The Hartford 2008 Annual Report Download - page 275

Download and view the complete annual report

Please find page 275 of the 2008 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

-

565

-

566

-

567

-

568

-

569

-

570

-

571

-

572

-

573

-

574

-

575

-

576

-

577

-

578

-

579

-

580

-

581

-

582

-

583

-

584

-

585

-

586

-

587

-

588

-

589

-

590

-

591

-

592

-

593

-

594

-

595

-

596

-

597

-

598

-

599

-

600

-

601

-

602

-

603

-

604

-

605

-

606

-

607

-

608

-

609

-

610

-

611

-

612

-

613

-

614

-

615

-

616

-

617

-

618

-

619

-

620

-

621

-

622

-

623

-

624

-

625

-

626

-

627

-

628

-

629

-

630

-

631

-

632

-

633

-

634

-

635

-

636

-

637

-

638

-

639

-

640

-

641

-

642

-

643

-

644

-

645

-

646

-

647

-

648

-

649

-

650

-

651

-

652

-

653

-

654

-

655

-

656

-

657

-

658

-

659

-

660

-

661

-

662

-

663

-

664

-

665

-

666

-

667

-

668

-

669

-

670

-

671

-

672

-

673

-

674

-

675

-

676

-

677

-

678

-

679

-

680

-

681

-

682

-

683

-

684

-

685

-

686

-

687

-

688

-

689

-

690

-

691

-

692

-

693

-

694

-

695

-

696

-

697

-

698

-

699

-

700

-

701

-

702

-

703

-

704

-

705

-

706

-

707

-

708

-

709

-

710

-

711

-

712

-

713

-

714

-

715

-

716

-

717

-

718

-

719

-

720

-

721

-

722

-

723

-

724

-

725

-

726

-

727

-

728

-

729

-

730

-

731

-

732

-

733

-

734

-

735

-

736

-

737

-

738

-

739

-

740

-

741

-

742

-

743

-

744

-

745

-

746

-

747

-

748

-

749

-

750

-

751

-

752

-

753

-

754

-

755

-

756

-

757

-

758

-

759

-

760

-

761

-

762

-

763

-

764

-

765

-

766

-

767

-

768

-

769

-

770

-

771

-

772

-

773

-

774

-

775

-

776

-

777

-

778

-

779

-

780

-

781

-

782

-

783

-

784

-

785

-

786

-

787

-

788

-

789

-

790

-

791

-

792

-

793

-

794

-

795

-

796

-

797

-

798

-

799

-

800

-

801

-

802

-

803

-

804

-

805

-

806

-

807

-

808

-

809

-

810

-

811

-

812

-

813

-

814

-

815

|

|

Table of Contents

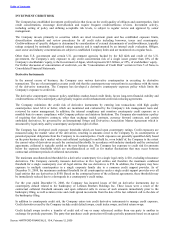

INVESTMENT CREDIT RISK

The Company has established investment credit policies that focus on the credit quality of obligors and counterparties, limit

credit concentrations, encourage diversification and require frequent creditworthiness reviews. Investment activity,

including setting of policy and defining acceptable risk levels, is subject to regular review and approval by senior

management.

The Company invests primarily in securities which are rated investment grade and has established exposure limits,

diversification standards and review procedures for all credit risks including borrower, issuer and counterparty.

Creditworthiness of specific obligors is determined by consideration of external determinants of creditworthiness, typically

ratings assigned by nationally recognized ratings agencies and is supplemented by an internal credit evaluation. Obligor,

asset sector and industry concentrations are subject to established Company limits and are monitored on a regular basis.

Other than U.S. government and certain U.S. government agencies backed by the full faith and credit of the U.S.

government, the Company’s only exposure to any credit concentration risk of a single issuer greater than 10% of the

Company’s stockholders’ equity, is the Government of Japan, which represents $2.3 billion, or 25%, of stockholders’ equity.

For further discussion of concentration of credit risk, see the “Concentration of Credit Risk” section in Note 5 of Notes to

Consolidated Financial Statements.

Derivative Instruments

In the normal course of business, the Company uses various derivative counterparties in executing its derivative

transactions. The use of counterparties creates credit risk that the counterparty may not perform in accordance with the terms

of the derivative transaction. The Company has developed a derivative counterparty exposure policy which limits the

Company’s exposure to credit risk.

The derivative counterparty exposure policy establishes market-based credit limits, favors long-term financial stability and

creditworthiness of the counterparty and typically requires credit enhancement/credit risk reducing agreements.

The Company minimizes the credit risk of derivative instruments by entering into transactions with high quality

counterparties rated A2/A or better, which are monitored and evaluated by the Company’s risk management team and

reviewed by senior management. In addition, the internal compliance unit monitors counterparty credit exposure on a

monthly basis to ensure compliance with Company policies and statutory limitations. The Company also maintains a policy

of requiring that derivative contracts, other than exchange traded contracts, currency forward contracts, and certain

embedded derivatives, be governed by an International Swaps and Derivatives Association Master Agreement which is

structured by legal entity and by counterparty and permits right of offset.

The Company has developed credit exposure thresholds which are based upon counterparty ratings. Credit exposures are

measured using the market value of the derivatives, resulting in amounts owed to the Company by its counterparties or

potential payment obligations from the Company to its counterparties. Credit exposures are generally quantified daily based

on the prior business day’s market value and collateral is pledged to and held by, or on behalf of, the Company to the extent

the current value of derivatives exceeds the contractual thresholds. In accordance with industry standards and the contractual

agreements, collateral is typically settled on the next business day. The Company has exposure to credit risk for amounts

below the exposure thresholds which are uncollateralized as well as for market fluctuations that may occur between

contractual settlement periods of collateral movements.

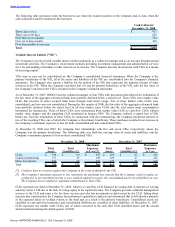

The maximum uncollateralized threshold for a derivative counterparty for a single legal entity is $10, excluding reinsurance

derivatives. The Company currently transacts derivatives in five legal entities and therefore the maximum combined

threshold for a single counterparty over all legal entities that use derivatives is $50. In addition, the Company may have

exposure to multiple counterparties in a single corporate family due to a common credit support provider. As of

December 31, 2008, the maximum combined threshold for all counterparties under a single credit support provider over all

legal entities that use derivatives is $100. Based on the contractual terms of the collateral agreements, these thresholds may

be immediately reduced due to a downgrade in a counterparty’s credit rating.

For the year ended December 31, 2008, the Company has incurred losses of $46 on derivative instruments due to

counterparty default related to the bankruptcy of Lehman Brothers Holdings Inc. These losses were a result of the

contractual collateral threshold amounts and open collateral calls in excess of such amounts immediately prior to the

bankruptcy filing, as well as interest rate and credit spread movements from the date of the last collateral call to the date of

the bankruptcy filing.

In addition to counterparty credit risk, the Company enters into credit derivative instruments to manage credit exposure.

Credit derivatives used by the Company include credit default swaps, credit index swaps, and total return swaps.

Credit default swaps involve a transfer of credit risk of one or many referenced entities from one party to another in

exchange for periodic payments. The party that purchases credit protection will make periodic payments based on an agreed

Source: HARTFORD FINANCIAL S, 10-K, February 12, 2009