The Hartford 2008 Annual Report Download - page 177

Download and view the complete annual report

Please find page 177 of the 2008 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

-

565

-

566

-

567

-

568

-

569

-

570

-

571

-

572

-

573

-

574

-

575

-

576

-

577

-

578

-

579

-

580

-

581

-

582

-

583

-

584

-

585

-

586

-

587

-

588

-

589

-

590

-

591

-

592

-

593

-

594

-

595

-

596

-

597

-

598

-

599

-

600

-

601

-

602

-

603

-

604

-

605

-

606

-

607

-

608

-

609

-

610

-

611

-

612

-

613

-

614

-

615

-

616

-

617

-

618

-

619

-

620

-

621

-

622

-

623

-

624

-

625

-

626

-

627

-

628

-

629

-

630

-

631

-

632

-

633

-

634

-

635

-

636

-

637

-

638

-

639

-

640

-

641

-

642

-

643

-

644

-

645

-

646

-

647

-

648

-

649

-

650

-

651

-

652

-

653

-

654

-

655

-

656

-

657

-

658

-

659

-

660

-

661

-

662

-

663

-

664

-

665

-

666

-

667

-

668

-

669

-

670

-

671

-

672

-

673

-

674

-

675

-

676

-

677

-

678

-

679

-

680

-

681

-

682

-

683

-

684

-

685

-

686

-

687

-

688

-

689

-

690

-

691

-

692

-

693

-

694

-

695

-

696

-

697

-

698

-

699

-

700

-

701

-

702

-

703

-

704

-

705

-

706

-

707

-

708

-

709

-

710

-

711

-

712

-

713

-

714

-

715

-

716

-

717

-

718

-

719

-

720

-

721

-

722

-

723

-

724

-

725

-

726

-

727

-

728

-

729

-

730

-

731

-

732

-

733

-

734

-

735

-

736

-

737

-

738

-

739

-

740

-

741

-

742

-

743

-

744

-

745

-

746

-

747

-

748

-

749

-

750

-

751

-

752

-

753

-

754

-

755

-

756

-

757

-

758

-

759

-

760

-

761

-

762

-

763

-

764

-

765

-

766

-

767

-

768

-

769

-

770

-

771

-

772

-

773

-

774

-

775

-

776

-

777

-

778

-

779

-

780

-

781

-

782

-

783

-

784

-

785

-

786

-

787

-

788

-

789

-

790

-

791

-

792

-

793

-

794

-

795

-

796

-

797

-

798

-

799

-

800

-

801

-

802

-

803

-

804

-

805

-

806

-

807

-

808

-

809

-

810

-

811

-

812

-

813

-

814

-

815

|

|

Table of Contents

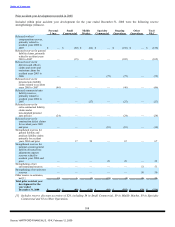

Policies in force

Policies in force represent the number of policies with coverage in effect as of the end of the period. The number of policies

in force is a growth measure used for Personal Lines, Small Commercial and Middle Market and is affected by both new

business growth and premium renewal retention.

Written pricing increase (decrease)

Written pricing increase (decrease) over the comparable period of the prior year includes the impact of rate filings, the

impact of changes in the value of the rating bases and individual risk pricing decisions. A number of factors impact written

pricing increases (decreases) including expected loss costs as projected by the Company’s pricing actuaries, rate filings

approved by state regulators, risk selection decisions made by the Company’s underwriters and marketplace competition.

Written pricing changes reflect the property and casualty insurance market cycle. Prices tend to increase for a particular line

of business when insurance carriers have incurred significant losses in that line of business in the recent past or the industry

as a whole commits less of its capital to writing exposures in that line of business. Prices tend to decrease when recent loss

experience has been favorable or when competition among insurance carriers increases.

Earned pricing increase (decrease)

Written premiums are earned over the policy term, which is six months for certain Personal Lines auto business and

12 months for substantially all of the remainder of the Company’s business. Because the Company earns premiums over the

6 to 12 month term of the policies, earned pricing increases (decreases) lag written pricing increases (decreases) by 6 to

12 months.

New business written premium

New business written premium represents the amount of premiums charged for policies issues to customers who were not

insured with the Company in the previous policy term. New business written premium plus renewal policy written premium

equals total written premium.

Premium renewal retention

Premium renewal retention represents the ratio of net written premium in the current period that is not derived from new

business divided by total net written premium of the prior period. Accordingly, premium renewal retention includes the

effect of written pricing changes on renewed business. In addition, the renewal retention rate is affected by a number of

other factors, including the percentage of renewal policy quotes accepted and decisions by the Company to non-renew

policies because of specific policy underwriting concerns or because of a decision to reduce premium writings in certain

lines of business or states. Premium renewal retention is also affected by advertising and rate actions taken by competitors.

Loss and loss adjustment expense ratio

The loss and loss adjustment expense ratio is a measure of the cost of claims incurred in the calendar year divided by earned

premium and includes losses incurred for both the current and prior accident years. Among other factors, the loss and loss

adjustment expense ratio needed for the Company to achieve its targeted return on equity fluctuates from year to year based

on changes in the expected investment yield over the claim settlement period, the timing of expected claim settlements and

the targeted returns set by management based on the competitive environment.

The loss and loss adjustment expense ratio is affected by claim frequency and claim severity, particularly for shorter-tail

property lines of business, where the emergence of claim frequency and severity is credible and likely indicative of ultimate

losses. Claim frequency represents the percentage change in the average number of reported claims per unit of exposure in

the current accident year compared to that of the previous accident year. Claim severity represents the percentage change in

the estimated average cost per claim in the current accident year compared to that of the previous accident year. As one of

the factors used to determine pricing, the Company’s practice is to first make an overall assumption about claim frequency

and severity for a given line of business and then, as part of the ratemaking process, adjust the assumption as appropriate for

the particular state, product or coverage.

Current accident year loss and loss adjustment expense ratio before catastrophes

The current accident year loss and loss adjustment expense ratio before catastrophes is a measure of the cost of

non-catastrophe claims incurred in the current accident year divided by earned premiums. Management believes that the

current accident year loss and loss adjustment expense ratio before catastrophes is a performance measure that is useful to

investors as it removes the impact of volatile and unpredictable catastrophe losses and prior accident year reserve

development.

Current accident year catastrophe ratio

Source: HARTFORD FINANCIAL S, 10-K, February 12, 2009