounting professionals. Legal personnel first

identify outstanding corporate litigation and regulatory matters posing a reasonable possibility of loss. These matters are

then jointly reviewed by accounting and legal personnel to evaluate the facts and changes since the last review in order to

determine if a provision for loss should be recorded or adjusted, the amount that should be recorded, and the appropriate

disclosure. The outcomes of certain contingencies currently being evaluated by the Company, which relate to corporate

litigation and regulatory matters, are inherently difficult to predict, and the reserves that have been established for the

estimated settlement amounts are subject to significant changes. In view of the uncertainties regarding the outcome of these

matters, as well as the tax-deductibility of payments, it is possible that the ultimate cost to the Company of these matters

could exceed the reserve by an amount that would have a material adverse effect on the Company’s consolidated results of

operations or cash flows in a particular quarterly or annual period.

Source: HARTFORD FINANCIAL S, 10-K, February 12, 2009