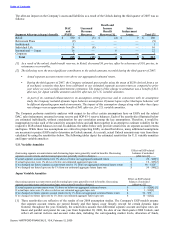

The Hartford 2008 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2008 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

-

565

-

566

-

567

-

568

-

569

-

570

-

571

-

572

-

573

-

574

-

575

-

576

-

577

-

578

-

579

-

580

-

581

-

582

-

583

-

584

-

585

-

586

-

587

-

588

-

589

-

590

-

591

-

592

-

593

-

594

-

595

-

596

-

597

-

598

-

599

-

600

-

601

-

602

-

603

-

604

-

605

-

606

-

607

-

608

-

609

-

610

-

611

-

612

-

613

-

614

-

615

-

616

-

617

-

618

-

619

-

620

-

621

-

622

-

623

-

624

-

625

-

626

-

627

-

628

-

629

-

630

-

631

-

632

-

633

-

634

-

635

-

636

-

637

-

638

-

639

-

640

-

641

-

642

-

643

-

644

-

645

-

646

-

647

-

648

-

649

-

650

-

651

-

652

-

653

-

654

-

655

-

656

-

657

-

658

-

659

-

660

-

661

-

662

-

663

-

664

-

665

-

666

-

667

-

668

-

669

-

670

-

671

-

672

-

673

-

674

-

675

-

676

-

677

-

678

-

679

-

680

-

681

-

682

-

683

-

684

-

685

-

686

-

687

-

688

-

689

-

690

-

691

-

692

-

693

-

694

-

695

-

696

-

697

-

698

-

699

-

700

-

701

-

702

-

703

-

704

-

705

-

706

-

707

-

708

-

709

-

710

-

711

-

712

-

713

-

714

-

715

-

716

-

717

-

718

-

719

-

720

-

721

-

722

-

723

-

724

-

725

-

726

-

727

-

728

-

729

-

730

-

731

-

732

-

733

-

734

-

735

-

736

-

737

-

738

-

739

-

740

-

741

-

742

-

743

-

744

-

745

-

746

-

747

-

748

-

749

-

750

-

751

-

752

-

753

-

754

-

755

-

756

-

757

-

758

-

759

-

760

-

761

-

762

-

763

-

764

-

765

-

766

-

767

-

768

-

769

-

770

-

771

-

772

-

773

-

774

-

775

-

776

-

777

-

778

-

779

-

780

-

781

-

782

-

783

-

784

-

785

-

786

-

787

-

788

-

789

-

790

-

791

-

792

-

793

-

794

-

795

-

796

-

797

-

798

-

799

-

800

-

801

-

802

-

803

-

804

-

805

-

806

-

807

-

808

-

809

-

810

-

811

-

812

-

813

-

814

-

815

|

|

Table of Contents

In valuing the embedded derivative, the Company attributes to the derivative a portion of fees collected from the contract

holder equal to the present value of future claims (the “Attributed Fees”). Attributed Fees in dollars are determined at the

inception of each quarterly cohort by setting the dollars equal to the present value of expected claims. The Attributed Fees,

in basis points, are determined by dividing the Attributed Fees in dollars by the present value of account value. The

Attributed Fees in basis points are locked-in for each quarterly cohort. Recent capital markets conditions, in particular high

equity index volatility and low interest rates have increased the Attributed Fees for recent cohorts to a level above our rider

fees.

Capital market assumptions can significantly change the value of embedded derivative living benefit guarantees. For

example, independent future decreases in equity market returns, future decreases in interest rates and future increases in

equity index volatility will all have the effect of increasing the value of the embedded derivative liability as of December 31,

2008 resulting in a realized loss in net income. Furthermore, changes in policyholder behavior can also significantly change

the value of the GMWB. For example, independent future increases in fund mix towards equity based funds vs. bond funds,

future increases in withdrawals, future decreasing mortality, future increasing usage of the step-up feature and decreases in

lapses will all have the effect of increasing the value of the GMWB embedded derivative liability as of December 31, 2008

resulting in a realized loss in net income. Independent changes in any one of these assumptions moving in the opposite

direction will have the effect of decreasing the value of the embedded derivative liability as of December 31, 2008 resulting

in a realized gain in net income. As markets change, mature and evolve and actual policyholder behavior emerges,

management continually evaluates the appropriateness of its assumptions. In addition, management regularly evaluates the

valuation model, incorporating emerging valuation techniques where appropriate, including drawing on the expertise of

market participants and valuation experts.

Valuation of Investments and Derivative Instruments

The Hartford’s investments in fixed maturities include bonds, redeemable preferred stock and commercial paper. These

investments, along with certain equity securities, which include common and non-redeemable preferred stocks, are classified

as “available-for-sale” and are carried at fair value. The after-tax difference from cost or amortized cost is reflected in

stockholders’ equity as a component of Accumulated Other Comprehensive Income (“AOCI”), after adjustments for the

effect of deducting the life and pension policyholders’ share of the immediate participation guaranteed contracts and certain

life and annuity deferred policy acquisition costs and reserve adjustments. The equity investments associated with the

variable annuity products offered in Japan are recorded at fair value and are classified as “trading” with changes in fair value

recorded in net investment income. Policy loans are carried at outstanding balance. Mortgage loans on real estate are

recorded at the outstanding principal balance adjusted for amortization of premiums or discounts and net of valuation

allowances, if any. Short-term investments are carried at amortized cost, which approximates fair value. Limited

partnerships and other alternative investments are reported at their carrying value with the change in carrying value

accounted for under the equity method and accordingly the Company’s share of earnings are included in net investment

income. Recognition of limited partnerships and other alternative investment income is delayed due to the availability of the

related financial statements, as private equity and other funds are generally on a three-month delay and hedge funds are on a

one-month delay. Accordingly, income at December 31, 2008 may not include the full impact of current year changes in

valuation of the underlying assets and liabilities. Other investments primarily consist of derivatives instruments which are

carried at fair value.

Valuation of Fixed Maturity, Short-Term and Equity Securities, Available-for-Sale

The fair value for fixed maturity, short-term and equity securities, available-for-sale, is determined by management after

considering one of three primary sources of information: third party pricing services, independent broker quotations or

pricing matrices. Security pricing is applied using a “waterfall” approach whereby publicly available prices are first sought

from third party pricing services, the remaining unpriced securities are submitted to independent brokers for prices, or lastly,

securities are priced using a pricing matrix. Typical inputs used by these three pricing methods include, but are not limited

to, reported trades, benchmark yields, issuer spreads, bids, offers, and/or estimated cash flows and prepayments speeds.

Based on the typical trading volumes and the lack of quoted market prices for fixed maturities, third party pricing services

will normally derive the security prices through recent reported trades for identical or similar securities making adjustments

through the reporting date based upon available market observable information as outlined above. If there are no recent

reported trades, the third party pricing services and brokers may use matrix or model processes to develop a security price

where future cash flow expectations are developed based upon collateral performance and discounted at an estimated market

rate. Included in the pricing of asset-backed securities (“ABS”), collateralized mortgage obligations (“CMOs”), and

mortgage-backed securities (“MBS”) are estimates of the rate of future prepayments of principal over the remaining life of

the securities. Such estimates are derived based on the characteristics of the underlying structure and prepayment speeds

previously experienced at the interest rate levels projected for the underlying collateral. Actual prepayment experience may

vary from these estimates.

Prices from third party pricing services are often unavailable for securities that are rarely traded or are traded only in

privately negotiated transactions. As a result, certain securities are priced via independent broker quotations which utilize

inputs that may be difficult to corroborate with observable market based data. Additionally, the majority of these

independent broker quotations are non-binding. A pricing matrix is used to price securities for which the Company is unable

Source: HARTFORD FINANCIAL S, 10-K, February 12, 2009