Tesco 2008 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2008 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

|

|

Tesco PLC Annual Report and

Financial Statements 2008 99

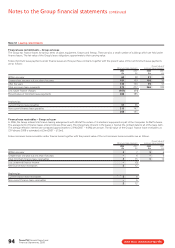

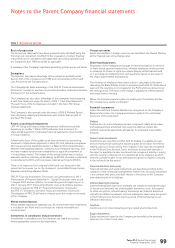

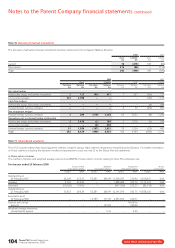

Basis of preparation

These financial statements have been prepared under UK GAAP using the

historical cost convention modified for the revaluation of certain financial

instruments and in accordance with applicable accounting standards and

the Companies Acts 1985 and 2006 as applicable.

A summary of the Company’s significant accounting policies are set out below.

Exemptions

The Directors have taken advantage of the exemption available under

Section 230 of the Companies Act 1985 and not presented a Profit and

Loss Account for the Company alone.

The Company has taken advantage of the FRS 29 ‘Financial Instruments:

Disclosures’ exemption and has not provided derivative financial instrument

disclosures for the company alone.

The Company has also taken advantage of the exemption from preparing

a cash flow statement under the terms of FRS 1 ‘Cash Flow Statement’.

The cash flows of the Company are included in the Tesco PLC Group

financial statements.

The Company is also exempt under the terms of FRS 8 ‘Related Parties’

from disclosing related party transactions with entities that are part of

the Tesco PLC Group.

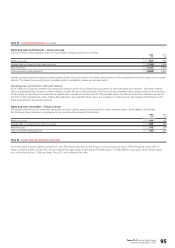

Recent accounting developments

UITF 44 ‘Group and treasury share transactions’ (effective for periods

beginning on or after 1 March 2007) addresses how to account for

share-based payments in individual financial statements of each entity

in Group situations.

Following the issue of this guidance we have reviewed our accounting

treatment of share-based payments in Tesco PLC and subsidiary companies.

Our new accounting treatment results in a Balance Sheet reclassification

between intercompany balances, investments and retained earnings, and

we have restated our prior year comparatives to apply this treatment as

if it had always existed. The impact of this reclassification was to reduce

amounts owed by subsidiary undertakings by £295m, decrease investments

in subsidiaries by £67m and to decrease retained earnings by £362m.

There is no impact on the Company’s Profit and Loss Account for the

current and prior years nor on the Company’s consolidated Group Income

Statement and Group Balance Sheet.

FRS 29 ‘Financial Instruments: Disclosures’ and amendments to IAS 1

‘Presentation of Financial Statements – Capital Disclosures’ were issued

in August 2005 and are effective for accounting periods beginning on or

after 1 January 2007. These amendments revise and enhance previous

disclosures required by FRS 25 ‘Financial Instruments: Disclosures’

and FRS 13 ‘Derivatives and other financial instruments: Disclosures’.

The adoption of FRS 29 will have no impact upon the results or net assets

of the Company.

Money market deposits

Money market deposits are stated at cost. All income from these investments

is included in the Profit and Loss Account as interest receivable and

similar income.

Investments in subsidiaries and joint ventures

Investments in subsidiaries and joint ventures are stated at cost less,

where appropriate, provisions for impairment.

Foreign currencies

Assets and liabilities in foreign currencies are translated into Pounds Sterling

at the financial year end exchange rates.

Share-based payments

Employees of the Company receive part of their remuneration in the form

of share-based payment transactions, whereby employees render services

in exchange for shares or rights over shares (equity-settled transactions)

or in exchange for entitlements to cash payments based on the value of

the shares (cash-settled transactions).

The fair value of employee share option plans is calculated at the grant

date using the Black-Scholes model. In accordance with FRS 20 ‘Share-based

payment’ the resulting cost is charged to the Profit and Loss Account over

the vesting period. The value of the charge is adjusted to reflect expected

and actual levels of vesting.

Where the Company awards options to employees of subsidiary entities,

this is treated as a capital contribution.

Financial instruments

Financial assets and financial liabilities are recognised on the Company’s

Balance Sheet when the Company becomes a party to the contractual

provisions of the instrument.

Debtors

Debtors are non interest-bearing and are recognised initially at fair value,

and subsequently at amortised cost using the effective interest rate

method, reduced by appropriate allowances for estimated irrecoverable

amounts.

Current asset investments

Investments are classified as either held for trading or available-for-sale,

and are measured at subsequent reporting dates at fair value. For held for

trading, gains and losses arising from changes in fair value are recognised

in the Profit and Loss Account. Gains and losses arising from changes in

fair value for available-for-sale investments are recognised directly in equity,

until the security is disposed of or is determined to be impaired, at which

time the cumulative gain or loss previously recognised in equity is included

in the net result for the period.

Financial liabilities and equity

Financial liabilities and equity instruments are classified according to the

substance of the contractual arrangements entered into. An equity instrument

is any contract that gives a residual interest in the assets of the Company

after deducting all of its liabilities.

Interest-bearing borrowings

Interest-bearing bank loans and overdrafts are initially recorded at the value

of the amount received, net of attributable transaction costs. Subsequent

to initial recognition, interest-bearing borrowings are stated at amortised

cost with any difference between cost and redemption value being recognised

in the Profit and Loss Account over the period of the borrowings on an

effective interest basis.

Creditors

Creditors are non interest-bearing and are stated at amortised cost.

Equity instruments

Equity instruments issued by the Company are recorded at the proceeds

received, net of direct issue costs.

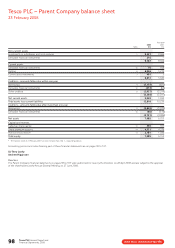

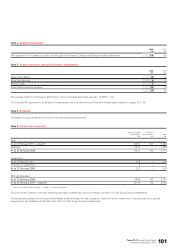

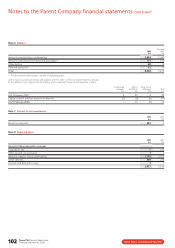

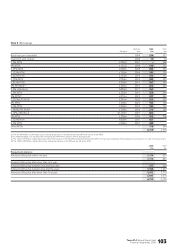

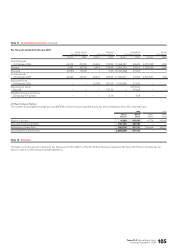

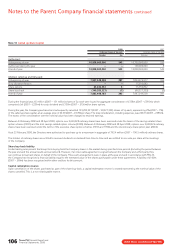

Notes to the Parent Company financial statements

Note 1 Accounting policies